| Close | Previous Close | Change | |

|---|---|---|---|

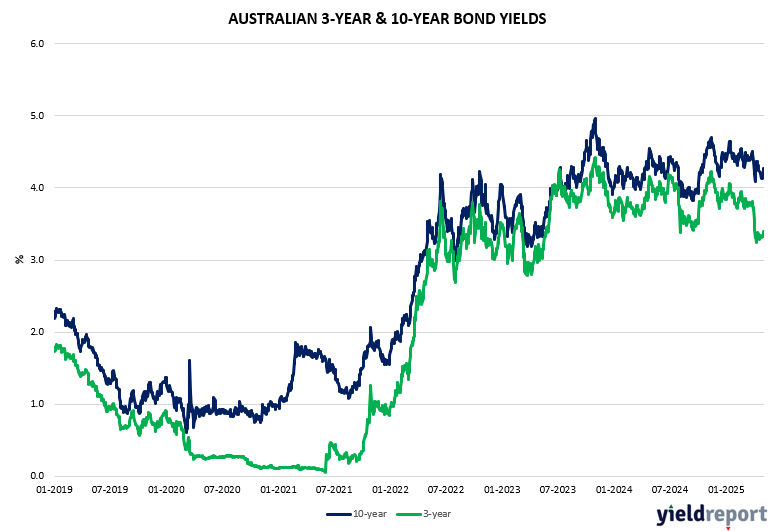

| Australian 3-year bond (%) | 3.393 | 3.328 | 0.065 |

| Australian 10-year bond (%) | 4.274 | 4.165 | 0.109 |

| Australian 30-year bond (%) | 4.93 | 4.891 | 0.039 |

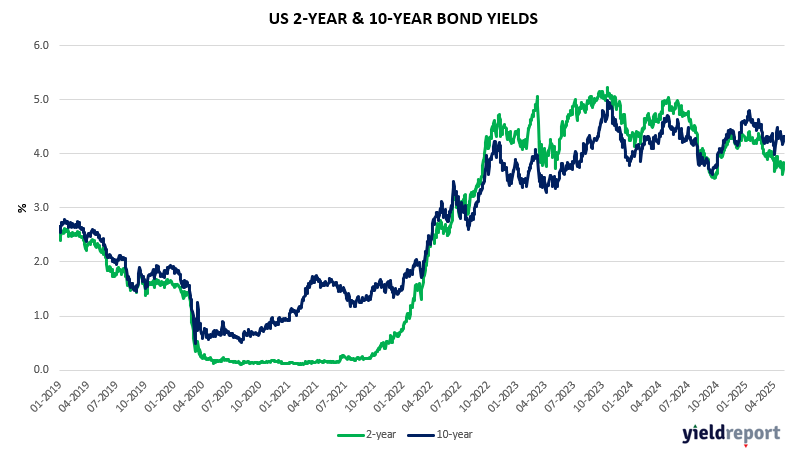

| United States 2-year bond (%) | 3.841 | 3.84 | 0.001 |

| United States 10-year bond (%) | 4.343 | 4.32 | 0.023 |

| United States 30-year bond (%) | 4.829 | 4.795 | 0.034 |

LOCAL BOND MARKETS

Australia’s 10-year government bond yield rose 2 bps to around 4.31%, reaching a two-week high after Prime Minister Anthony Albanese secured a second three-year term in the federal elections. Albanese pledged a “disciplined” government focused on addressing cost-of-living issues, global trade tensions, and reaffirmed commitments to renewable energy, tax cuts, housing, and healthcare investments. These policies are seen as potentially increasing inflationary pressures, which could limit the Reserve Bank’s ability to cut rates. To be honest, a day of tread water.

Meanwhile, the Melbourne Institute’s Monthly Inflation Gauge rose 0.6% in April, easing from March’s 0.7% but marking a second consecutive increase. Investors are now looking ahead to the RBA’s May policy meeting, where a 25 bps rate cut to 3.85% is widely expected. Markets are also pricing in a further decline to 2.85% by year-end amid easing inflation and weaker global growth prospects.

US BOND MARKETS

The yield on the 10-year US Treasury note jumped to 4.35% on Monday, extending the rise from last week as markets weighed on upside inflation risks against economic pessimism from tariffs. ISM data reflected a sharp expansion in US services activity in addition to a surge in cost pressures, aligned with the strong jobs report and higher PCE inflation figures released last week. This countered data that underscored a negative impact from tariff threats, including the GDP contraction in Q1, the surge in imports to front-load levies, and plunge in port volumes.

Lack of clarity on whether President Trump will maintain tariffs for a longer period drove markets to a consensus that the Federal Reserve will maintain rates unchanged this week. While concerns of economic contraction drove rate futures to reflect multiple cuts by the Fed this year, support for US Treasuries were offset by worries that uncertain economic policy may damage the US exceptionalism in capital markets.

What’s happening? Well, this is what’s happening. Fifteen minutes after the April employment report hit early Friday, President Donald Trump seized on the surprisingly strong job growth to ratchet up his pressure on Federal Reserve Chair Jerome Powell, saying there was no reason to hold off on cutting interest rates. Bond traders came to the exact opposite conclusion. The pace of hiring — as well as a manufacturing report on Thursday that wasn’t as downbeat as expected — drove traders to dial back rate-cut bets that had steadily mounted as Trump’s trade war unleashed havoc in financial markets and sowed fears of a US recession.

After piling into short-term Treasuries, anticipating the Fed would start easing policy as soon as next month to contain the fallout, they reversed course. Two-year yields shot up, staging the biggest two-day jump since October, and futures traders started pricing in what Fed officials have been consistently trying to drive home — that they will remain in wait-and-see mode until there’s more evidence that the economy has turned. With inflation being above the Fed’s target, tariffs which can move prices higher and a still solid labor market, the Fed is unlikely to do anything. They are data dependent and the data could turn weaker by the time the Fed meets mid-June.