Summary:

US CPI this week indicated cooling inflation. But it has done little to temper consumer concerns, with long-term inflation expectations, jumping by the most since 1993. And it capped off a volatile week on Wall Street that saw stocks sink into correction territory, giving the Fed and chair Powell plenty to digest for their decision this up coming week. But the big issue – growth concerns have come to the forefront.

The focus so far this year has been a reassessment of growth and it’s been a clear reassessment to the downside. Tariffs are bad for growth and bad for inflation, which puts the Fed in a bind. Bonds are reacting on the threat of inflation.

The US economy, both for consumers and for corporates, is in a wait-and-see situation. It does make sense that the soft data should eventually begin to spill over to at least some weakening in the hot data. The US economy is beginning to look like it needs or will justify a rate cut.

All this is impacting spreads. High Yield spreads have widened by the most in six months this past week, notwithstanding that they remain near historic lows. The flipside – meaning they could move out significantly more if a recession hits.

Goldman Sachs Group Inc. strategists have already sharply raised their forecasts for the risk premiums as tariff risks increase and the White House flags that it is willing to tolerate short-term pain in an attempt to address the trade deficit. They now expect high-yield spreads to reach 440 basis points in the third quarter compared with 295 basis points previously. Levels as of March 13 were 335 basis points.

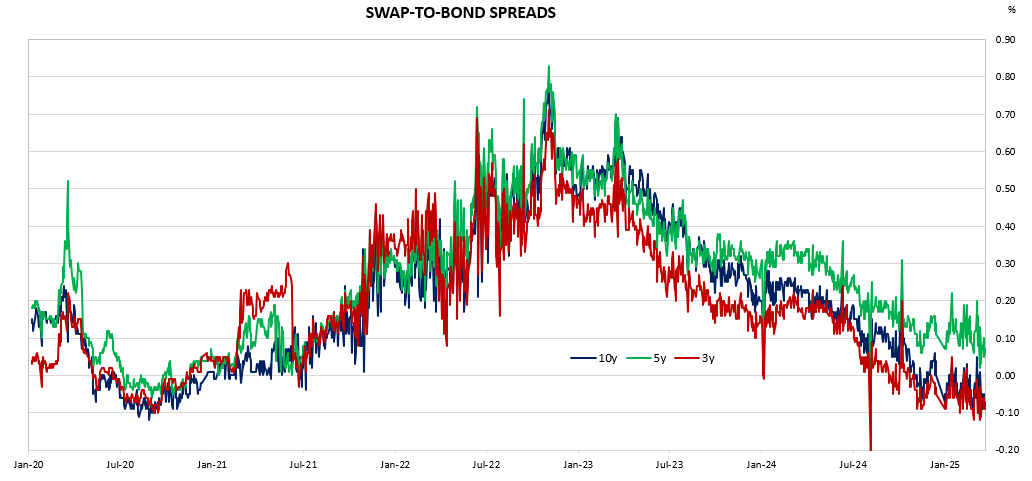

Figure 1 : Australian Corporate Bond Spreads