| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 47,289.33 | -427.09 | -0.90% |

| S&P 500 | 6,812.63 | -36.46 | -0.53% |

| Nasdaq | 23,275.92 | -89.76 | -0.38% |

| VIX | 17.24 | 0.89 | 5.44% |

| Gold | 4,265.20 | -9.6 | -0.22% |

| Oil | 59.57 | 0.25 | 0.42% |

OVERVIEW OF THE US MARKET

Wall Street closed lower on December 1, 2025, as a cryptocurrency selloff deepened and caution spread amid global bond market ripples from Japan. The S&P 500 fell 0.53% to 6812.63, slipping below 6800 intraday before a slight recovery, while the Nasdaq Composite dropped 0.38% to 23275.92 and the Dow Jones Industrial Average declined 0.90% to 47289.33. The pullback interrupted a rally that had pushed the S&P 500 to its longest monthly winning streak since 2021, with small caps underperforming as the Russell 2000 slid over 1%. Traders shunned riskier assets, including crypto-exposed stocks, following nearly $1 billion in liquidated leveraged positions that drove Bitcoin down to around $85,000.

Sector performance was mixed, with energy up 0.91% on rising oil prices and information technology edging 0.07% higher, buoyed by megacaps. However, utilities tumbled 2.35%, health care and industrials each lost 1.49%, and real estate fell 1.39%. Communication services dropped 1.01%, reflecting broader risk aversion. Among stock movers, NVIDIA Corp. rose 1.65% on volume of 187.5 million shares after announcing a $2 billion investment in Synopsys Inc., which surged amid the tie-up aimed at expanding AI applications. Q32 Bio Inc. soared 74.43% on heavy trading, while decliners included Bitfarms Ltd. down 5.75%, Opendoor Technologies Inc. off 7.27%, and Plug Power Inc. sliding 4.48%. Moderna Inc. fell after FDA restrictions on vaccines, and Barrick Mining Corp. gained on IPO exploration for its North American assets potentially worth over $60 billion.

Economic data showed US factory activity contracting for the ninth straight month, with the ISM manufacturing PMI at 48.2 in November, below the 49.0 forecast and down from 48.7 in October, signaling weakening orders and rising input costs. This added to market jitters ahead of key releases, including Friday’s PCE inflation gauge expected to show stable but sticky pressures, and ADP employment figures. Fed officials face a debate on the job market at their December 9-10 meeting, with speculation leaning toward a 25-basis-point rate cut despite robust earnings growth projections.

Strategists remain optimistic on seasonality, noting December’s historical strength. Sam Stovall at CFRA highlighted the S&P 500’s second-best average return and lowest volatility in the month since 1990. LPL Financial’s Adam Turnquist pointed to gains typically emerging in the second half, with the index averaging 1.4% up since 1950 and 73% positivity rate. For years like 2025 where the S&P 500 entered December up over 10%, Bespoke Investment Group sees average gains exceeding 2%. Ulrike Hoffmann-Burchardi at UBS Global Wealth Management emphasized robust earnings growth of 7-14% supporting upside, viewing the soft economic patch as temporary with global acceleration in 2026. RBC Capital Markets’ Lori Calvasina forecast the index at 7,750 by end-2026, implying 13% gains, favoring value over growth and small caps if macro improves. Corporate news included OpenAI’s stake in Thrive Holdings, DeepSeek’s AI model updates, and Eli Lilly cutting Zepbound prices amid competition. Overall, while Monday’s dip reflected benign risk aversion without fundamental drivers, per Kyle Rodda at Capital.com, year-end positioning and consumer spending set the stage for a potential Santa rally.

OVERVIEW OF THE AUSTRALIAN MARKET

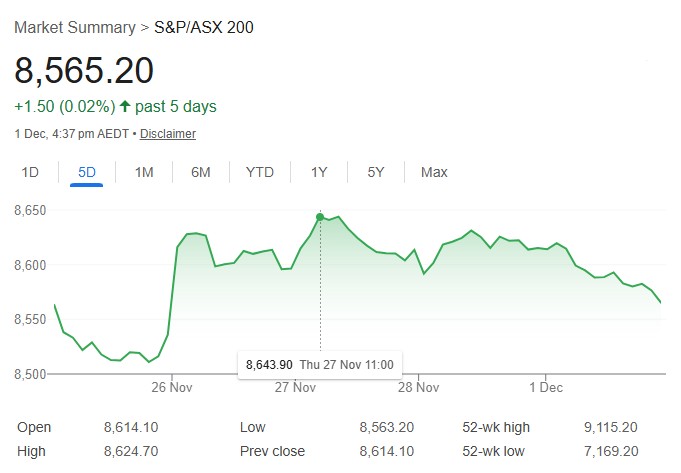

The S&P/ASX 200 closed lower on December 1, 2025, down 0.57% at 8,565.2, amid weakness in high P/E sectors and broader risk aversion tied to global crypto and bond moves. The All Ordinaries fell 0.58% to 8,866.5, with small ords down 0.80% and the all tech index tumbling 1.64%. Advancers trailed decliners 78 to 198 in the ASX 300, reflecting heavy weighting in declining areas like information technology (-1.33%), communication services (-1.11%), health care (-1.65%), and financials (-0.94%). Resources provided some offset, with materials up 0.27% and energy gaining 0.52% on oil strength.

Precious metals and critical minerals drove gains, buoyed by silver and gold rallies amid tight supply. Minerals 260 surged 22.1% after doubling its Bullabulling Gold Project resource to 4.5Moz, aligning with uptrends. Unico Silver rose 16.9%, Sun Silver 15.9%, and Andean Silver 12.6% on sector momentum. Greatland Resources climbed 10.2% post-Havieron feasibility presentation, and Lake Resources added 8.3% in uptrend continuation. Silver Mines gained 7.5%, DPM Metals 6.1%, and West African Resources 4.3%. Chalice Mining rose 4.7% amid critical minerals strength, Capstone Copper 4.3% and Firefly Metals 4.0% on copper gains, with Global X Copper Miners ETF up 3.1%. Predictive Discovery advanced 3.9%, Turaco Gold 3.8% on drilling updates, and Domino’s Pizza 3.1%.

Decliners included AUB Group down 17.8% after ceasing talks with EQT and CVC, Meteoric Resources off 12.5% on environmental license update, and Metcash sliding 9.2% post-half-year results. European Lithium fell 8.6%, Digico Infrastructure REIT 8.2% in downtrend, Cettire 7.8%, Australian Ethical Investment 7.7%, Temple & Webster 7.3% continuing AGM fallout, Energy One 7.2%, Aeris Resources 7.0%, HMC Capital 7.0%, and Vaneck Bitcoin ETF 6.1% on Bitcoin’s drop.

China’s November PMI showed manufacturing at 49.2 (in-line, still contracting) and non-manufacturing at 49.5 (below forecast, slipping into contraction), pressuring sentiment. OPEC kept output unchanged, supporting energy. Ahead, Wednesday’s Q3 GDP is forecast at +0.7% q/q and +2.2% y/y, potentially the fastest in three years, amid hot inflation and tight labor, with markets pricing 50-50 odds of an RBA hike late 2026. RBA Governor Bullock speaks Tuesday, and October household spending (+0.6% m/m forecast) follows Thursday.

Strategists eye sustained investment from last week’s capex surge of 11.5% q/q, strongest in over two decades, with intentions up. Building activity rose sharply, aiding GDP via housing push. Consumer spending strengthened per Westpac, with wealth effects from record home prices. However, low productivity caps potential growth at 2%, risking inflation if demand surges. HSBC’s Paul Bloxham calls for fiscal-monetary coordination to cool, or rates may rise sooner. Treasurer Chalmers signals budget savings mid-month. Overall, while resources buoyed Monday, heavier tech and financial drags dominated, but accelerating growth and seasonal factors could support rebound if data confirms resilience.