Summary:

Weekly Overview – Ending 4 July 2025

Short-term money market rates eased further this week, with Bank Bill Swap Rates (BBSW) falling across all key tenors. The 1-month BBSW dropped by 8.18 basis points to 3.585%, while the 3-month and 6-month rates declined to 3.583% (-3.70 bps) and 3.7544% (-0.63 bps) respectively. These declines reflect softening funding conditions and increasing market expectations of RBA rate cuts, as short-term inflation and growth pressures continue to moderate.

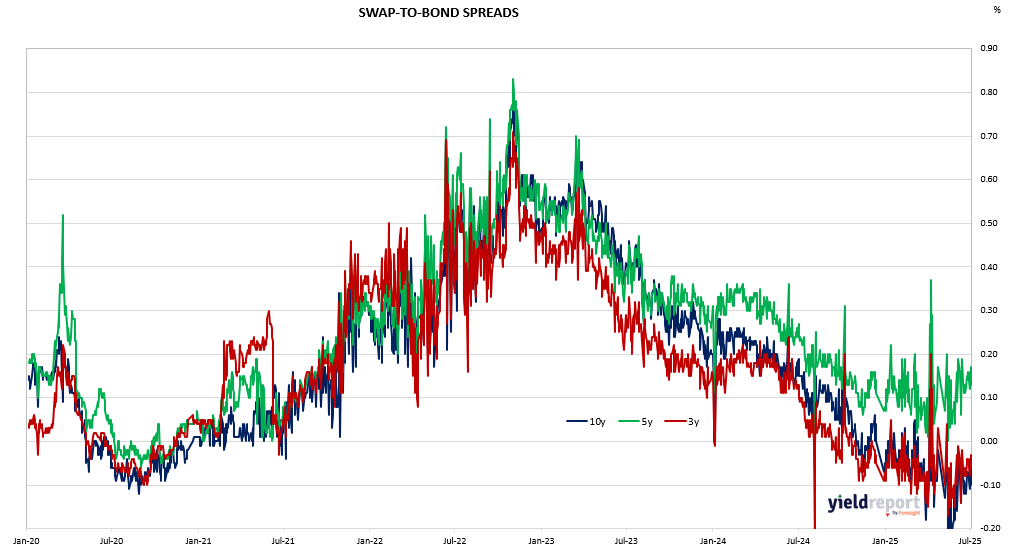

Meanwhile, longer-term swap rates moved modestly higher. The 10-year swap rate rose by 2.38 basis points to 4.093%, with similar gains seen in the 5-year (+2.13 bps to 3.6325%) and 3-year (+2.00 bps to 3.235%) tenors. Despite the weekly uptick, monthly changes remain flat or negative, reflecting continued caution. The swap-to-bond spread chart shows spreads nearing zero or turning negative across 3Y, 5Y, and 10Y terms, suggesting tighter yield differentials and a possible shift in investor sentiment towards lower-risk government bonds.

Bank Bill Swap Rates

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 month 3.585 -0.0818 -0.17 3 months 3.583 -0.037 -0.1284 6 months 3.7544 -0.0063 -0.0241 SWAP RATES

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 year 3.2451 0.0075 -0.0584 3 years 3.235 0.02 0.0013 5 years 3.6325 0.0213 -0.0038 10 years 4.093 0.0238 -0.0058 15 years 4.3305 0.0327 0.0005

Exhibit 1: Australian 3Y/10Y Bond Yield