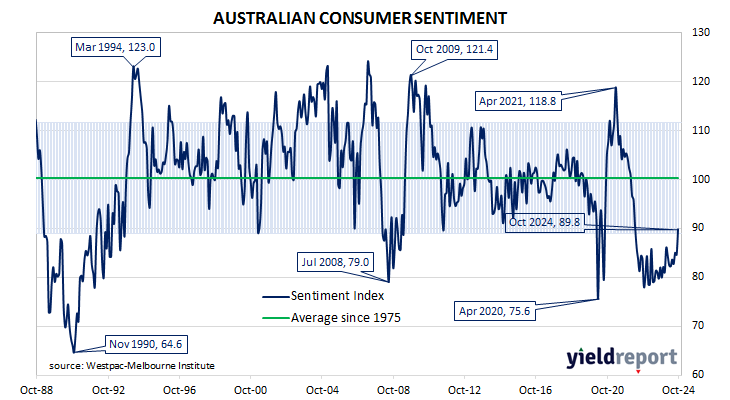

Summary: Westpac-Melbourne Institute consumer sentiment index rises in October; Westpac: best since RBA rate tightening phase began; ACGB generally fall; rate-cut expectations firm; Westpac: consumers no longer fearful RBA could take interest rates higher; all five sub-indices rise; fewer respondents expecting higher jobless rate.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again in mid-July 2018. Both measures then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery. However, consumer sentiment then weakened considerably and has languished at pessimistic levels since mid-2022 while business sentiment has been more robust.

According to the latest Westpac-Melbourne Institute survey conducted over the first week of October, household sentiment improved markedly, albeit to a level which is still on the pessimistic side. Their Consumer Sentiment Index jumped from September’s reading of 84.6 to 89.8, a reading which is significantly lower than the long-term average reading of just over 101 and at the lower bound of the “normal” range.

“This is the most promising update we have seen over the cycle to date,” said Westpac senior economist Matthew Hassan. “While pessimism still dominates, the October consumer sentiment read is the best since the RBA interest rate tightening phase began two and a half years ago.”

Any reading of the Consumer Sentiment Index below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic.

The figures came out on the same day as two other private sector surveys and Commonwealth Government bond yields generally fell, although ultra-long yields rose in what was probably a catch up from the previous day’s lack of movement. By the close of business, the 3-year ACGB yield had shed 7bps to 3.69%, the 10-year yield had lost 5bps to 4.17% while the 20-year yield finished 7bps higher at 4.56%.

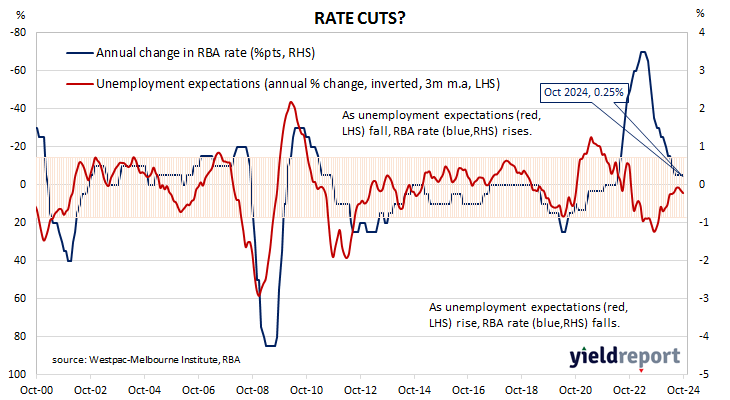

Expectations regarding rate cuts in the next twelve months firmed, with a February 2025 rate cut priced in as an 80% probability. Cash futures contracts implied an average of 4.315% in November, 4.245% in December and 4.175% in February 2025. September 2025 contracts implied 3.675%, 66bps less than the current cash rate.

“Expectations have been buoyed by interest rate cuts abroad and more promising signs that inflation is moderating locally,” Hassan added. “Consumers are no longer fearful that the RBA could take interest rates higher. However, responses around family finances suggest progress on cost-of-living pressures, the main source of negative sentiment reads overall, is still slow.”

All five sub-indices registered higher readings, with the “Economic conditions – next 12 months” sub-index posting the largest monthly percentage gain.

The Unemployment Expectations index, formerly a useful guide to RBA rate changes, fell from 138.4 to 129.8, essentially in line with the long-term average of 129.1. Lower readings result from fewer respondents expecting a higher unemployment rate in the year ahead.