Summary: RBA trims GDP forecasts out to June 2026; underlying inflation forecasts lowered slightly; jobless rate expected to rise slightly, stabilise in mid-4s in 2025; headline inflation forecasts generally reduced; ACGB yields rise; rate-cut expectations soften; Citigroup: fairly neutral overall.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

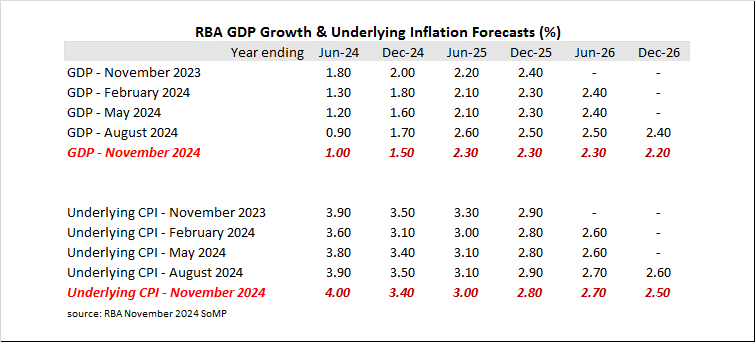

In August’s SoMP, the opening sentence of the “Global Outlook” section stated the overall outlook was little changed from that of May. “The 2024 forecast is a little higher than was forecast three months ago; the 2025 forecast remains unchanged.”

As far as Australia was concerned at the time, “The outlook for GDP growth in 2024 is similar to three months ago. Imports growth was much stronger than expected in the March quarter and this has offset a stronger near-term outlook for public demand and household consumption growth relative to three months ago.”

November’s “Global Outlook” is slightly more optimistic than August’s. “The outlook has been revised slightly higher relative to three months ago, as upward revisions to growth in China have been only partially offset by downward revisions to growth in New Zealand and India (for 2026).”

From a domestic view, this latest SoMP stated, “Growth in domestic demand is expected to pick up as growth in household consumption recovers and public demand continues to support activity.” The RBA noted this acceleration will take place a little later than it expected three months ago.

As such, the RBA’s GDP growth forecasts have all been trimmed by 0.20 percentage points with the exception of the year to June 2025 which was lowered by 0.30 percentage points.

“Higher interest rates have been working to bring demand and supply closer towards balance, with weak growth in private domestic demand in recent quarters partly offset by strong growth in public demand.”

The RBA’s underlying inflation forecasts have also been mostly reduced by modest amounts for all forecast periods with the exception of the year to June 2026. However, the RBA still expects inflation to move below the top of its target range by December 2025, as previously expected. Likewise, it is not expected to reach the middle of the band until December 2026, as before.

“Services inflation is projected to decline as the labour market softens. Housing inflation is also projected to moderate as nominal income growth eases, population growth slows and earlier constraints on housing construction ease. Goods inflation is forecast to remain at its current modest pace.”

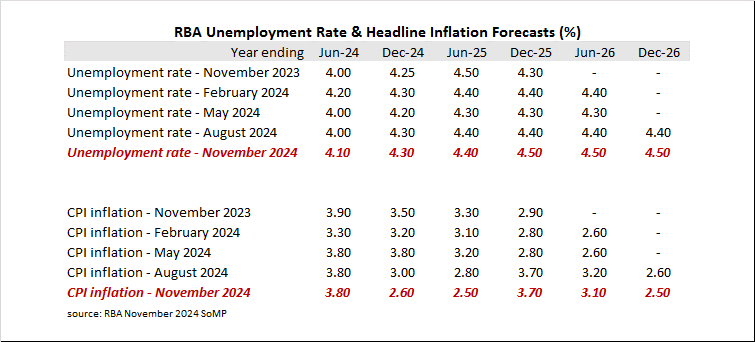

The RBA’s view of the unemployment rate typically follows from its forecasts of GDP growth. The unemployment rate has been fluctuating between 3.70% and 4.20% during 2024 and the RBA still expects it to rise modestly to 4.30% by the end of 2024 and then stabilise at a slightly higher level around 4.50% in 2025 and 2026.

“The unemployment rate is forecast to increase gradually over the coming year, consistent with subdued economic growth. While this assessment is little changed from the August Statement, the earlier easing in some labour market indicators has stalled recently and this presents some risk that labour market conditions ease by less than expected.”

Headline inflation forecasts have been lowered by 0.40 percentage points for the year to December 2024 and by 0.30 percentage points for the year to June 2025. Forecasts for periods further out have mostly been trimmed a little.

“Headline inflation will be below underlying inflation for a time due to temporary cost-of-living support to households. Following the end of these support measures, as legislated, headline inflation is expected to increase in the second half of 2025 to be outside the target range, before declining again to converge with measures of underlying inflation.”

The statement came out at the same time as the latest RBA policy decision and Commonwealth Government bond yields rose by declining amounts along the curve. By the close of business, the 3-year ACGB yield had gained 4bps to 4.08%, the 10-year yield had added 1bp to 4.58% while the 20-year yield finished unchanged at 4.90%.

Expectations regarding rate cuts in the next twelve months softened slightly, with a February 2025 rate cut now not viewed as especially likely. Cash futures contracts implied an average of 4.33% in November, 4.315% in December and 4.285% in February 2025. October 2025 contracts implied 3.925%, 41bps less than the current cash rate.

“The November SMP and Board Statement were fairly neutral, and only little changed from the previous iteration,” said Citigroup senior economist Faraz Syed. “However, the Board also judged that the demand and supply imbalance is improving and noted that the growth in household consumption, albeit continue to recover, will be slower compared to the August SMP.”