| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 44,240.76 | -165.6 | -0.37% |

| S&P 500 | 6,225.52 | -4.46 | -0.07% |

| Nasdaq | 20,418.46 | 5.95 | 0.03% |

| VIX | 16.81 | -0.98 | -5.51% |

| Gold | 3,310.50 | -6.4 | -0.19% |

| Oil | 68.03 | -0.3 | -0.40% |

OVERVIEW OF THE US MARKET

Mixed sentiment prevailed as stocks showed resilience amid the passage of the “One Big Beautiful Bill” and uncertainty around today’s July 9 tariff deadline, now extended to August 1. Treasury yields edged higher, and the dollar remained stable. Oil prices rose slightly, though Middle East tensions have muted.

The S&P 500 dipped 0.07% to 6,225.52, and the Nasdaq Composite edged up 0.03% to 20,418.46, reflecting a cautious close. West Texas Intermediate crude climbed to $67.50 a barrel, supported by energy sector strength. In after-hours trading, BTCS Inc. surged, signaling speculative interest.

Energy stocks led gains, up 2.72%, driven by oil price stability despite eased Middle East concerns. Tech stocks, including NVIDIA up 1.11% on high volume, regained ground, buoyed by the OBBBA’s tax cut extensions. Consumer staples fell 1.09%, with defensive names under pressure. The OBBBA, signed into law, extends 2017 tax cuts and adds deductions, boosting market optimism, though tariff uncertainty lingers with negotiations ongoing.

Middle East tensions have subsided, with the Israel-Iran ceasefire holding steady, reducing oil volatility risks. Market expectations currently price two rate cuts by year-end, with September favored, reflecting caution amid fiscal and trade developments. Today’s tariff deadline resolution, now shifted to August 1, could still influence sentiment as trade talks continue.

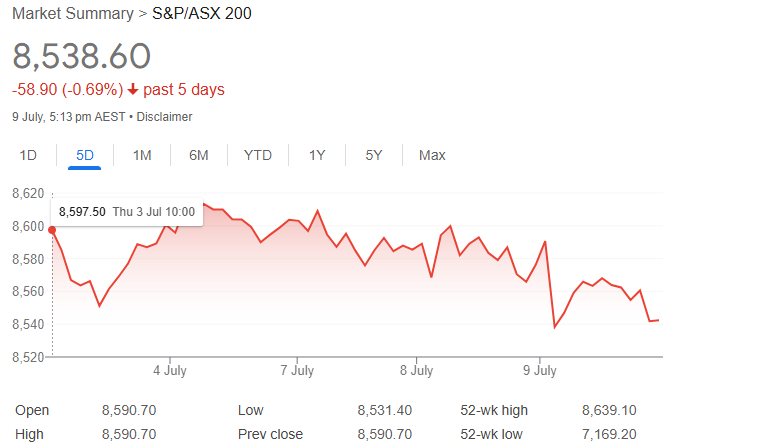

OVERVIEW OF THE AUSTRALIAN MARKET

The ASX 200 closed 1.4 points higher (+0.02%) at 8,591.4, defying expectations after the RBA’s surprise decision to hold rates steady. With an 86% cut likelihood priced in, the market’s late rally from session lows of -0.46% showcased resilience, partly fueled by global optimism from the OBBBA.

Market breadth was balanced, with 102 S&P/ASX 200 constituents finishing lower. The big four banks led the rebound, with Commonwealth Bank up 0.8%, NAB up 0.6%, and ANZ up 0.2%. Wesfarmers added 0.5%, boosting late strength. Consumer staples faced selling pressure, with Woolworths down 1.4% and Coles down 1.7%, while utilities (-1.1%) and real estate (-0.5%) struggled amid rate hold reactions.

The RBA’s hold, announced at 2:30 PM AEST yesterday, shifted focus to future cuts, with investors eyeing year-end easing.