Summary: Annual Inflation rate slows to 4.1% in December quarter, less than expected; RBA preferred measure slows from 5.1% to 4.2%; ACGB yields fall significantly; rate-cut expectations harden; alcohol & tobacco, housing main drivers of result.

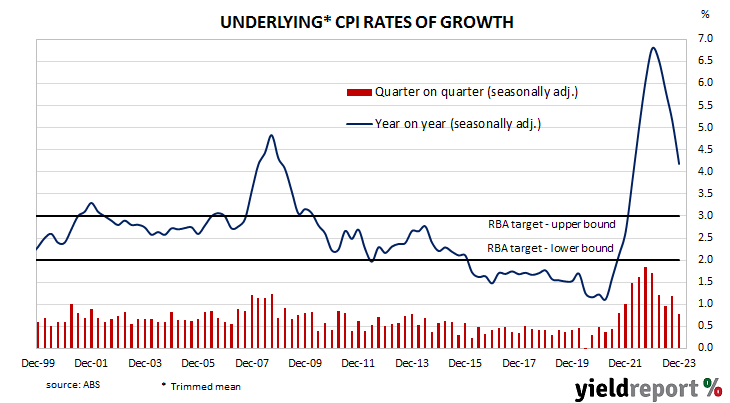

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

Consumer price indices for the December quarter have now been released by the ABS and the inflation rate posted a 0.6% rise before seasonal adjustments. The result was below consensus expectations of a 0.8% rise as well as the September quarter’s 1.2% increase. On a 12-month basis, the inflation rate slowed from 5.4% to 4.1%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 0.8% over the quarter, slightly less than the 0.9% increase which had been generally expected and noticeably lower than the September quarter’s 1.2% rise. The 12-month inflation rate slowed from 5.1% to 4.2%.

Domestic Treasury bond yields moved significantly lower on the day. By the close of business, the 3-year ACGB yield had shed 15bps to 3.54%, the 10-year yield had lost 13bps to 4.03% while the 20-year yield finished 12bp lower at 4.34%.

In the cash futures market, expectations regarding rate cuts later this year hardened. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.315% through February, 4.30% in March and 4.275% in April. However, August contracts implied a 4.015% average cash rate while November contracts implied 3.81%, 52bps less than the current rate.

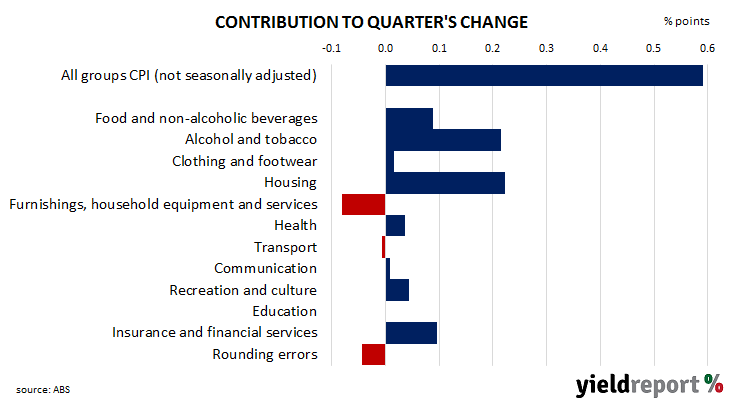

The main drivers of the headline inflation figure in the quarter were a 2.8% rise in alcohol and tobacco prices and a 1.0% rise in housing costs, each contributing just over 0.20 percentage points of the 0.6% (unadjusted) increase.

Here’s what a few economists said about the figures:

Catherine Birch, ANZ

The quarterly non-tradables print was still very strong, at 1.3% q/q, with the six-month annualised rate at 5.4%. Services inflation was still solid as well at 1.0% q/q. This will likely see the RBA maintain its tightening bias and hawkish tone in the February statement. Our base case remains that the cash rate has peaked at 4.35% but that cuts won’t begin until late this year. That said, risks might be starting to skew toward an earlier commencement of rate cuts. We doubt the RBA will signal this at its coming meeting, however.

Chris Read, Morgan Stanley Australia

This print is below RBA forecasts for both headline and core and suggests that their inflation path is likely to be revised down at their February meeting next week. This, alongside an extension of their forecast horizon to June 2026, could see a forecast achievement of their target midpoint, 2.5%. This should see a more balanced outlook from the RBA, although we still expect the bar for a broader pivot to easing to be relatively high; the RBA views policy as only modestly restrictive, fiscal policy will be supportive through 2H24 and there still looks to be some stickiness in CPI categories the RBA has flagged previously i.e. services, non-tradables.

Justin Smirk, Westpac

The global disinflationary impulse has arrived. For the first time in three years, the prices of globally traded goods declined. Tradable inflation fell by 0.4% over the quarter, to be 1.3% higher in annual terms. The prices of household goods, fuel, clothing all fell over the quarter.

Growth in some domestic prices continue to remain elevated, including the cost of dwelling construction, rents, and insurance. More broadly we are seeing growth in prices across market services slow. We expect this to continue as growth in the population eases; there will be less pressure on rental markets and the capital stock will catch up to the increase in labour, boosting labour productivity and reducing unit labour costs.