Summary: Annual Inflation rate slows to 3.6% in March quarter, more than expected; RBA preferred measure slows from 4.2% to 4.0%; ACGB yields jump; rate-cut expectations soften; education, health, housing, food main drivers of result.

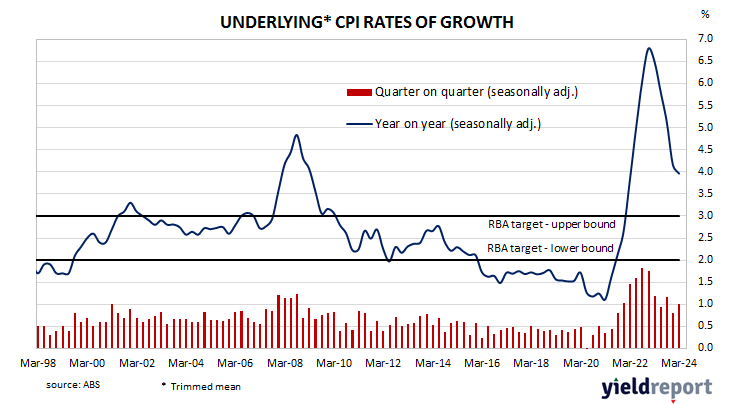

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

Consumer price indices for the March quarter have now been released by the ABS and the inflation rate came in at 1.0% before seasonal adjustments. The result was above consensus expectations of a 0.8% rise as well as the December quarter’s 0.6% increase. However, on a 12-month basis, the inflation rate still slowed from 4.1% to 3.6%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, also increased by 1.0% over the quarter, more than the 0.8% increase which had been generally expected and the December quarter’s 0.8% rise. The 12-month inflation rate slowed from 4.2% to 4.0%.

Domestic Treasury bond yields jumped on the day. By the close of business, the 3-year ACGB yield had gained 21bps to 4.04%, the 10-year yield had added 18bps to 4.46% while the 20-year yield finished 13bps higher at 4.70%.

In the cash futures market, expectations regarding rate cuts in the next twelve months softened significantly. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.32% through May and 4.325% in June. August contracts implied a 4.37% average cash rate, November contracts implied 4.325%, while May 2025 contracts implied 4.165%, 16bps less than the current rate.

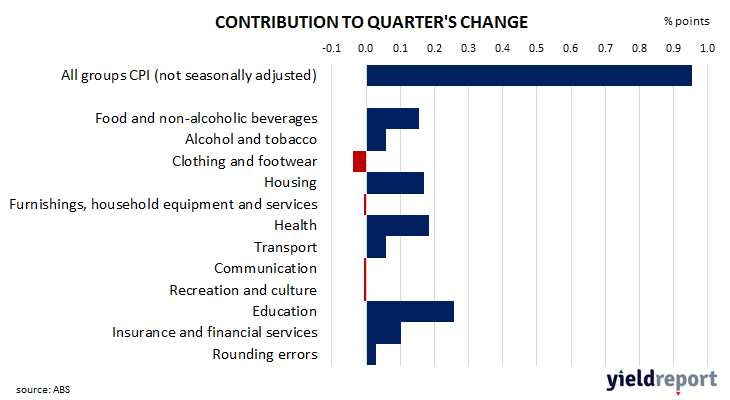

The main drivers of the headline inflation figure in the quarter were a 5.9% rise in education costs, with health, housing and food prices also making significant contributions.

Here’s what a few economists said about the figures:

Carlos Cacho, Jarden Australia

Overall inflationary pressures actually increased quarter on quarter, with 59% of the CPI basket seeing annualised price increases of greater than 4%, the highest since March 2023. Importantly for consumers, grocery price inflation moderated to 2.3% year on year, led by falling fresh food prices.

More broadly, whilst discretionary goods inflation continues to moderate, other key essential items remain elevated. Indeed, services remain the key driver of inflation, lifting to greater than 5% annualised but moderating to 4.3% year on year. Meanwhile, goods prices are around 2% annualised. Further, breaking CPI into four broad categories, we now see that the moderation in CPI has been driven largely by FX-sensitive imported consumer goods and temporary factors, whilst the persistent and labour-sensitive components remain elevated.

Catherine Birch, ANZ

We think the RBA will want to see a couple of quarters of lower non-tradables and services inflation to be convinced that overall inflation will not only return to the 2–3% target band but remain there. As such, non-tradables and services inflation will need to slow materially in Q2 for rate cuts to begin at the November meeting, which comes after the Q3 CPI data, barring a more significant deterioration in labour market and/or activity data.

One positive takeaway is that the diffusion index only picked up a little, suggesting the reacceleration in seasonally adjusted inflation was relatively contained rather than being broad-based.

Josh Williamson, Citi

Headline and underlying inflation beat consensus estimates of 0.8% in Q1, both rising by 1.0% over the quarter, while we had expected an increase of 0.9% for both. Inflation remains sticky across the services and housing sector, while regulated price rises are also not doing the RBA any favours.

Although inflation should decelerate in Q2, we still see a higher underlying inflation profile in 2024. High labour costs continue to pose upside risks to inflation. Consequently, we now see little hope that the RBA can cut policy rates in 2024. We remove our 25bp cut in November and push it out to February 2025.