| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 41,859.09 | -1.35 | 0.00% |

| S&P 500 | 5,842.01 | -2.6 | -0.04% |

| Nasdaq | 18,925.73 | 53.09 | 0.28% |

| VIX | 20.24 | -0.01 | -0.05% |

| Gold | 3,329.90 | 35.3 | 1.08% |

| Oil | 61.3 | 0.08 | 0.13% |

US MARKET

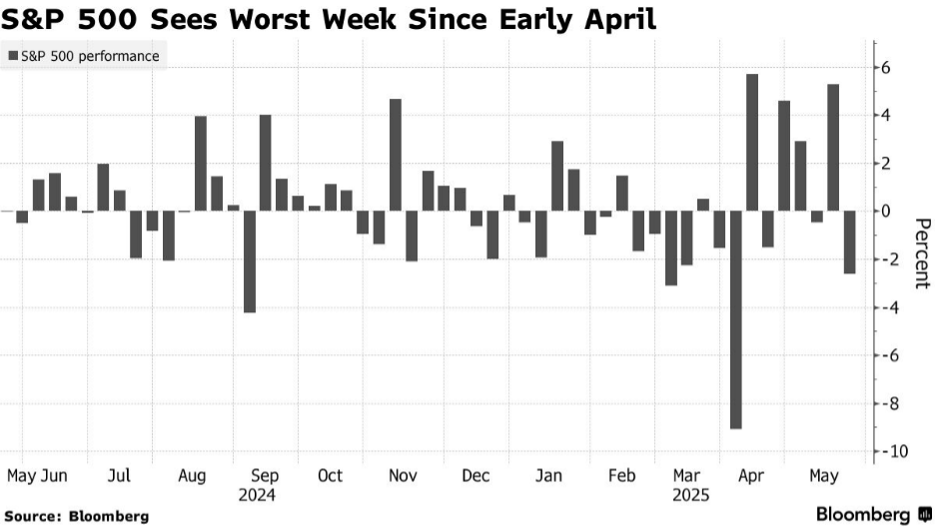

US stocks declined on Friday after Donald Trump escalated trade tensions by threatening tariffs on both Apple and the European Union. The S&P 500 fell 0.6%, the Nasdaq 100 dropped 0.9%, and the Dow lost 256 points. This pullback came just as investors were gaining confidence amid a temporary pause in tariffs and signs of progress in negotiations with the UK and China. Benchmark 10-year Treasuries held 2 bps gains at 4.51% as Bessent said regulators may ease a capital rule on the market, which could reduce yields. Over the week, the S&P 500 fell 2%, the Dow declined 2.2%, and the Nasdaq slipped 1.6%. On Friday, the Dollar Spot Index fell 0.8% to its lowest level since December 2023. US markets are closed on Monday for the Memorial Day holiday.

Apple shares tumbled 3%, bringing its valuation below $3 trillion, after Trump demanded that iPhones sold in the US be made domestically or face a 25% tariff. He also proposed a 50% tariff on all EU imports starting June 1 due to stalled trade talks, renewing fears of protectionist policies. More broadly, tech stocks led the downturn, with names like Micron, Qualcomm, and Nvidia posting losses of more than 1%.

The sudden tariff moves underscores the ongoing risk that shifts in US policy can abruptly upend market dynamics at short notice. Markets had rebounded in recent weeks on optimism that Trump was softening his approach to tariffs, and investor attention had turned to concerns about the US debt and deficits. This is a reminder that the tariffs will continue to be a source of major uncertainty until there are meaningful agreements finalised. Interestingly though, the price reactions were relatively muted, all things considered. That is, the market is viewing it as a Trumpian tactic rather than a likelihood.

While concerns over trade, fiscal deficits, and growth may be less evident in equity markets when considering the broader market’s impressive recovery from the April lows, they still appear to be relevant to the dollar. The USD has struggled to gain traction over the last month as de-dollarization trends continue against a backdrop of rising deficit forecasts and a US debt downgrade. And that, obviously, is pertinent to Australian investors that have exposure to US assets.

OVERVIEW OF AUSTRALIAN MARKET

The S&P/ASX 200 Index rose 0.15% to close at 8,361 on Friday, recouping losses from the previous session, with financial and uranium stocks leading the rebound. The benchmark index also finished the week marginally higher, marking the fifth weekly rise in six. Six of 11 sectors were in the green, with real estate leading gains. The move higher on Friday came after a retreat in US Treasury yields and which helped quell some anxiety about the US fiscal outlook.

Banks helped buoy the ASX 200, with CBA up 0.8% and nearing an all-time high struck earlier in the week. NAB rose 0.9%. Technology tracked gains on Wall Street, with NextDC up 1.8% and Xero 0.8%. Real estate bellwether Goodman Group’s 2.7% advance also helped buoy the ASX. Miners helped moderate the share market’s advance after iron ore slipped back below $US99 a tonne. Fortescue was off 1.7% and Rio Tinto 1.2%.

Uranium miners also saw strong buying interest amid reports that US President Trump may sign executive orders soon to accelerate growth in the nuclear energy industry. Boss Energy surged 12.1%, followed by Paladin Energy (+6.7%) and Deep Yellow (+8.3%).