Summary

With Trump’s new tariff regime set to begin August 1, global trade partners face escalating pressure. Formal rate notices—ranging from 10% to 70%—will be sent by July 9. So far, only Vietnam and the UK have secured agreements, while negotiations with Japan and the EU remain tense. Vietnam faces re-export tariffs as high as 40%, and Japan risks auto tariffs amid electoral sensitivities. Despite the looming disruption, markets are pricing in short-lived tariff pressure, fueling TACO trades. However, the lack of finalized deals underscores rising geopolitical friction just as U.S. fiscal strategy leans heavily on trade as a revenue pillar.

Backdrop

Since Trump announced his reciprocal tariffs on April 2, we pointed out three contradictions that undermine the US position, leading us to conclude that the tariff stance would likely soften—a view we’ve since updated in subsequent reports.

On July 7, Trump unveiled a new tariff list and simultaneously extended the negotiation deadline to August 1. This reinforces that high tariffs are proving to be self-damaging to the US economy, and that Trump still sees negotiations as his core strategic tool.

Real Motives

The latest developments in negotiations, Trump’s demands and pursues bargaining logic across three dimensions: country-level tariffs, industry-specific tariffs, and non-tariff agreements.

- First, on country-level tariffs, we can observe from two countries that have already finalized trade agreements with the US—the UK (a pro-US ally) and Vietnam (a China-friendly country)—that subsequent tariffs are likely to fall within the 10–20% range. As outlined in our April 2 report, this aligns with our projected scenario of an effective tariff rate increase of 10–15%.

- Second, industry-specific tariffs appear more bark than bite. Most are “conditional tariffs”—steel and aluminium tariffs apply only to their core components; auto parts are exempt if they comply with USMCA rules. The much-anticipated semiconductor tariffs have yet to materialize, largely due to the US semiconductor industry’s dependence on foreign-sourced critical inputs (about 60%). Imposing tariffs in this area would end up harming the US the most.

- Finally, looking beyond tariffs to broader agreements, Trump’s true objectives become even clearer through ongoing bilateral negotiations: market access (e.g., Vietnam reducing import tariffs on US goods to 0%), US-directed investment (e.g., countries placing large orders for Boeing aircraft, US beef, and LNG), and the strategic containment of China.

These demands are repeatedly emphasized in talks with various countries, revealing the core “real agenda” behind Trump’s policy.

High tariffs, while often front and centre in public discourse, are largely a fake issue—a tool rather than a goal. In contrast, foreign investment into the US is a real issue, reflecting a key economic objective.

Similarly, the much-hyped concern over US debt default is another fake issue, whereas the Federal Reserve’s interest rate policy, particularly rate cuts, is a real issue with tangible economic implications. Media distractions such as the Mar-a-Lago scandals fall into the fake category, while US dollar hegemony remains a real and strategic priority.

From these observations, Trump’s core policy strategy becomes clear.

- Domestically, it centres on expanding fiscal stimulus, while

- Internationally, the priority is to maintain sustained pressure on China. Tariffs serve as a crucial instrument within this strategy: they help bridge fiscal gaps created by tax cuts and simultaneously exert leverage on foreign governments. However, it’s critical to note that this strategy is only sustainable under the condition of moderate tariff levels. If tariffs rise too aggressively, they risk driving up inflation, complicating the Federal Reserve’s path to cutting interest rates, exacerbating the US debt burden, and provoking retaliatory actions from trade partners.

- Once the market internalizes this trade-off, its sensitivity to tariff news will likely diminish.

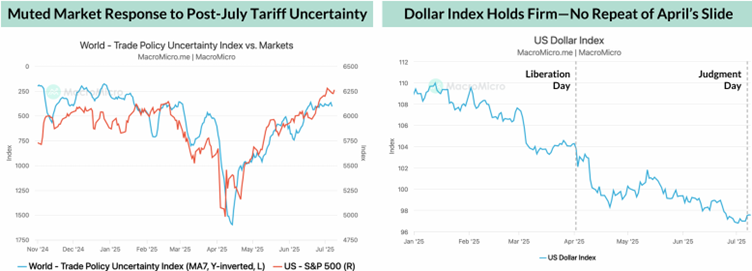

Trade policy uncertainty remains elevated post-‘Judgment Day’, but markets have not experienced renewed volatility—suggesting stabilization rather than escalation.

Markets show signs of tariff fatigue: US equities hit fresh highs in June, and even after Trump unveiled retaliatory tariffs on 14 trading partners, stocks held steady. The US Dollar Index also stabilized near 97, avoiding the steep sell-off seen in early April

Figure 1: Market Response to July Tariff

About YieldReport – Your Income Advantage

YieldReport is Australia’s leading online data and research platform for interest rate markets, securities and products that focus on fixed income and yield generation. YieldReport provides advice, reviews, analysis and insights on what’s shaping the yield curve and fixed income markets. It’s a key reference for pricing and performance data on yield-generating investments — from cash, term deposits, and bonds to hybrids, ETFs, and more.

Its insights help individuals and institutions make informed decisions — whether managing their own portfolios or acting in fiduciary roles.

Explore more via the website: www.yieldreport.com.au

Follow daily updates on LinkedIn, X, Instagram & Facebook.

Contact us: contact@yieldreport.com.au or call 0408 266 713.