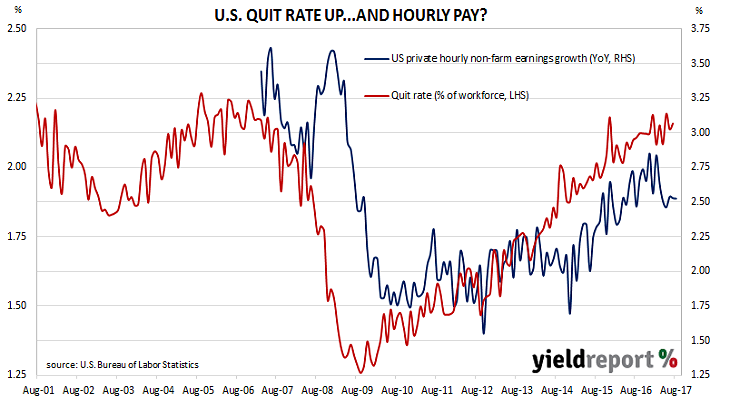

The quit rate time series produced by the Job Openings and Labor Turnover Survey (JOLTS) is a leading indicator of U.S hourly pay. As wages account for around 55% of a product’s or service’s price*, wage inflation and overall inflation rates tend to be closely related. Federal Reserve chief Janet Yellen is thought to pay close attention to the quit rate and she has referred to it in more than a few speeches.

Figures released as part of the July JOLTS report show the quit rate increased from 2.1% of the non-farm workforce at the end of June to 2.2% at the end of July. The increase was driven by quit rates in the durable goods manufacturing and health care sectors.

While the quit rate has trended up consistently since the depths of the U.S. recession in 2008/2009, the relationship with hourly pay rates has been more rubbery. Private hourly non-farm pay growth has tended to move in a “step” fashion and the 2.5% growth rate since April is an example of this. However, this situation is unlikely to remain indefinitely.