| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 43,968.64 | -224.48 | -0.51% |

| S&P 500 | 6,340.00 | -5.06 | -0.08% |

| Nasdaq | 21,242.70 | 73.27 | 0.35% |

| VIX | 16.57 | -0.2 | -1.19% |

| Gold | 3,498.30 | 44.6 | 1.29% |

| Oil | 63.88 | 0 | 0.00% |

OVERVIEW OF THE US MARKET

Just after midnight, sweeping U.S. tariffs took effect across dozens of countries, intensifying President Trump’s trade war. Negotiators from affected nations, including Switzerland, are scrambling to secure exemptions and reduce tariff rates. Swiss President Karin Keller-Sutter left Washington without a deal, facing a steep 39% tariff. India’s Prime Minister Narendra Modi responded defiantly to Trump’s decision to double tariffs on Indian goods to 50%, vowing to protect domestic farmers amid criticism over India’s Russian oil purchases.

Markets reacted unevenly. The Nasdaq notched its 17th record high of 2025, while the Dow and S&P 500 slipped slightly. Apple shares surged after announcing a $100 billion investment in U.S. manufacturing, earning it a potential tariff waiver. Meanwhile, Intel stock fell after Trump called for its CEO’s resignation. The European Union secured a 15% tariff ceiling on semiconductor exports as part of a broader trade agreement.

Toyota warned tariffs could cost it $9.5 billion this year. Treasury yields rose following a weak 30-year bond auction. In Europe, the Stoxx 600 climbed, but the U.K.’s FTSE 100 dropped after the Bank of England cut interest rates, strengthening the pound. Trump also nominated Stephen Miran to the Federal Reserve board on a short-term basis.

U.S. tariffs and corporate earnings drove sharp moves across sectors:

🚀 Gainers

- Apple (AAPL): Rose 3.2% after pledging an additional $100B to U.S. manufacturing, qualifying for potential tariff exemptions.

- TSMC (TSM), Broadcom (AVGO): Semiconductor stocks climbed on hopes of tariff waivers.

- Corning (GLW), MP Materials (MP): Gained after Apple announced partnerships tied to its domestic production push.

- DoorDash (DASH): Jumped 5% after swinging to profit and beating revenue expectations.

- Firefly Aerospace (FLY): Soared 34% on its Nasdaq debut.

- Duolingo (DUOL): Surged 14% on strong user growth and bookings.

- Rogers (ROG): Rose 2.4% after activist investor Starboard Value disclosed a 9% stake.

📉 Decliners

- Eli Lilly (LLY): Dropped 14% after its weight-loss pill underwhelmed; rival Novo Nordisk (NVO) rose 6.7%.

- Crocs (CROX): Plunged 29% after warning of declining sales and a $90M annual tariff hit.

- Ralph Lauren (RL): Fell 6.5% despite raising guidance, citing inflation concerns from levies.

- Bumble (BMBL): Slid 16% on weaker quarterly sales and declining paid user numbers.

The tariff landscape continues to reshape investor sentiment and corporate strategy.

OVERVIEW OF THE AUSTRALIAN MARKET

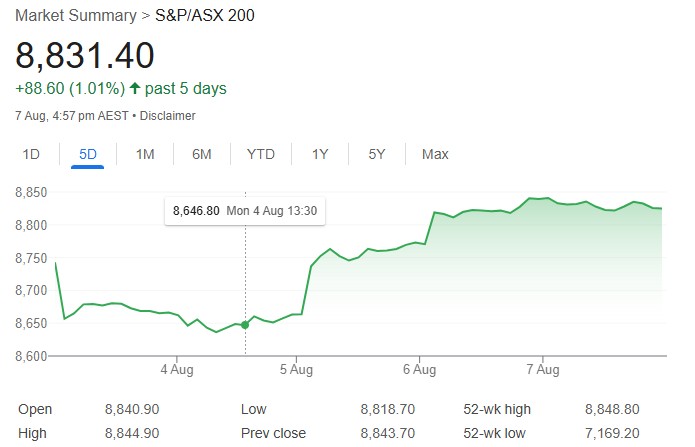

The Australian share market dipped slightly on August 7, 2025, as the S&P/ASX 200 index closed 12.3 points lower, or 0.14%, at 8,831.4, retreating from its record high the previous day. The broader All Ordinaries index also edged down, losing 9.1 points, or 0.10%, to 9,102.0. Despite the pullback, the market recorded its second-highest close in history, with advancers outpacing decliners 186 to 92 on the S&P/ASX 300, signaling a relatively mild correction.

Six of the 11 major ASX sectors ended in positive territory, with Consumer Discretionary leading the pack, up 0.89%, driven by strong performances from Wesfarmers (+0.7% to $89.52) and Aristocrat Leisure (+1.5% to $71.38). Information Technology followed with a 0.40% gain, buoyed by a robust US tech sector lead overnight. Real Estate (+0.37%) and Energy (+0.19%) also supported the market, with the latter tracking a modest uptick in oil prices after positive US demand data and potential Ukraine peace talks. The Gold Sub-Index (+1.2%) shone brightly, lifted by rising gold prices, with Westgold Resources rallying 5.1% to lead the top-200 performers.

Health Care was the weakest sector, down 1.16%, dragged lower by heavyweights Resmed (-2.1%) and CSL (-1.5%). Financials also struggled, falling 0.29%, primarily due to an 8.6% plunge in ASX Limited ($6.06) after an earnings miss and ongoing governance scrutiny. Commonwealth Bank (-0.5%) and NAB (-0.5%) contributed to the sector’s decline, though ANZ and Westpac posted modest gains.

Standout performers included defence stocks like Electro Optic Systems (+11%) and Elsight (+10%), alongside a lithium stock revival led by Pilbara Minerals (+3.8%), spurred by a surge in GFEX lithium carbonate futures. AMP also rebounded 4.8% after an optimistic outlook from UBS. Conversely, TPG Telecom’s shares remained subdued, recovering only 0.8% to $5.26 after a selloff triggered by a takeover announcement mix-up.

Investors are cautious ahead of the Reserve Bank of Australia’s (RBA) upcoming monetary policy decision, with bond traders pricing in a potential rate cut following a higher-than-expected trade surplus of AUD 5,365 million in June, well above the Reuters poll estimate of AUD 3,400 million. This bolstered the Australian dollar, which climbed 0.36% to 65.26 US cents.