| Close | Previous Close | Change | |

|---|---|---|---|

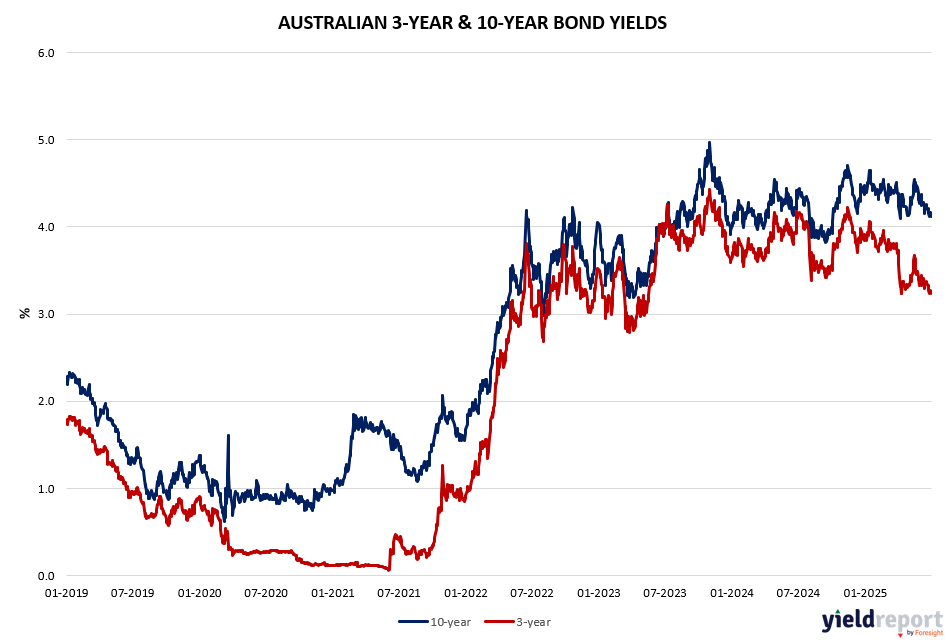

| Australian 3-year bond (%) | 3.238 | 3.271 | -0.033 |

| Australian 10-year bond (%) | 4.123 | 4.166 | -0.043 |

| Australian 30-year bond (%) | 4.81 | 4.858 | -0.048 |

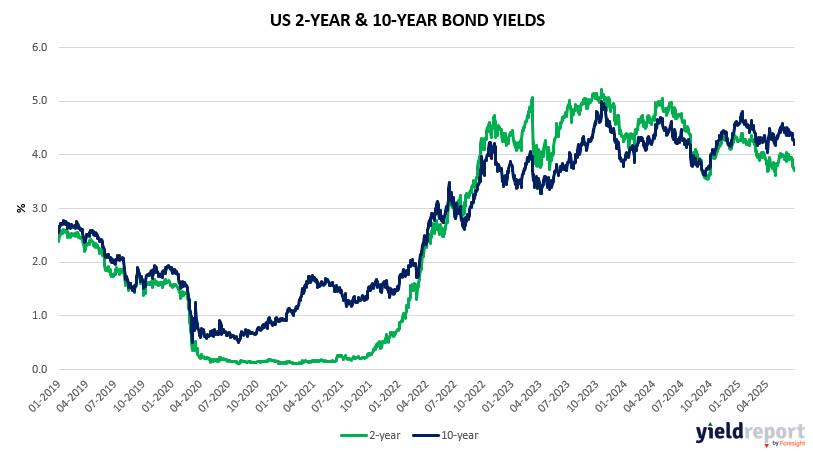

| United States 2-year bond (%) | 3.707 | 3.725 | -0.018 |

| United States 10-year bond (%) | 4.203 | 4.251 | -0.048 |

| United States 30-year bond (%) | 4.7487 | 4.8081 | -0.0594 |

Overview of the Australian Bond Market

The Australian bond market saw steady movements, reflecting a mix of domestic economic stability and global influences. The Bloomberg AusBond Composite 0+ Yr Index edged up 0.12%, signaling a slight rise in bond prices. Short-term yields softened, with three-month bank bills declining 2 basis points to 3.23% and six-month bank bills dropping 5 basis points to 3.54%. Government bond yields varied: the 2-year yield fell to 3.23%, the 5-year held at 3.54%, the 10-year decreased 3 basis points to 4.13%, and the 15-year yield rose slightly to 4.47%.

These shifts occurred amidst expectations of Reserve Bank of Australia (RBA) rate cuts, supported by stable inflation at 2.1% in May and unemployment steady at 4.1%. Markets are pricing in a 92% chance of a 25 basis point cut to 3.60% at the July 7–8 RBA meeting, with two more cuts expected by year-end to bring the cash rate to 3.10%, and a terminal rate of 2.85% projected for early 2026. Key drivers include:

– Weak Q1 GDP growth of 0.2% quarterly and 1.3% annually, below forecasts.

– Subdued consumer and business sentiment.

– A disinflation trend with May CPI at 2.1%.

– Stable unemployment at 4.1%, with minimal wage pressure.

Analysts from CBA, Westpac, NAB, and ANZ forecast a cut to 3.60% in July, followed by a further reduction to 3.35% in August, aligning with expectations of deeper easing. Global trade tensions and geopolitical factors continue to shape market dynamics, though Australia’s bond demand remains robust.

Overview of the US Bond Market

US Treasuries experienced a modest rally as yields declined, influenced by ongoing speculation about Federal Reserve leadership changes. The 10-year Treasury yield fell 4 basis points to 4.24%, while the 2-year yield dropped to 3.77%, reflecting market expectations of potential rate cuts. This movement follows reports of President Donald Trump considering a replacement for Federal Reserve Chair Jerome Powell by September or October, amid his continued push for lower borrowing costs.

Investors anticipate a dovish successor, potentially accelerating rate cuts beyond current projections, with traders pricing in a 95% likelihood of a 25 basis point cut in September and two cuts fully expected by year-end, with a third cut partially anticipated. The Bloomberg Dollar Spot Index weakened by 0.5% to its lowest since April 2022, impacting the dollar against Group-of-10 peers, with Commerzbank predicting the euro could reach $1.18 soon if rate cut expectations persist.

Economic data supported this outlook, with US consumer spending in Q1 growing at a revised 0.5% annualized rate, contributing just 0.3 percentage points to GDP—the weakest since Q2 2020—down from a prior 0.79 point boost, per Bureau of Economic Analysis figures. Durable goods orders surged 16.4% in May, driven by a 48% rise in transportation equipment, notably nondefense aircraft parts, though broader business investment remained sluggish, according to Commerce Department data.