| Close | Previous Close | Change | |

|---|---|---|---|

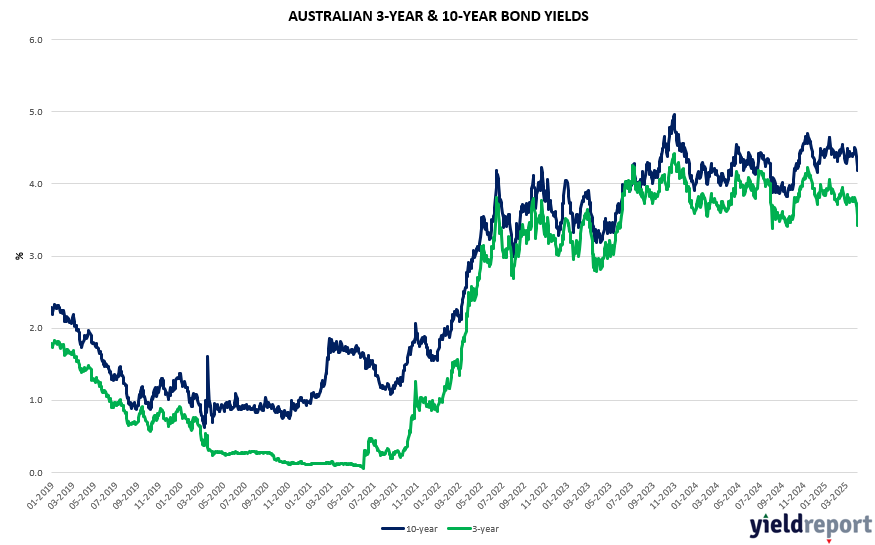

| Australian 3-year bond (%) | 3.254 | 3.362 | -0.108 |

| Australian 10-year bond (%) | 4.350 | 4.215 | 0.135 |

| Australian 30-year bond (%) | 5.063 | 4.897 | 0.166 |

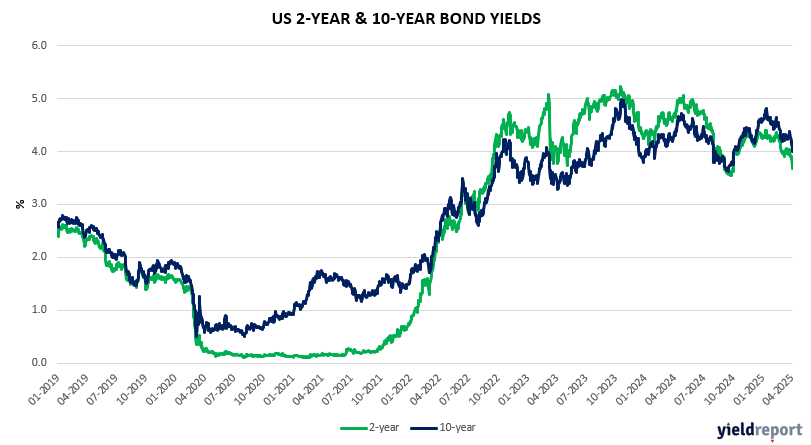

| United States 2-year bond (%) | 3.773 | 3.703 | 0.070 |

| United States 10-year bond (%) | 4.372 | 4.310 | 0.062 |

| United States 30-year bond (%) | 4.850 | 4.801 | 0.049 |

LOCAL BOND MARKETS

Australia’s 10-year government bond yield jumped an extraordinary 23 bps to 4.44%. Since Monday, the yield has increased 40 bps. Why? Well the Australian market is simply following the US market, because it certainly has nothing to do with reset monetary policy expectations here in Australia. And it is not like Australia risks stagflation like the US.

What is making more sense is the front end of the curve. The more policy sensitive 1-year, 2-year, and 3-year continue to notch up material declines in yields with the market having reset RBA interest rate expectations.

As for the baffling Monday and Tuesday moves in US bonds, traders have posited an array of reasons for Monday’s whiplash: a market primed for a pullback after such a sharp rally; lurking concerns about tariffs stirring inflation or necessitating government stimulus; liquidations in favour of cash-like instruments; and rumours that foreign owners, including China, were selling. We would posit another one – rebalancing of portfolios away from US assets. Most concerningly, this could be an early sign that investors are looking to liquidate positions even in high-quality assets to raise cash. That seems to be what has been happening with gold over the last several days.

As we noted on Tuesday regarding reset monetary policy expectations, Deutsche Bank is the first forecaster to call for a 50 bps cut by the RBA in May. “Unless the US administration tilts to an ‘off ramp’ within days on its tariff policy, we expect the RBA to lower rates by 50 bps in May,” Phil O’Donoghue, chief economist for Australia at Deutsche Bank. “We then expect another 50 bps of cuts in the second half (25 bps at each of the August and November meetings), taking the cash rate to 3.1% by the end of 2025.” The shift comes as markets are pricing in a 25% chance of an outsized, 50 bps cut at the RBA’s next meeting on May 20. Money markets are fully priced for a standard 25 bps move.

As for the market, it is now ascribing a 15% probability of a 50 bps cut at the May meeting. The market significantly repriced rate expectations on Monday, now fully priced for a 25 bps easing at each of the RBA’s next policy meetings in May, July and August, and expect even more will follow later in the year. A few market participants have even suggested the RBA may make an out of cycle rates decision. When certain market players start talking about inter-meeting rate cuts, you know things are truly breaking down.

RBA Gov Bullock’s speech on Thursday (at 8pm AEST) will get great attention and ironically a hawkish stance could feasibly accelerate the selling in the AUD.

US BOND MARKETS

Prior to lunch time US time, there was a debate on what would convince the US Administration to opt for some type of pause on tariffs. Would it be Congress, the President’s advisors, business leaders, the legal system, markets, or something else? We got the answer today: It’s the government bond market — particularly, how close it gets to the line that separates wild price volatility from market malfunctioning.

Anyone that thinks the cratering of the bond markets over the last few days did not at least precipitate this announcement would be naïve. There is a golden rule in the financial market – no one gets to stuff with the bond markets. And we are not just talking about the range of more arcane trades that were going heavily awry as from Monday and were no doubt risking investment strategy blow ups. You can’t make unfunded tax cuts if your treasury market is in flux because Trump just gave up on tariffs funding the tax cuts. To make an argument for unfunded tax cuts, well you need a compliant treasury market.

Various investment houses have now wound back recession calls. Reflective of calls, Torsten Slok, Apollo’s chief economist stated “I do think that recession risk has been removed now. It looks like now we have a more steady pace of negotiations coming.” Not so quick, we think. The vast majority of recesssions in US have been started by the business sector reducing spend. Today’s announcement is not going all of sudden to convince businesses to start spending.

In terms of bonds, the back end of the curve hardly moved. The front end had massive moves. The 10-year +3 bps to 4.34%. The 2-year +20 bps to 3.94%. In the 2-year, it was the biggest intraday surge since March of 2023. That was of course during the regional-bank turmoil in the US.

High yield markets breathed a huge sigh of relief after the tariff news, with ETFs in the asset class surging. The biggest high-yield bond ETFs — JNK and HYG — and the largest leveraged loan fund — BKLN –rallied by the most since November 2022.