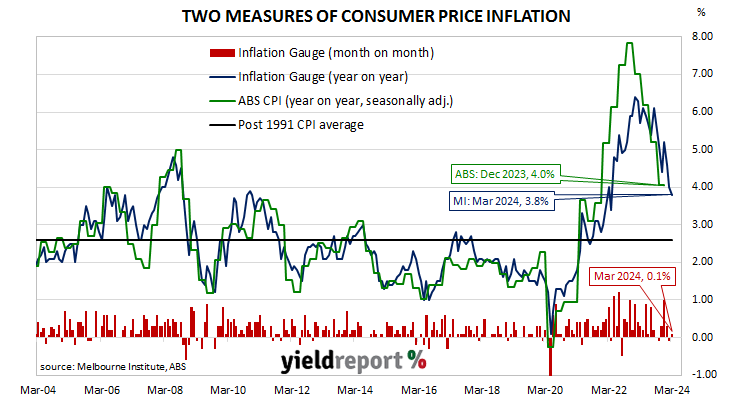

Melbourne Institute Inflation Gauge index up 0.1% in March; up 3.8% on annual basis; ACGB yields rise noticeably; rate-cut expectations soften.

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for as long as twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate the ABS rate by around 0.1%, or at least until recently.

The Melbourne Institute’s latest reading of its Inflation Gauge index indicates consumer prices increased by just 0.1% in March, following a fall of 0.1% in February and a 0.3% rise in January. The index rose by 3.8% on an annual basis, down from February’s comparable figure of 4.0%.

The update was released on the same day as ANZ’s latest Job Ads report and Commonwealth Government bond yields rose noticeably across the curve, largely in line with overnight rises of US Treasury yields. By the close of business, the 3-year ACGB yield had gained 7bps to 3.62% while 10-year and 20-year yields finished 10ps higher at 4.08% and 4.38% respectively.

In the cash futures market, expectations regarding rate cuts later this year softened. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.305% through May and 4.29% in June. However, August contracts implied a 4.20% average cash rate, November contracts implied 4.03%, while February contract implied 3.865%, 46bps less than the current rate.

Given the Inflation Gauge’s tendency to overestimate, the latest figures imply an official CPI reading of 1.0% (seasonally adjusted) for the March quarter or 3.7% in annual terms. However, it is worth noting the annual CPI rate to the end of March 2023 was 7.0% while the Inflation Gauge had implied a 5.7% annual rate at the time.