| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.618 | 3.578 | 0.04 |

| Australian 10-year bond (%) | 4.308 | 4.235 | 0.073 |

| Australian 30-year bond (%) | 4.94 | 4.893 | 0.047 |

| United States 2-year bond (%) | 3.604 | 3.504 | 0.1 |

| United States 10-year bond (%) | 4.085 | 3.989 | 0.096 |

| United States 30-year bond (%) | 4.6367 | 4.5512 | 0.0855 |

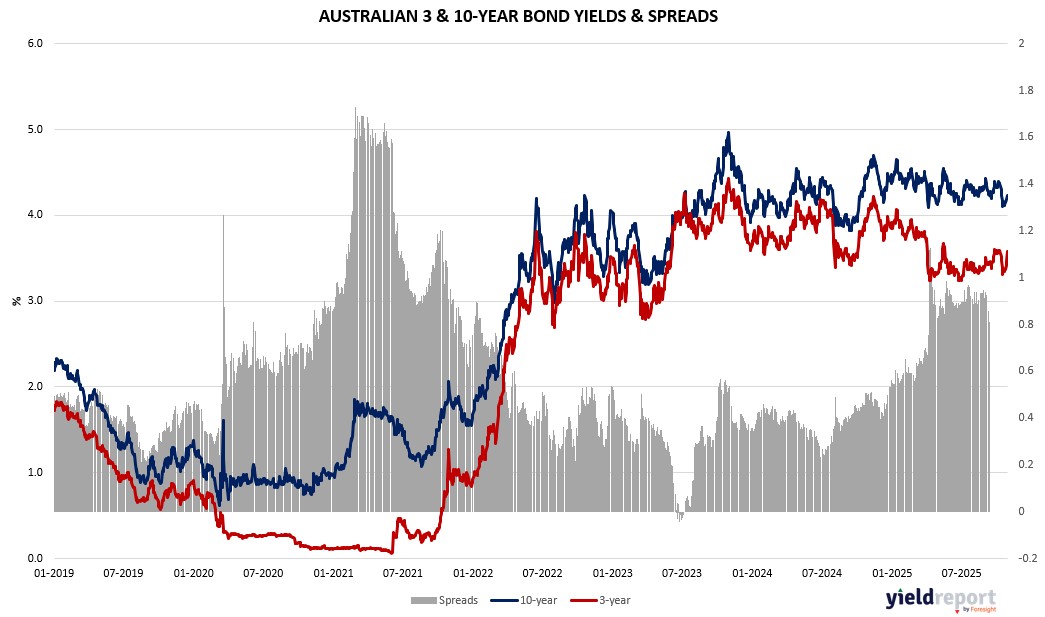

Overview of the Australian Bond Market

Australian government bond yields climbed as third-quarter inflation prints exceeded forecasts, reducing odds of RBA cuts and aligning with a hawkish Fed tone that bolstered global yields. The 10-year yield rose 7 basis points to 4.29%, the 2-year added 3 to 3.57%, and the 15-year increased 7 to 4.60%. The curve showed little change, with markets pricing steady policy amid resilient data.

The CPI rose 1.3% quarterly and 3.2% annually, with RBA’s trimmed mean at 1.0% quarterly and 3.0% yearly—0.3 points above estimates—pushing back easing expectations. Weighted median CPI hit 2.8% year-over-year, signaling persistent pressures. This came as US-China trade progress, including extended truces and export flows, eased global risks but left competition intact, potentially supporting yields if supply chains stabilize without reigniting inflation.

The Aussie dollar held near 0.6591, dragged by a softer yuan and copper prices ahead of PPI and China PMI data. Finance Minister Satsuki Katayama backed the BOJ’s rate hold as reasonable, while UK developments added currency volatility. Bond traders anticipate steady auctions, though inflation resilience could pressure prices if growth holds, echoing Fed debates and strengthening the higher-for-longer narrative.

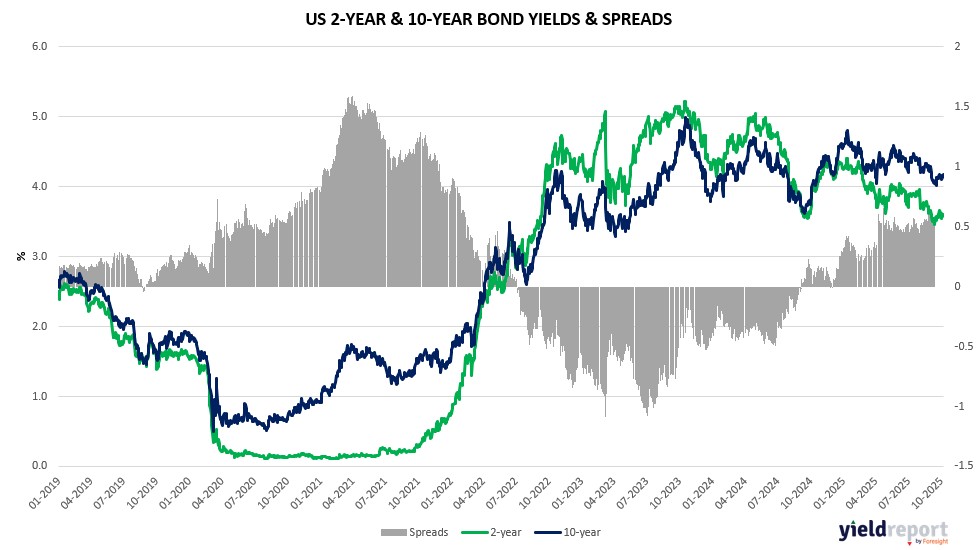

Overview of the US Bond Market

Bond traders pared bets on aggressive Federal Reserve easing following the central bank’s hawkish-tilted rate cut and Powell’s caution that a December reduction is not assured, pushing Treasury yields higher across the curve. The 10-year yield rose 2 basis points to around 4.10%, while the 2-year added to 3.61% and the 30-year climbed to 4.65%. The 2s-10s curve steepened slightly to +48.5 basis points amid month-end flows and a stronger dollar.

The selloff reflected tempered rate-cut expectations as policymakers grapple with resilient jobs data and inflation, with the Fed’s 10-2 vote highlighting internal divisions—one for a larger cut, another for holding steady. Treasury Secretary Scott Bessent supported the move but called for reforms, echoing doubts about further easing amid the US-China trade truce that eases global risks but leaves uncertainties. The agreement, which includes tariff rollbacks and export continuity for rare earths, may stabilize supply chains but falls short of a full resolution, potentially limiting downside for yields if economic fallout is contained.

On the economic front, durable goods orders rose 0.2% in September, missing forecasts, while consumer confidence improved more than expected. The dollar index surged 0.31% to its highest since early August, bolstered by rising yields and ECB steadiness, with EUR/USD down 0.28% and USD/JPY up 0.92%. Gold jumped 2.0% to $4,018.72 an ounce on safe-haven demand, but oil dipped 0.5% as investors assessed the trade deal.

Swap contracts now price in under half a point of easing by year-end, with markets bracing for Dallas Fed President Lorie Logan’s remarks on Friday. Asset managers trimmed net long positions in Treasury futures last week, per CFTC data, with leveraged funds reducing shorts in longer tenors. Dealers expect steady coupon auction sizes for August-October, aligning with April guidance, though 5- and 10-year sales may edge $1 billion larger. While trade progress dissipates some uncertainty, high valuations and AI spending scrutiny could pressure bonds if growth holds, strengthening the case for rates to stay elevated longer.