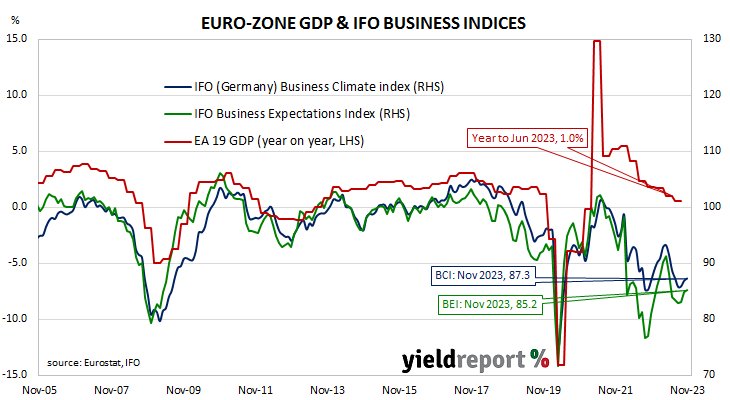

ifo business climate index rises in November, slightly below expected figure; German economy stabilising; current conditions index up, expectations index up; German, French 10-year yields slightly higher; expectations index implies euro-zone GDP contraction of 2.0% in year to February.

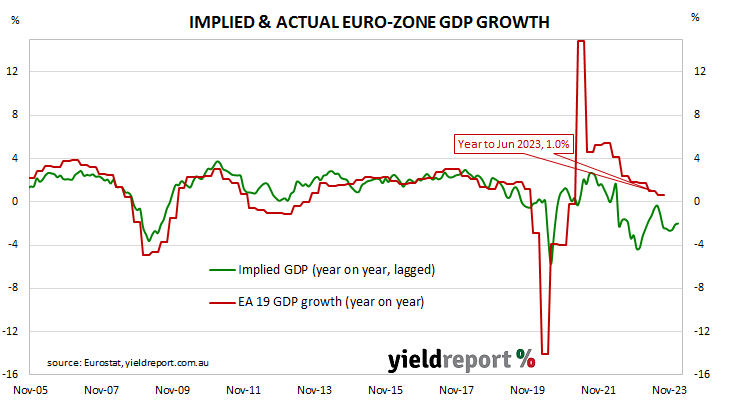

Following recessions in euro-zone economies in 2009/2010, the ifo Institute’s Business Climate Index largely ignored the European debt-crisis of 2010-2012, mostly posting average-to-elevated readings through to early-2020. However, the index was quick to react in the March 2020 survey, falling precipitously before recovering quickly in subsequent months. Readings through much of 2021 generally fluctuated around the long-term average before dropping away in 2022.

According to the latest report released by ifo, German business sentiment has improved for a third consecutive month. November’s Business Climate Index recorded a reading of 87.3, slightly below the generally expected figure of 87.5 but up from October’s final reading of 86.9. The average reading since January 2005 is 96.4.

“The German economy is stabilising, albeit at a low level,” said Clemens Fuest, President of the ifo Institute.

German firms’ views of current conditions and their collective outlook both improved. The current situation index crept up from October’s revised figure of 89.2 to 89.4 while the expectations index increased from 84.8 after revisions to 85.2.

German and French long-term bond yields finished a touch higher on the day. By the close of business, the German 10-year yield had added 2bps to 2.64% while the French 10-year OAT yield finished 1bp higher at 3.20%.

The ifo Institute’s business climate index is a composite index which combines German companies’ views of current conditions with their outlook for the next six months. It has similarities to consumer sentiment indices in the US such as the ones produced by The Conference Board and the University of Michigan.

It also displays a solid correlation with euro-zone GDP growth rates. However, the expectations index is a better predictor as it has a higher correlation when lagged by one quarter. November’s expectations index implies a 2.% year-on-year GDP contraction to the end of February.