27 November 2024

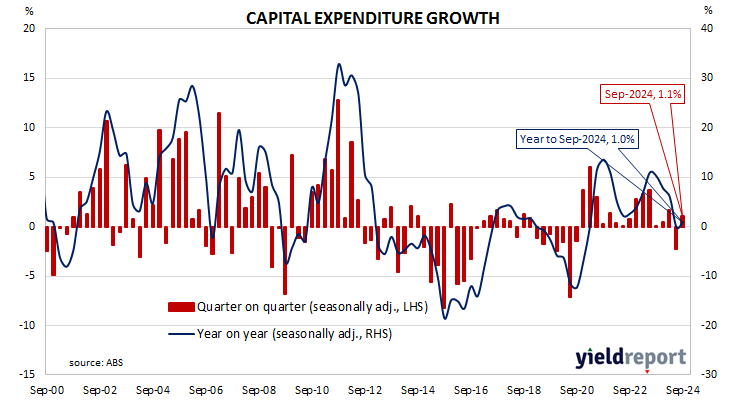

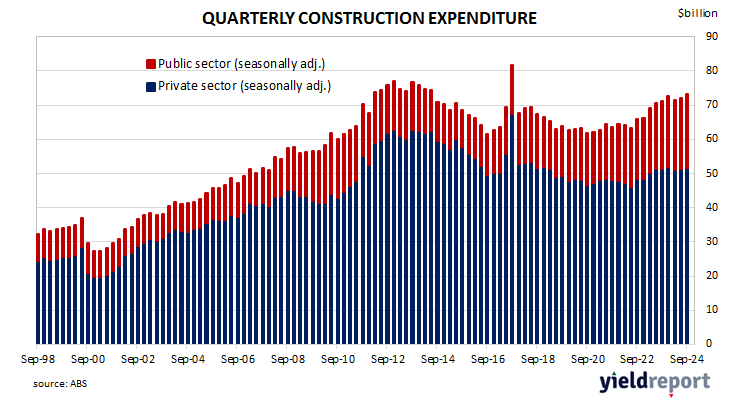

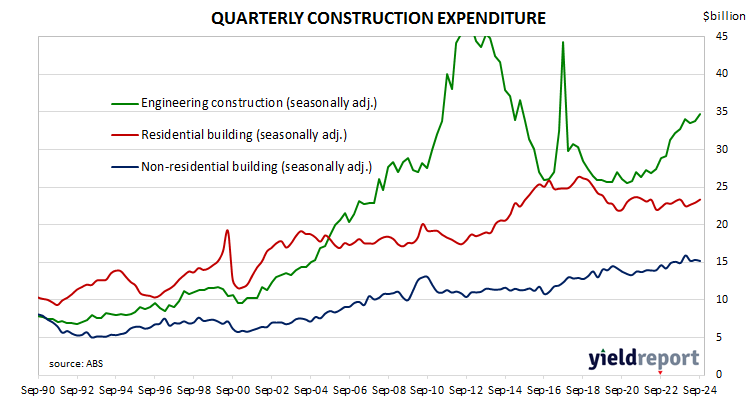

Summary: Construction spending up 1.6%, more than expected; up 3.2% from September 2023 quarter; Westpac: dynamics associated with Australian construction activity remain little changed; ACGB yields generally fall; rate-cut expectations soften; Westpac: public infrastructure works main driver behind growth in overall activity; residential sector up 1.8%, non-residential building down 1.0%, engineering up 2.6%.

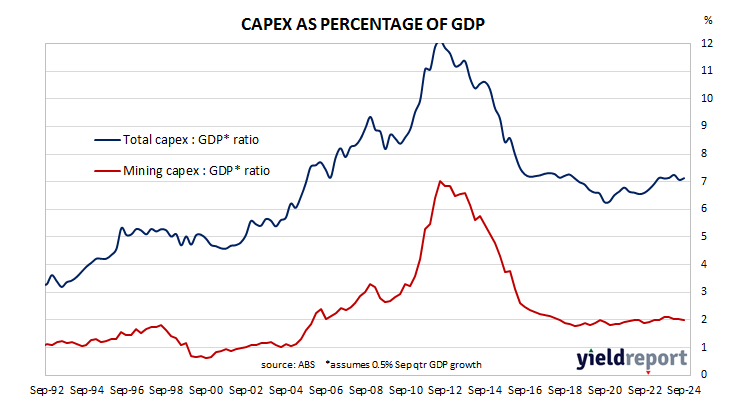

Construction expenditure increased substantially in Australia in the early part of last decade following a more-steady expansion through the 2000s. A large portion of the increase came from the commissioning of new projects and the expansion of existing ones to exploit a tripling in price of Australia’s mining exports in the previous decade.

According to the latest construction figures published by the ABS, total construction in the September quarter increased by 1.6% on a seasonally adjusted basis. The result was more than the 0.5% increase which had been generally expected as well as the June quarter’s 1.1% rise after revisions. On an annual basis, the growth rate increased from 2.4% to 3.2%.

“Despite the stronger quarterly result and upward revisions, the key dynamics associated with Australian construction activity remain little changed,” said Westpac senior economist Ryan Wells.

The figures came out at the same time as October CPI numbers and domestic Treasury bond yields generally fell with the exception of 20-year yields which corrected for the previous day’s outsized move. By the close of business, the 3-year ACGB yield had lost 2bps to 3.97%, the 10-year yield had shed 3bps to 4.43% while the 20-year yield finished 6bps higher at 4.76%.

Expectations regarding rate cuts in the next twelve months softened. Cash futures contracts implied an average of 4.33% in December, 4.295% in February and 4.13% in May. October 2025 contracts implied 3.88%, 46bps less than the current cash rate.

“The composition continues to emphasise the importance of public infrastructure works as the main driver behind growth in overall construction activity,” Wells added. “Both State and Federal Government budgets have boosted the construction project pipeline and have provided a floor underneath current and future activity.”

Residential building construction expenditures increased by 1.8%, up from the June quarter rise of 1.2% after revisions. On an annual basis, expenditure in this segment was 0.1% higher than the September 2023 quarter, in contrast with the June’s quarter’s 1.0% decrease.

Non-residential building spending decreased by 1.0%, in contrast with the previous quarter’s 0.9% rise. On an annual basis, expenditures were 1.7% higher than the September 2023 quarter, in line with the June quarter’s increase after revisions.

Engineering construction increased by 2.8% in the quarter, up from the 1.0% rise in the previous quarter. Spending on an annual basis in this segment was 6.0% higher than the September 2023 quarter, up from the June quarter’s comparable figure of 5.2% after revisions.

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature, unlike unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures which are next due in early September.