| Close | Previous Close | Change | |

|---|---|---|---|

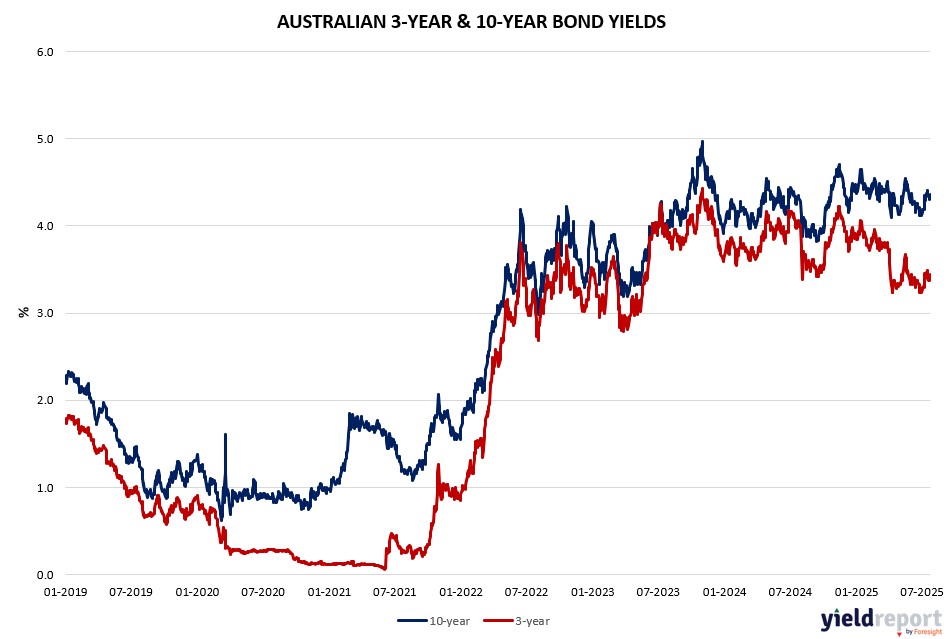

| Australian 3-year bond (%) | 3.455 | 3.447 | 0.008 |

| Australian 10-year bond (%) | 4.355 | 4.356 | -0.001 |

| Australian 30-year bond (%) | 5.064 | 5.071 | -0.007 |

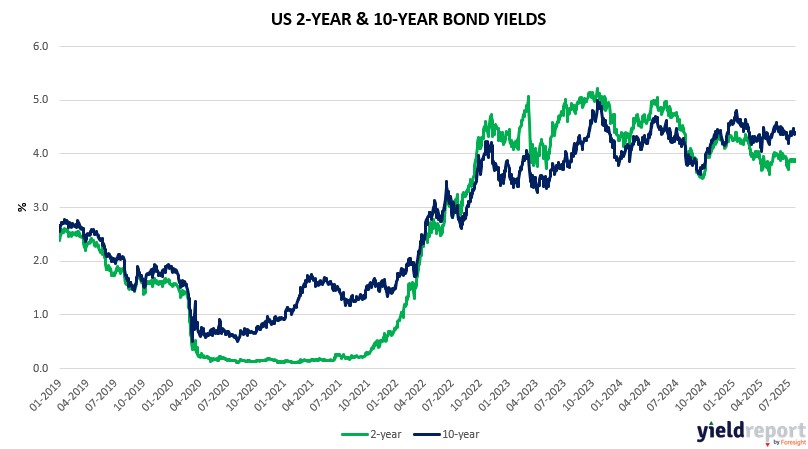

| United States 2-year bond (%) | 3.925 | 3.889 | 0.036 |

| United States 10-year bond (%) | 4.412 | 4.392 | 0.02 |

| United States 30-year bond (%) | 4.9543 | 4.9481 | 0.0062 |

Overview of the Australian Bond Market

Australian 10-year Treasuries dipped slightly as the market absorbed Friday’s weak close, with the yield falling 1 basis point to 4.34%. The 2-year yield rose 1 basis point to 3.41%, while the 5-year yield held steady at 3.74%. The 15-year yield eased 1 basis point to 4.70%, reflecting cautious sentiment amid global trade tensions.

Yields have risen over the past month, with the 10-year up 22 basis points, supported by solid PMI data (composite 53.6, services 55.2) but tempered by a -0.03% composite leading index. The RBA’s measured and gradual rate-cut path forms expectations on an almost sure cut in August and another cut later this year, targeting 3.35% in early 2026. The AUD’s 0.14% drop to 0.6581 signals trade uncertainty.

Interest-rate swaps show a flattish curve, with yields reacting to US durable goods beating expectations at -9.3% and new home sales at 0.627 million. The August 1 tariff deadline will be pivotal, with markets balancing domestic resilience against global risks.

Overview of the US Bond Market

On Friday, the US Treasury bond market experienced modest yield declines across most maturities, reflecting cautious investor sentiment amid mixed economic signals. The 10-year Treasury yield fell by approximately 2 basis points to 4.388%, while the 30-year yield dropped 2.3 basis points to 4.926%, indicating a slight shift toward safer assets.

Shorter-term yields also edged lower, with the 2-year yield down 2.7 basis points to 3.821%, suggesting tempered expectations for aggressive Federal Reserve rate cuts. The bond market responded to softer-than-expected economic data, including a dip in durable goods orders and signs of cooling inflation, which reinforced the view that the Fed may ease policy later this year.

Treasury Inflation-Protected Securities (TIPS) saw mixed movement, with the 5-year TIPS yield declining to 1.45%, while longer-dated TIPS rose slightly, reflecting uncertainty around long-term inflation expectations.

Overall, trading volumes remained steady, and the yield curve stayed inverted, signalling ongoing concerns about economic slowdown. Investors are closely watching upcoming data releases, including the Fed’s interest rate decision and Q2 GDP figures, which could influence future yield movements.

The bond market’s cautious tone underscores its role as a barometer for macroeconomic sentiment and monetary policy expectations.

Monthly reports on sales of existing homes and new homes both came in below analysts’ forecasts as elevated mortgage rates and high prices continued to weigh on the U.S. housing market. Sales of existing homes fell 2.7% in June to 3.93 million while new home sales rose a below forecast 0.6% to 627,000.

Looking ahead, Wednesday’s initial estimate of second-quarter GDP will show whether the U.S. economy rebounded in the spring from the first quarter’s negative result. From January through March, GDP decreased at an annual rate of 0.5%, in part due to an increase in imports in advance of rising tariffs. It was the first quarterly contraction in GDP since the first quarter of 2022.

In addition to a GDP report and more quarterly earnings, the new week will bring a U.S. Federal Reserve policy meeting that concludes on Wednesday and a jobs report on Friday. The Fed is widely expected to keep interest rates unchanged; the jobs report will show how July’s jobs growth compared with June’s bigger-than-expected gain of 147,000 jobs.