Summary: Leading index growth rate declines in December; Westpac: growth signal not particularly strong but a clear improvement on past two years; reading implies annual GDP growth of around 2.75%-3.00%; ACGB yields generally rise moderately; rate-cut expectations soften; Westpac: more positive growth signal still looks fairly tentative.

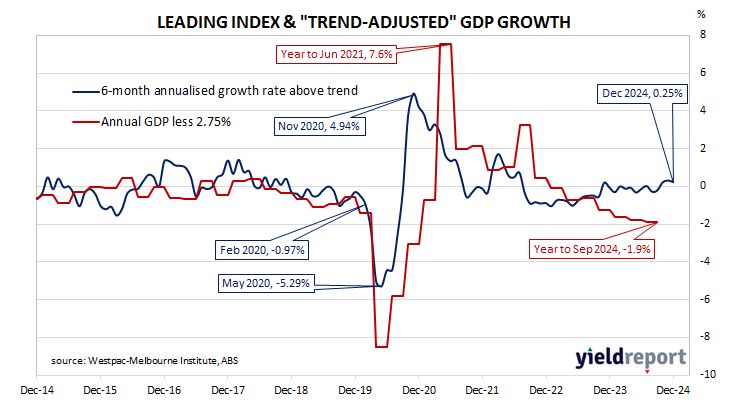

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic growth in the short-term. After reaching a peak in early 2018, the index trended lower through 2018 and 2019 before plunging to recessionary levels in the second quarter of 2020. Subsequent readings spiked towards the end of 2020 but then trended lower through 2021 and 2022 before flattening out in 2023 and 2024.

December’s reading has now been released and the six month annualised growth rate of the indicator registered 0.25%, down from November’s revised figure of 0.33%. The index reading represents a rate relative to “trend” GDP growth, which is generally thought to be around 2.50% to 2.75% per annum in Australia.

“While the growth signal is still not particularly strong, it has shown a clear improvement on the persistently negative, below-trend reads recorded over the previous two years,” said Westpac Head of Australian Macro-Forecasting Matthew Hassan.

Westpac states the index leads GDP growth by “three to nine months into the future” but the highest correlation between the index and actual GDP figures occurs with a three-month lead. The current reading may therefore be considered to be indicative of an annual GDP growth rate of around 2.75% to 3.00% in the next quarter.

Treasury bond yields rose moderately across the curve on the day. By the close of business, 3-year and 10-year ACGB yields had both gained 5bps to 3.91% and 4.49% respectively while the 20-year yield finished 4bps higher at 4.91%.

Expectations regarding rate cuts in the next twelve months softened slightly, although a February cut is still currently viewed as more likely than not. Cash futures contracts implied an average of 4.27% in February, 4.005% in May and 3.775% in August. December contracts implied 3.64%, 70bps less than the current cash rate.

“Commodity prices and financial markets face significant risks around global trade and geopolitics,” Hassan said. “Meanwhile locally, the consumer and housing sectors face ongoing uncertainty about the timing and scale of a prospective interest rate easing. All up, the more positive growth signal still looks fairly tentative.”

The RBA’s November Statement on Monetary Policy GDP growth forecasts are slightly higher than Westpac’s latest numbers, which are 1.3% for calendar year 2024 and 2.2% for calendar year 2025. The RBA forecasts GDP growth for the years ending December 2024 and December 2025 to be 1.5% and 2.3% respectively.