| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 45,883.45 | 49.23 | 0.11% |

| S&P 500 | 6,615.28 | 30.99 | 0.47% |

| Nasdaq | 22,348.75 | 207.65 | 0.94% |

| VIX | 15.69 | 0.93 | 6.30% |

| Gold | 3,717.30 | -1.7 | -0.05% |

| Oil | 63.32 | 0.02 | 0.03% |

OVERVIEW OF THE US MARKET

Wall Street surged to fresh records as traders bet almost unanimously on a Federal Reserve interest rate cut this Wednesday, the first since Donald Trump’s presidency. Markets are positioned for a quarter-point reduction, but the bigger question is how aggressively the Fed will ease into 2026. The rally has been powered by a record-breaking $14 trillion advance in U.S. equities, with the S&P 500 topping 6,600 and the Nasdaq 100 extending its longest winning streak since 2023. Tesla rebounded sharply, Alphabet crossed the $3 trillion valuation mark, and positive sentiment was boosted by progress on a U.S.-China TikTok deal.

Treasuries rallied, with two-year yields near one-year lows, while the dollar weakened. Labor market softness and contained inflation have cemented expectations for an initial cut, though officials remain cautious with inflation still above target. Analysts emphasize the importance of the Fed’s “dot plot” and Powell’s press conference. A dovish tone could fuel dollar weakness and extend equity gains, while a “wait and see” stance may slow momentum. Retail sales data due before the decision will also provide critical insight into consumer demand.

Strategists remain divided. Some, like UBS, expect 100 basis points of cuts by early 2026, citing easing inflation and weakening jobs. Others, including Morgan Stanley, warn markets may be overly optimistic, with risks that the Fed may not deliver cuts as swiftly as investors hope. JPMorgan notes equities could temporarily turn cautious once easing resumes, while history shows markets often rally strongly in the year following a rate-cut cycle restart.

Corporate news added complexity: Nvidia faced new antitrust pressure in China, Google weighed ad tech divestments, Disney partnered with Webtoon for digital comics, and the FTC probed Ticketmaster. Nvidia also expanded cloud partnerships via CoreWeave, while Snap moved closer to launching consumer AR glasses. Robinhood announced a private markets fund, Exxon Mobil pushed for retail investor alignment, and Kering reported a cyberattack.

Meanwhile, President Trump reignited debate on quarterly reporting, advocating for semiannual disclosures to reduce costs and allow management to focus long term. Analysts warn this could reduce transparency for investors.

Volatility expectations remain subdued, while earnings momentum is strengthening, with 2026 estimates rising for nine consecutive weeks. Market bulls see further upside, projecting the S&P 500 could hit 7,200 by mid-2026. Still, risks around inflation and labor market weakness remain central.

At Monday’s close, the S&P 500 rose 0.5%, Nasdaq 100 gained 0.8%, and Dow added 0.1%. Treasury yields eased across maturities, gold climbed 1% to $3,680 an ounce, and oil rose to $63.32. Bitcoin slipped to $115,335, while ether fell 2.7%. The euro, pound, and yen all strengthened against a weaker dollar.

Overall, Wall Street’s optimism is pinned on the Fed validating expectations of a cutting cycle. Investors see strong earnings and easing rates fueling momentum into 2026, but cautious central bank messaging or renewed inflationary pressures could temper the exuberance.

OVERVIEW OF THE AUSTRALIAN MARKET

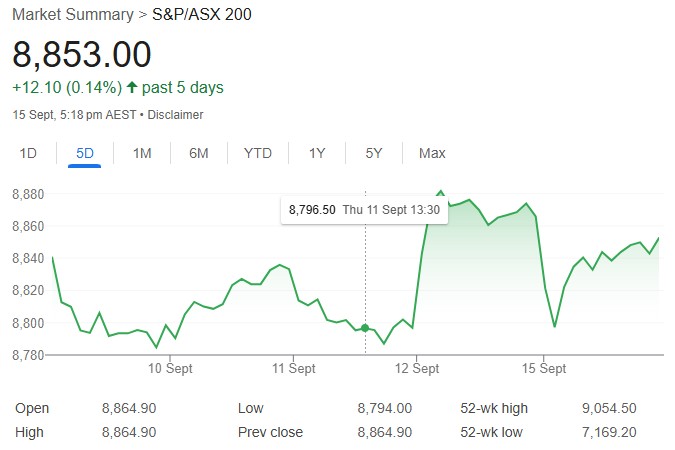

Australian shares closed marginally lower on September 15, 2025, paring early losses after dipping nearly 70 points intraday, as health care and materials weighed despite more winners than losers overall. The S&P/ASX 200 slipped 0.13% to 8,853.0, while the All Ordinaries fell 0.09% to 9,120.9. Small ords edged down 0.17%, emerging companies up 0.06%, and all tech gained 0.11%. Seven of 11 sectors rose, led by energy up 0.64%, consumer discretionary 0.59%, utilities 0.37%, and consumer staples 0.31%. Financials dipped 0.20%, communication services 0.27%, materials 0.54%, and health care 0.84%.

Advancers outnumbered decliners 145 to 128 in the ASX 300, with ebb and flow among mega-caps. Health care followed CSL down 1.6% to its lowest since June 2019, erasing nearly a quarter of value since August’s gloomy earnings. Big banks mixed: ANZ and CBA off 0.6% each, NAB and Westpac up 0.6%. Resources sapped points, with BHP down 0.6% and Rio Tinto 0.1% on softer Chinese industrial production and retail sales undershooting, pressuring iron ore prices. Energy led as uranium and coal bounced, Boss Energy up 7.9% and Whitehaven Coal 2.0%. Gold sub-index plunged 2.7% on profit-taking despite steady prices near $US3,764 record—Evolution Mining fell 5.2%, Capricorn Metals 4.3%, Regis Resources 4.1%, Perseus Mining 3.4%—frustrating but historically rebounding with metal strength.

Lithium surged on 2% higher Chinese carbonate futures to RMB 72,780/t and 1.3% spot spodumene to $US810/t, plus weekend Australian reports of global heavyweights and sovereign funds eyeing assets amid US push against China dominance—Pilbara Minerals rose 9.1%, Liontown Resources 6.3%, IGO 6.7%, Mineral Resources 3.3%, recouping fraction of last week’s CATL mine rumor losses. Consumer heavyweights buoyed staples and discretionary: Woolworths and Coles tracking gains, Wesfarmers supporting. AMP surged 6.5% to $1.80 on $120 million class action settlement over super fees. Guzman y Gomez jumped over 5% ex-dividend, Credit Corp down 1.5% locking dividends. Qantas slipped 1% to $11.30 ahead of Tuesday ex-dividend.

IG’s Tony Sycamore noted buyers below 8800 for fourth in five sessions, signaling consolidation after August’s run amid weak seasonality and tariff volatility. Subdued tone ahead of AU jobs Thursday and US Fed decision Wednesday, with US futures up modestly signaling records post-retail sales and industrial production.

Top gainers: Kaili Resources 36.4% on drilling complete, Resolution Minerals 25.0% on antimony results, LTR Pharma 19.8%, Dateline Resources 17.3%, Sunrise Energy Metals 15.5%, Immutep 13.0%, Felix Gold 12.5% on antimony intersects, Race Oncology 11.8%, Vulcan Energy Resources 11.7%, Civmec 10.9%, St George Mining 10.8%, Avita Medical 10.1% on CE Mark, Pilbara Minerals 9.1% on stake increase, Lumos Diagnostics 9.1%, Minerals 260 9.1% on conference, Cogstate 8.5%, Falcon Metals 8.5%, Dreadnought Resources 8.0% on drilling resume, Shape Australia 8.0%, Boss Energy 7.9%, Emeco 7.9% on speculation, Zimplats 7.8%, Fiducian Group 7.5%, Decidr Ai 7.4%, IGO 6.7%, Duratec 6.4%, Liontown 6.3%. Decliners: Ora Banda Mining down 10.0%, African Gold 9.7%, Metallium 8.1% on notice, Zenith Minerals 8.0%, Matsa Resources 7.7%, West Wits Mining 6.4% on placement, Turaco Gold 6.1%, Talga Group 5.4%, Evolution Mining 5.3%, Fleetwood 5.2%, Washington H Soul Pattinson 5.2% on report.

AUD/USD rose 0.09% to 0.6657, clinging to 10-month highs on iron ore support and US cut hopes weighing dollar. Ex-dividend: Chorus, Credit Corp, Data3, Fleetwood, Guzman y Gomez, Kelsian, Lovisa, Qube, Ramelius Resources.

ON THE ASX: ASX 200 down 11.9 points or 0.13% to 8,853; All Ordinaries down 7.8 points or 0.09% to 9,120.9. NZX 50 down 0.15% to 13,208.31; Nikkei up 0.88% to 44,768.12.