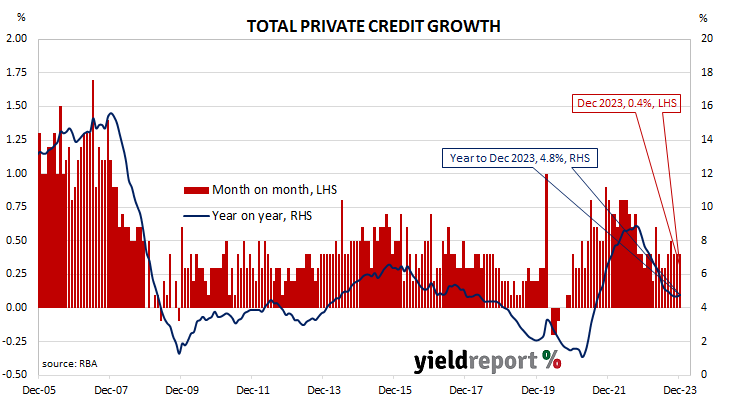

Private sector credit up 0.4% in December, in line with expectations; annual growth rate increases to 4.8%; Westpac: rounds out year of subdued growth; ACGB yields fall significantly; rate-cut expectations harden; owner-occupiers, business segments each account for around 45% of net growth.

The pace of lending growth in the non-bank private sector by financial institutions in Australia followed a steady-but-gradual downtrend from late 2015 through to early 2020 before hitting what appears to be a nadir in March 2021. That downtrend ended later in that same year and annual growth rates shot up through 2022, peaking in September/October before easing through 2023.

According to the latest RBA figures, private sector credit increased by 0.4% in December. The result was in line with consensus expectations as well as the previous two months’ growth. On an annual basis, the growth rate increased slightly from November’s figure of 4.7% to 4.8%.

“Private sector credit rose by a subdued 0.4% in the December quarter, rounding out a year of subdued growth,” said Westpac senior economist Andrew Hanlan. “This subdued credit growth occurred in an environment of elevated interest rates and a sluggish economy, as well as an economy operating at a high level of capacity, with unemployment still near historic lows and a housing market where demand is outstripping limited supply.”

The figures came out at the same time as the latest CPI report and Treasury bond yields moved significantly lower on the day. By the close of business, the 3-year ACGB yield had shed 15bps to 3.54%, the 10-year yield had lost 13bps to 4.03% while the 20-year yield finished 12bp lower at 4.34%.

In the cash futures market, expectations regarding rate cuts later this year hardened. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.315% through February, 4.30% in March and 4.275% in April. However, August contracts implied a 4.015% average cash rate while November contracts implied 3.81%, 52bps less than the current rate.

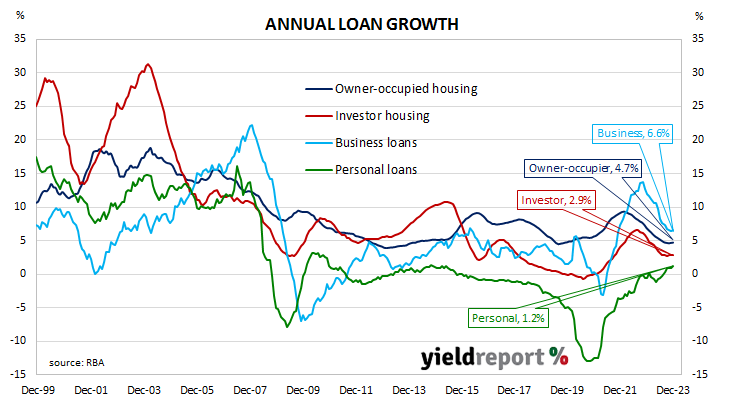

Owner-occupier lending and business lending each accounted for around 45% of the net growth over the month. Investor lending accounted for the balance.

The traditional driver of overall loan growth, the owner-occupier segment, grew by 0.4% over the month, in line with the previous five months. The sector’s 12-month growth rate ticked up from 4.6% to 4.7%.

Total lending in the non-financial business sector increased by 0.5%, the same as in the previous month after revisions. Growth on an annual basis picked up from 6.5% to 6.6%.

Monthly growth in the investor-lending segment slowed to a near-halt in early 2018 and essentially stayed that way until mid-2021. In December, net lending rose by 0.2%, down from 0.3%, maintaining the 12-month growth rate at 2.9%.

Total personal loans declined by 0.1%, in line with November’s contraction. However, the annual growth rate still accelerated from 0.9% to 1.2%. This category of debt includes fixed-term loans for large personal expenditures, credit cards and other revolving credit facilities.