Summary: Conference Board leading index down 0.1% in December, in line with expectations; CB: half of ten index components down, half up; US Treasury yields rise; rate-cut expectations soften; CB: signals fewer headwinds to US economic activity ahead.

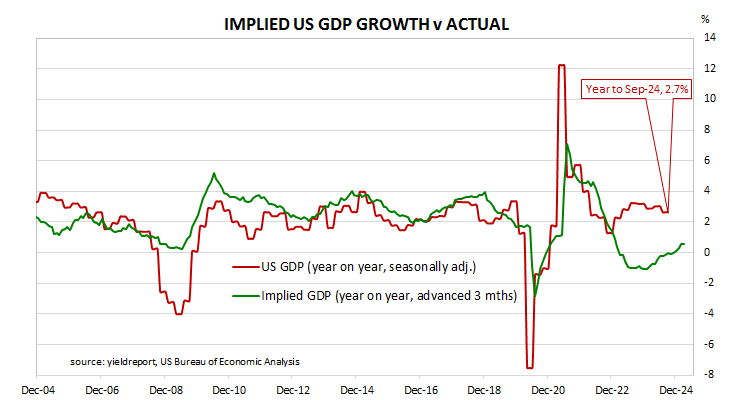

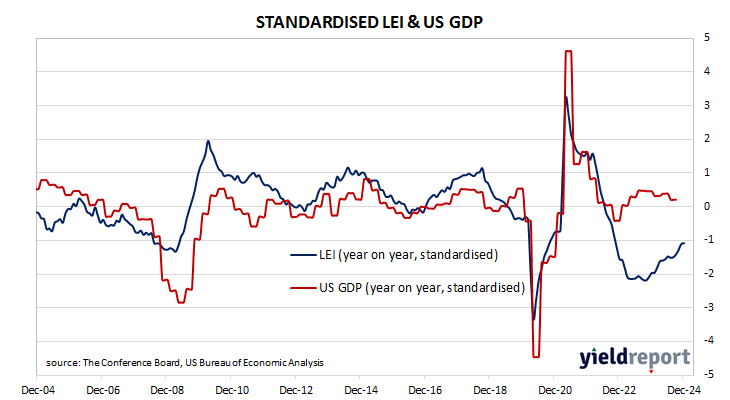

The Conference Board Leading Economic Index (LEI) is a composite index composed of ten sub-indices which are thought to be sensitive to changes in the US economy. The Conference Board describes it as an index which attempts to signal growth peaks and troughs; turning points in the index have historically occurred prior to changes in aggregate economic activity. Readings from March and April of 2020 signalled “a deep US recession” while subsequent readings indicated the US economy would recover rapidly. Post-2022 readings implied US GDP growth rates would turn negative but that has not been the case so far.

The latest reading of the LEI indicates it decreased by 0.1% in December. The decline was in line with expectations but in contrast with November’s upwardly-revised 0.4% increase.

“Low consumer confidence about future business conditions, still relatively weak manufacturing orders, an increase in initial claims for unemployment and a decline in building permits contributed to the decline,” said Justyna Zabinska-La Monica of The Conference Board. “Still, half of the ten components of the index contributed positively in December.”

US Treasury bond yields rose almost-uniformly across the curve on the day. By the close of business, the 2-year Treasury yield had added 3bps to 4.30%, the 10-year yield had gained 4bps to 4.60% while the 30-year yield finished 3bps higher at 4.82%.

In terms of US Fed policy, expectations of a lower federal funds rate in the next 12 months softened slightly, although one 25bp cut is currently priced in along with a solid chance of another one. At the close of business, contracts implied the effective federal funds rate would average 4.325% in February, 4.30% in March and 4.27% in April. December contracts implied 3.95%, 38bps less than the current rate.

“Moreover, the LEI’s six-month and twelve-month growth rates were less negative, signalling fewer headwinds to US economic activity ahead,” added Zabinska-La Monica. “Nonetheless, we expect growth momentum to remain strong to start the year and US real GDP to expand by 2.3% in 2025.”

Regression analysis suggests the latest reading implies a 0.6% year-on-year growth rate in March, up from the 0.5% year-to-February growth rate after revisions.