Summary: US producer price index (PPI) up 0.5% in September, greater than expected; annual rate increases to 2.2%; “core” PPI up 0.3%; NAB: trade services prices jump, driven by margins for retailers of hardware, building materials; long-term Treasury yields down significantly, 2-year yield up a little; 2024 rate-cut expectations soften; goods prices up 0.9%, services prices up 0.3%.

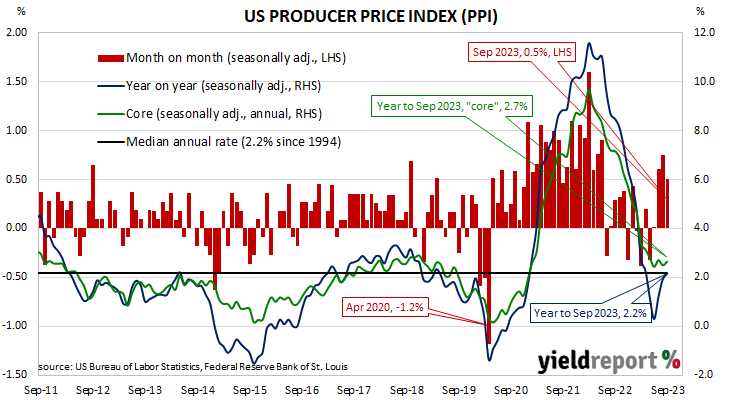

Around the end of 2018, the annual inflation rate of the US producer price index (PPI) began a downtrend which continued through 2019. Months in which producer prices increased suggested the trend may have been coming to an end, only for it to continue, culminating in a plunge in April 2020. Figures returned to “normal” towards the end of that year but were well above the long-term average through 2021, 2022 and the first quarter of 2023.

The latest figures published by the Bureau of Labor Statistics indicate producer prices increased by 0.5% after seasonal adjustments in September. The result was greater than the 0.3% rise which had been generally expected but less than August’s 0.7% increase. On a 12-month basis, the rate of producer price inflation after seasonal adjustments and revisions accelerated from August’s figure of 1.9% to 2.2%.

Producer prices excluding foods and energy, or “core” PPI, increased by 0.3% after seasonal adjustments. The result was more than the expected 0.2% increase as well as August’s 0.2%. The annual rate accelerated from 2.5% to 2.7% after revisions.

“There was a 7.0% annualized jump in the trade services component, which measures gross wholesale and retail margins, driven by a leap in margins for retailers of hardware, building materials,” said NAB Head of Market Economics, Tapas Strickland. “If you exclude trade services from core then PPI was bang in line at 0.2%.”

Long-term US Treasury bond yields fell significantly on the day while short-term yields increased modestly. By the close of business, the 2-year Treasury yield had added 2bps to 4.99%, the 10-year yield had shed 10bps to 4.56% while the 30-year yield finished 15bps lower at 4.69%.

In terms of US Fed policy, expectations of a lower federal funds rate in the next 12 months softened a little. At the close of business, contracts implied the effective federal funds rate would average 5.355% in November, 3bps more than the current spot rate, 5.385% in December and 5.405% in January. September 2024 contracts implied 4.92%, 41bps less than the current rate.

The BLS stated a 0.9% rise in final demand goods was the main factor in the overall increase. Prices of final demand services increased by 0.3%.

The producer price index is a measure of prices received by producers for domestically produced goods, services and construction. It is put together in a fashion similar to the consumer price index (CPI) except it measures prices received from the producer’s perspective rather than from the perspective of a retailer or a consumer. It is another one of the various measures of inflation tracked by the US Fed, along with core personal consumption expenditure (PCE) price data.