Summary: ACGB yields fall; ACGB 10-year spread to US Treasury yield falls to -12bps; 10-year bond yields steady in US, mixed in major European markets; $1.9 billion of bonds issued by AOFM.

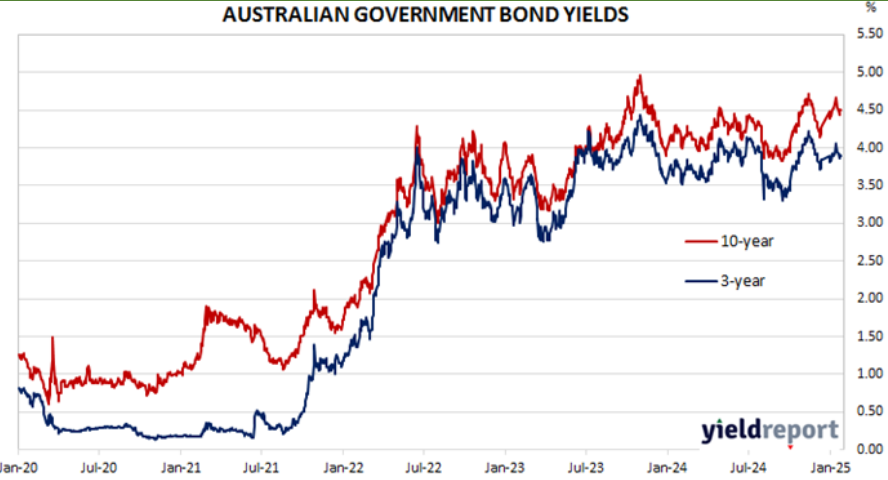

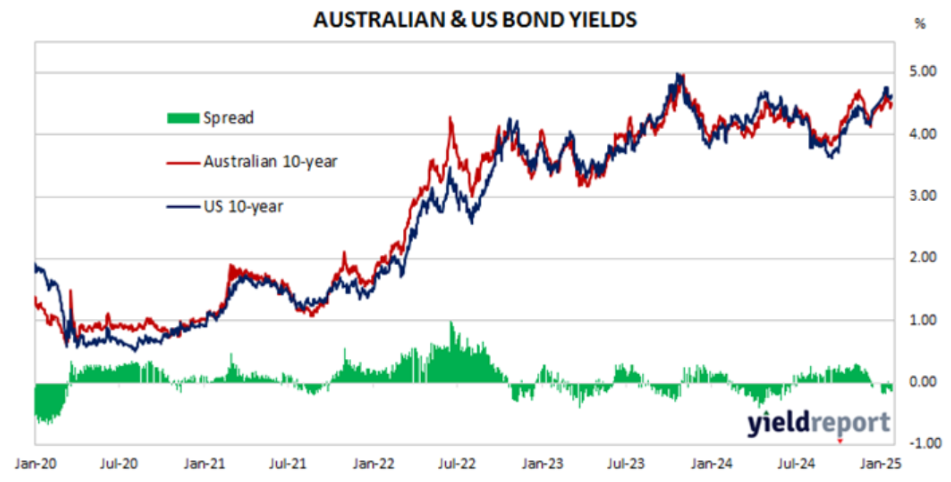

Locally, long-term ACGB yields remained fell for the first two days of the week, then reversed course and rose modestly on each of the three remaining days. By the end of the week, the 3-year ACGB yield had shed 5bps to 3.90%, the 10-year yield had lost 2bps to 4.51% while the 20-year yield finished 4bps lower at 4.92%. The spread between US and Australian 10-year Treasury bond yields fell 2bps to -12bps.

Over in the US, 10-year bond yields started its shortened week with a moderate fall which was reversed over the following two days. Yields then declined slightly at the end of the week.

The Conference Board’s December reading of its Leading Index was the first notable report for the shortened US week and it came out on Wednesday. The index posted a modest decline but the authors noted “fewer headwinds to US economic activity ahead…”

S&P Global’s January flash reading of its US composite index were released at the end of the week. The composite index dropped from 55.4 in December to 52.4. The manufacturing index increased from 49.4 to 50.1 while the services index fell from 56.8 to 52.8. “Although output growth slowed slightly in January, sustained confidence suggests that this slowdown might be short-lived.”

The New York Fed’s Nowcast model was also updated as usual. The December 2024 quarter forecast remained unchanged at 2.6% (annualised) while the March 2025 quarter forecast remained unchanged at 3.0% (annualised).

By this point, the US 2-year Treasury bond yield had slipped 1bp to 4.27%, the 10-year yield had returned to its starting point at 4.63% while the 30-year yield finished 1bp lower at 4.85%.

In major euro-zone markets, 10-year bond yields followed a vaguely-similar pattern to their US counterpart.

S&P Global released its January flash PMI figures for the euro-zone at the end of the week. The preliminary reading of the composite index was 50.2, up from December’s final reading of 49.6. ““The kick-off to the new year is mildly encouraging. The private sector is back in cautious growth mode after two months of shrinking. The drag from the manufacturing sector has eased a bit, while the services sector continues to grow moderately.”

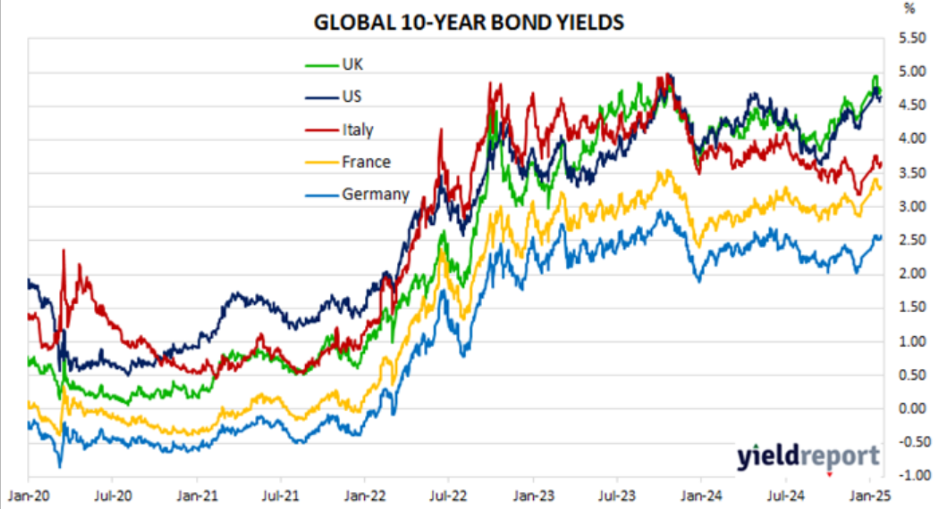

By this point, the German 10-year bund yield had gained 4bps to 2.57% while the French 10-year bond yield had slipped 1bp to 3.30%. The Italian 10-year BTP yield added 2bps to 3.66% over the week while the British 10-year gilt yield finished 3bps lower at 4.73%.

The AOFM held three vanilla bond tenders and one index-linked bond (ILB) tender this week. $300 million of June 2034s, $800 million of June 2035s and $700 million of June 2031s were priced at nominal yields of 4.47%, 4.47% and 4.21% respectively while the $100 million of November 2032 ILBs were priced at a real yield of 2.06%. There were also two Treasury note tenders which raised $3.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $52.40 billion. There are currently $847.05 billion of Treasury bonds and $42.785 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2025 when $41.50 billion worth of bonds are due. There are also $36.00 billion of short-term Treasury notes outstanding.