Summary: Business conditions deteriorate in November; business confidence slumps, well below long-term average; NAB: points to soft growth in Dec quarter; ACGB yields fall noticeably; rate-cut expectations harden; Westpac: update consistent with broader downward trend in businesses’ assessment of business conditions; capacity utilisation rate unchanged.

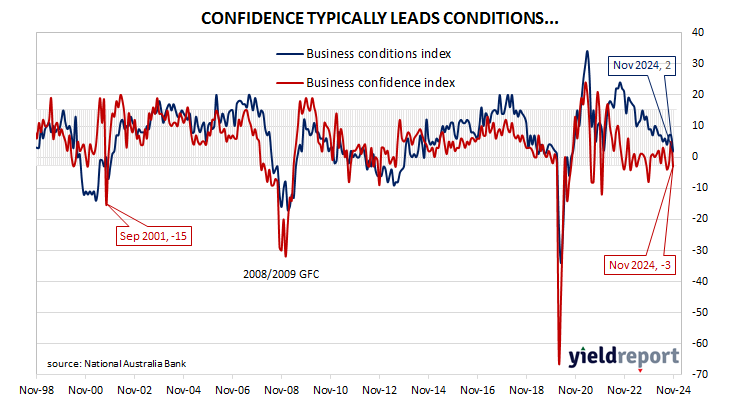

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s index then began to slip and forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 as the index trended lower. It hit a nadir in April 2020 as pandemic restrictions were introduced but then improved markedly over the next twelve months and subsequently remained at robust levels until recently.

According to NAB’s latest monthly business survey of around 350 firms conducted in the third week of November, business conditions have deteriorated noticeably to a level below the long-term average. NAB’s conditions index registered 2 points, down 5 points from October’s reading.

Business confidence also slumped. NAB’s confidence index dropped 8 points to -3 points, a reading which is well below its long-term average. NAB’s confidence index typically leads the conditions index by one month, although some divergences have appeared from time to time.

“Overall, the survey points to ongoing soft growth in Q4, though with capacity utilisation unchanged at an above-average level it will likely take more time for price pressures to fully normalise,” said NAB Head of Australian Economics Gareth Spence. “Indeed, price and cost growth indicators were broadly unchanged across the survey, though retail prices fell back to 0.6% in quarterly terms.”

The figures came out on the same day as the latest RBA monetary policy decision and Commonwealth Government bond yields fell noticeably across the curve. By the close of business, the 3-year ACGB yield had shed 8bps to 3.71% while 10-year and 20-year yields both finished 6bps lower at 4.15% and 4.50% respectively.

Expectations regarding rate cuts in the next twelve months hardened, with a February cut now viewed again as likely. Cash futures contracts implied an average of 4.265% in February, 3.945% in May and 3.6445% in August. November contracts implied 3.505%, 83bps less than the current cash rate.

“While recent NAB business survey updates had given some hope that Australian businesses might be turning more optimistic, the latest survey’s update for November was more consistent with the broader downward trend in their assessment of business conditions seen since early 2022,” noted Westpac senior economist Mantas Vanagas. “That resulted in more pessimism about the future economic outlook.”

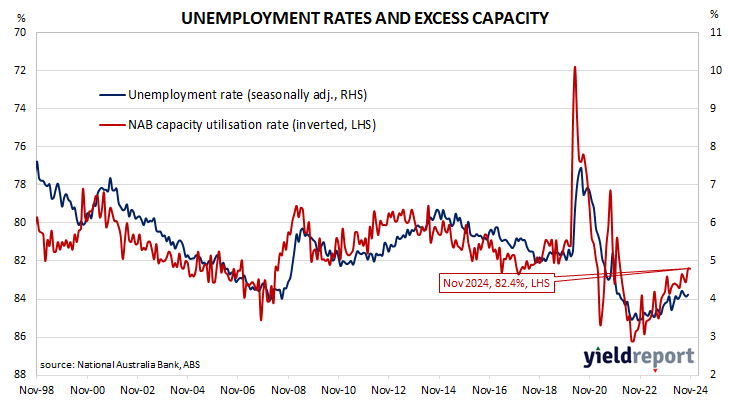

NAB’s measure of national capacity utilisation remained unchanged from October’s revised reading of 82.4%, a level which is still quite robust from a historical perspective. Five of the eight sectors of the economy were reported to be operating at or above their respective long-run averages.

Capacity utilisation is generally accepted as an indicator of future investment expenditure and it also has a strong inverse relationship with Australia’s unemployment rate.