| Close | Previous Close | Change | |

|---|---|---|---|

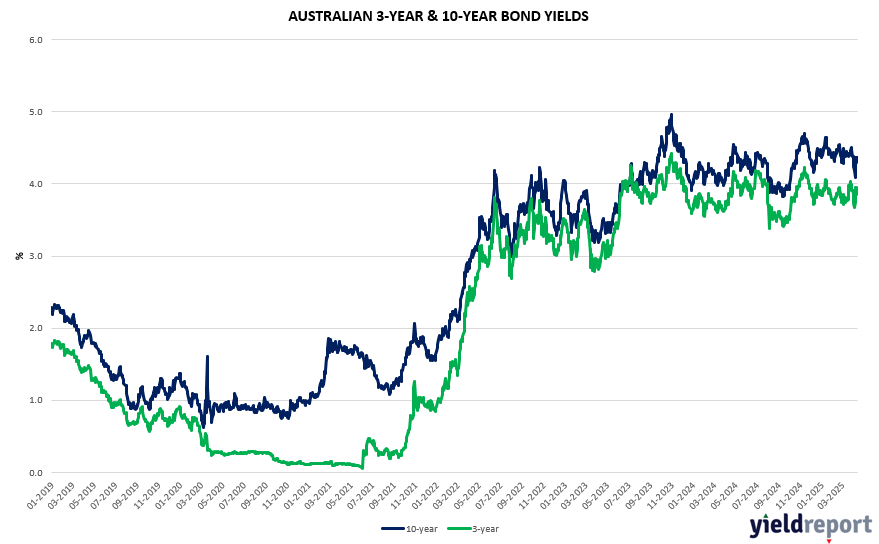

| Australian 3-year bond (%) | 3.353 | 3.376 | -0.023 |

| Australian 10-year bond (%) | 4.310 | 4.370 | -0.060 |

| Australian 30-year bond (%) | 5.012 | 5.082 | -0.070 |

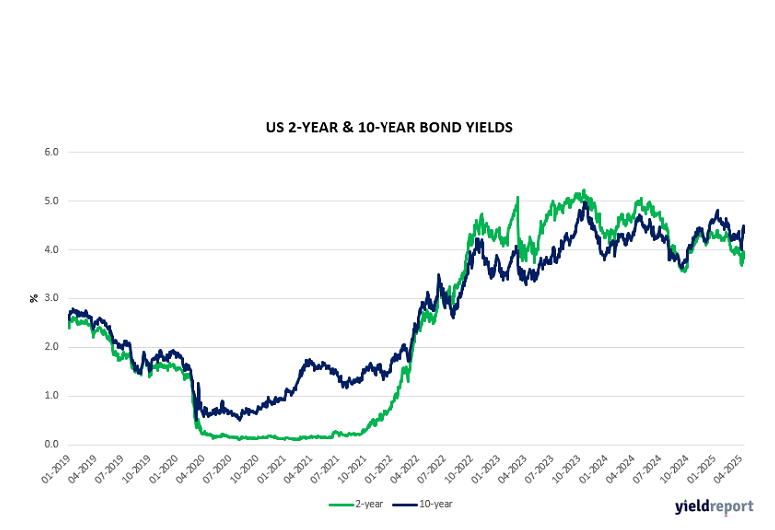

| United States 2-year bond (%) | 3.826 | 3.927 | -0.100 |

| United States 10-year bond (%) | 4.335 | 4.466 | -0.131 |

| United States 30-year bond (%) | 4.788 | 4.860 | -0.072 |

LOCAL BOND MARKETS

Australia’s 10-year government bond yield dropped 4 bps to 4.31% as investors assessed the Reserve Bank of Australia’s meeting minutes. The April minutes of the RBA meeting was released on Tuesday. The RBA flagged that interest rates could be cut again in May after the federal election, once it has the latest information on inflation and Donald Trump’s trade war. The RBA’s preferred measure of underlying inflation is likely to decline below 3% in the March quarter, when the consumer price index is published on April 30, according to the minutes.

However, the RBA also pointed to both economic and inflation risks, cautioning against premature policy easing. While the labor market remains tight, wage growth could slow. The board sees the May meeting as crucial for reassessing policy, but it remains too early to determine the next rate move. With global uncertainties, particularly concerning US tariffs, risks to growth have shifted to the downside. Markets are pricing in a 25-basis point cut in May and anticipate around 120 basis points of easing this year. Investors are now waiting for jobs data to gain further insight into labour market conditions.

US BOND MARKETS

US government debt rallied slightly and across the curve on Tuesday, erasing declines after a Treasury Department official said a rule change was under consideration that could lower trading costs for banks. The US 10-year was down 4 bps to 4.34%, the US 3-year down 2 bps to 3.86%.

While the rule change mentioned by Deputy Treasury Secretary Michael Faulkender has been on the radar for years, his comments on the Supplementary Leverage Ratio, or SLR, helped drive yields lower to levels last seen during last week’s market turmoil.

Investors also were motivated to buy longer-maturity Treasury debt at yield levels that offer the most compensation, relative to shorter-maturities, in more than a decade. The term premium increased to 71 basis points, last seen in September 2014. Term premiums have been on the rise as US economic policy becomes harder to predict. A gauge of policy uncertainty neared a record this month after President Donald Trump announced sweeping tariffs and then backtracked on some. Proposals for tax cuts and a potential need to increase the US government debt limit also contributed to the move.

Many market watchers last week suggested that foreign powers including China were offloading their US Treasury holdings in retaliation for Trump’s tariffs, exacerbating the plunge in prices. But Ed Yardeni, the noted US economist, released a detailed note yesterday indicating the vast majority of selling had come from forced selling by hedge funds.

Meanwhile, higher Treasury yields are failing to support the value of the US dollar as they have historically. The relationship between the dollar and Treasury yields is the weakest in three years as investors question the dollar’s haven status. Options positioning shows show that traders expect more losses for the dollar. The moves last weak were highly unusual and in an interview yesterday, Jenet Yellen stated that she believed the move in the USD last week was a sign of foreign asset selling. But there is a ton of narratives out in the markets about last weeks move.

Meanwhile, in the corporate bond market, lowly rated high yield companies have failed to sell any debt in the US high-yield bond market since Trump unleashed market turmoil and raised fears of a US recession with the wave of tariffs he announced earlier this month. Wall Street banks face potential losses on billions of dollars of short-term loans they had committed to in the expectation that junk-bond investors would ultimately take on the debt. But banks can be wrong-footed if the interest rate they have agreed to provide differs sharply from market levels, as can be the case in times of stress. The market sell-off comes as the private equity industry – and the banks that have long profited from their deals – struggles with a drop-off in dealmaking and fading hopes of a revival amid a looming threat of a recession.

High yield credit spreads have eased slightly, now at 410 bps. Last week they shot to the highest level in nearly two years last week, hitting 4.61bps before retreating slightly after Trump agreed to pause some tariffs. Goldman Sachs last week raised its forecast for defaults by high-yield and leveraged loan borrowers this year to 5% and 8% respectively, up from 3% and 3.5%.