Summary: RBA lowers GDP forecasts; underlying inflation forecasts reduced; jobless rise now expected earlier; headline inflation forecasts lowered; Westpac: domestic data weaker since December than assumed in November forecasts.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In November’s SoMP, the opening sentence of the “Outlook” section referred to slowing global growth which would remain “well below its historical average in the year ahead”, reflecting tighter monetary policy in advanced economies and a soft outlook for the Chinese economy.

As far as Australia was concerned at the time, “Growth in the Australian economy is expected to remain below trend over 2023 and 2024…But the economy has proved to be more resilient in recent quarters than previously expected, which is supporting demand conditions for Australian businesses.”

February’s “Global Outlook” stated the “overall outlook is little changed from three months ago, with stronger forecast growth in the United States and high-income economies in east Asia offset by weaker growth in some other advanced economies.”

From a domestic view, the SoMP stated “Economic growth is expected to remain subdued in the near term as inflation and earlier interest rate increases weigh on demand.”

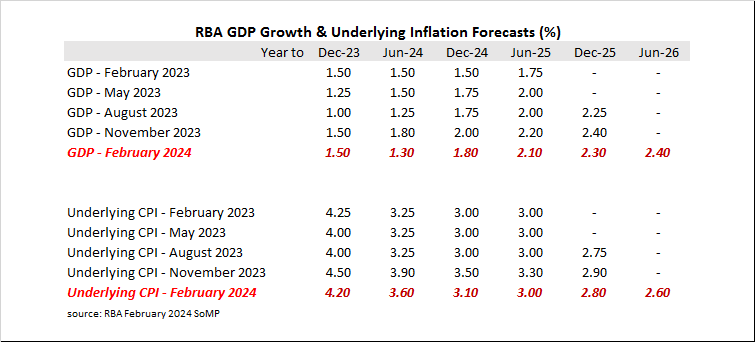

As a result, the RBA’s GDP growth forecasts for the year to June 2024 have been lowered by 0.50 percentage points while periods farther out have been trimmed by 0.10 or 0.20 percentage points.

“GDP growth is forecast to pick up gradually from later this year, largely reflecting stronger growth in household consumption and public demand.”

The RBA’s underlying inflation forecasts have also been lowered but not by enough to meet the RBA’s goal in the middle of its target range of 2%-3%. Despite the reduction in inflation forecasts, the RBA still expects to be only back at the top of this target range by mid-2025.

“Goods price inflation has declined more quickly than expected three months ago, as the earlier easing in global upstream costs was passed through to consumer-facing prices; domestic demand is also a little softer than previously anticipated.” However, “services inflation remains high and is expected to decline only gradually as domestic inflationary pressures moderate.”

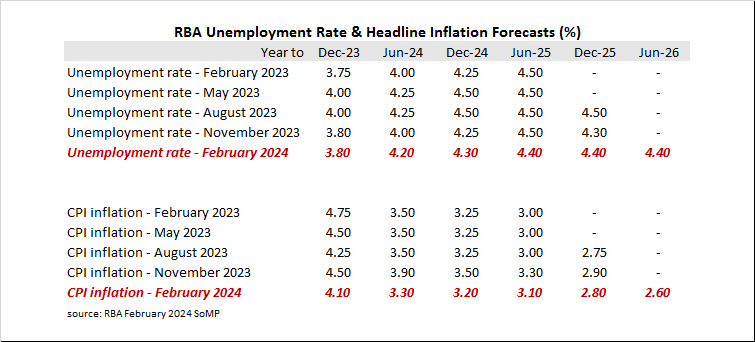

The RBA’s view of the unemployment rate typically follows from its forecasts of GDP growth. The unemployment rate has been fluctuating between 3.50% and 3.90% during 2023 but the RBA now expects it to rise to 4.20% by June 2024. Forecasts from November have been ratcheted back in this latest SoMP to be roughly in line with those of August.

“Both the broader hours-based underutilisation rate, i.e. people working fewer hours than they want, and the unemployment rate have increased since late 2022 when labour market conditions were very tight, and a further increase is expected over coming quarters in response to slower economic growth.”

Headline inflation forecasts have been reduced by 0.60 percentage points for the year to June 2024 and by 0.30 percentage points for the year to December 2024. Periods farther out have also been trimmed in a minor fashion.

“The recent decline in fuel prices will lower headline inflation in the March quarter this year; together with the scheduled expiry of government electricity rebates in 2024, this creates some volatility in the progress of headline inflation to target.”

The statement came out at the same time as the latest RBA policy decision and Commonwealth Government bond yields rose modestly on the day, lagging the large increases of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had added 2bps to 3.67% while 10-year and 20-year yields both finished 3bps higher at 4.14% and 4.44% respectively.

In the cash futures market, expectations regarding rate cuts later this year softened slightly. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.305% through March, 4.295% in April and 4.25% in May. However, August contracts implied a 4.125% average cash rate while November contracts implied 3.935%, 39bps less than the current rate.

“Since the last Board meeting in December, essentially all the domestic data have been weaker than assumed in the RBA’s November forecast round,” said Westpac Chief Economist Luci Ellis. “Consumer spending, investment and especially inflation all ended 2023 weaker than the RBA forecast. The narrative that inflation had become increasingly home-grown and demand-driven has become harder to sustain.”