Summary:

The Australian Government bond yields finished the week higher as investors adjusted their expectations based on RBA Governors speech and macro data that were released over the week.

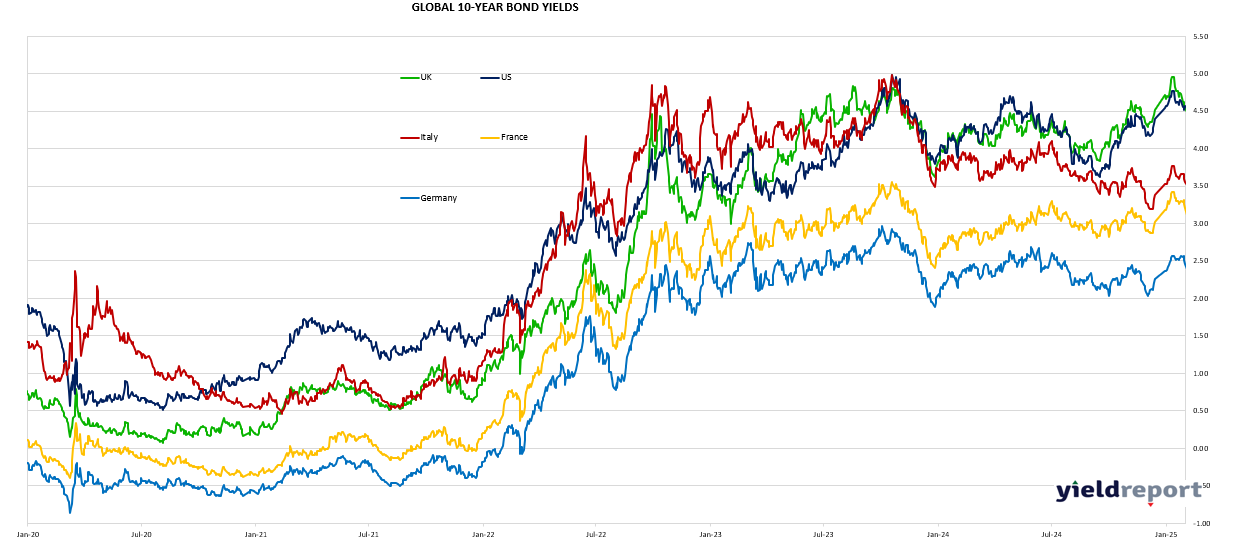

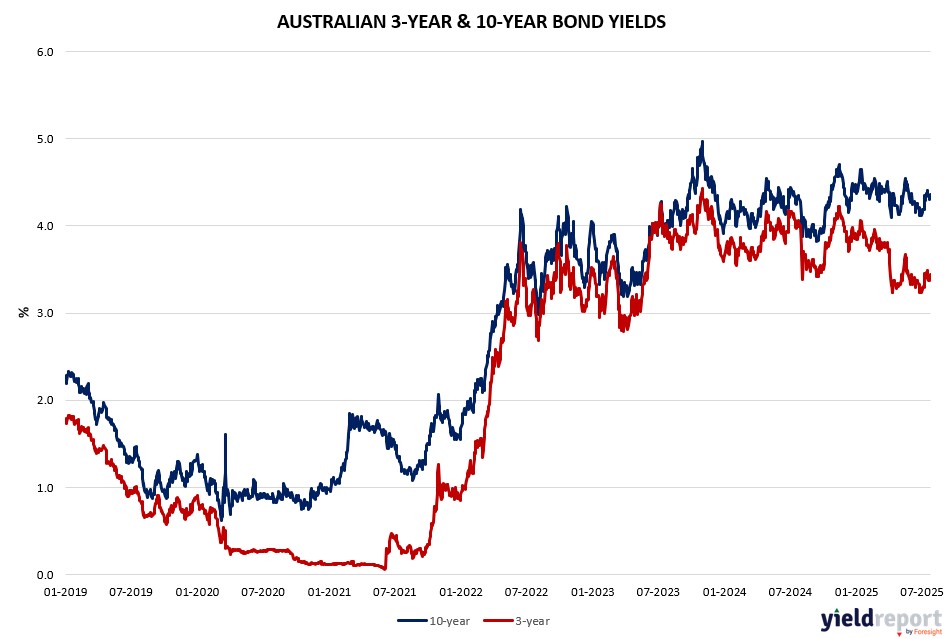

The 1-year and 2-year government bonds yield increased by 8 basis points while the benchmark Australian 10-year Government bond yield moved slightly higher by 2 basis points to finish at 4.36 %, levels that were very close to where US 10-year bonds finished last week. The 30-year bonds also sold off with yield increasing 4 basis points to close at 5.06%.

This week’s cash rate expectations by market participants were adjusted to signal a cautious market stance after the RBA left rates steady in its meeting earlier in the month, surprising many economists who predicted a rate cut by 25bps. The current cash rate sits at 3.85% compared to the cycle peak of 4.35% that was reached in September 2023. The first cut in the current cycle was delivered by the RBA on 19th February 2025.

The market is pricing in a 75-basis point cut over the next year, targeting a 3.1% cash rate by mid-2026, influenced by recent economic data including the CPI and US Fed Reserve decision to keep rates steady in the US. RBA does not appear to be concerned about the recent increase in Australian unemployment rate, siting tight labour market conditions. So while the market participants are focused on growth and employment concerns, the RBA is taking a more balanced approach to both growth and inflation given the uncertainty around tariff impact within the context of tight labour market.

The Bank Bill Swap Rate (BBSW) market remained steady this week, reflecting a balanced response to the RBA’s decision to hold the cash rate at 3.85%, weak employment data in Australia and somewhat mixed macro data from the US. For the week ending July 25, 2025, the 1-month BBSW held at 3.70%, while the 3-month BBSW stayed at 3.69%, based on daily data trends. The 6-month BBSW dropped slightly to 3.75% from 3.76%, indicating a flat short-end yield curve amid tariff concerns, mixed macro and price data and market anticipation of an August rate cut.

The longer end of the swap rate curve steepened during the week with the 1-year swap rate up 8 basis points to 3.41%. The 3-year swap rate increased 9 basis points to end the week at 3.41%. The 5-year swap rate increased 6 basis points to 3.80%, reflecting investor expectations of revised cash rate path for Australia following RBA’s surprise decision to pause rate cut earlier during the month and uncertainties around US tariffs.

The Australian 3- and 10-year bond spreads moved slightly higher as market participants adjusted their short end rate expectations. In the US, the spread between 2- and 10-year bonds were stable over the week.

Figure 1: Aust. 3 yr minus 10 yr Bond Spread

Figure 2: Australian & US Bond Yields

Figure 3: US 10 yr minus 2 yr Bond Spread