| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.377 | 3.362 | 0.015 |

| Australian 10-year bond (%) | 4.257 | 4.252 | 0.005 |

| Australian 30-year bond (%) | 4.976 | 4.978 | -0.002 |

| United States 2-year bond (%) | 3.742 | 3.713 | 0.029 |

| United States 10-year bond (%) | 4.254 | 4.24 | 0.014 |

| United States 30-year bond (%) | 4.8273 | 4.8191 | 0.0082 |

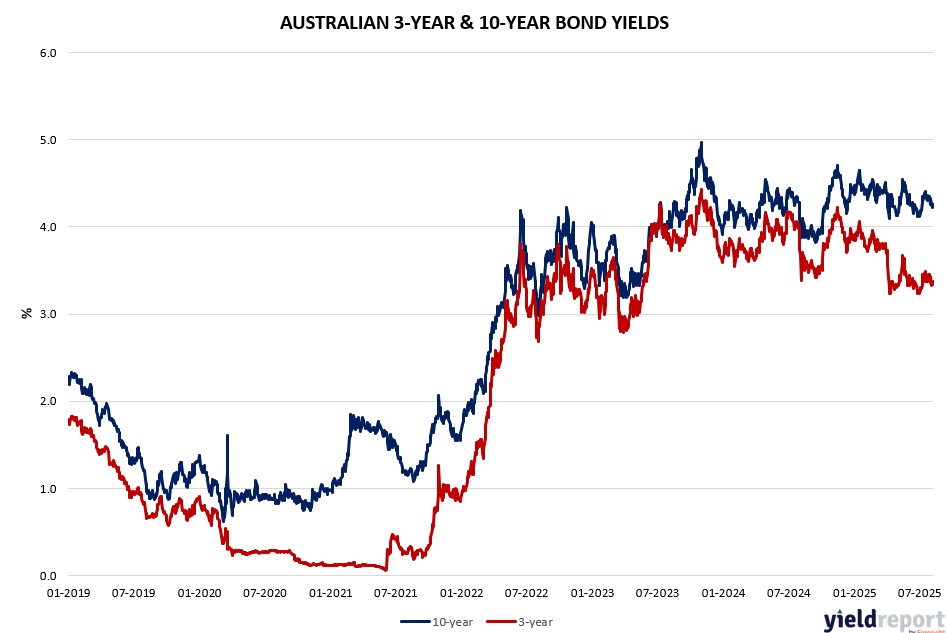

Overview of the Australian Bond Market

Australian government bond yields were mixed on August 8, 2025, as traders balanced strong trade data against global yield rises and RBA cut expectations. The 10-year yield held at 4.24% (flat daily, -10 basis points monthly), the 2-year rose to 3.34% (+1 bp daily), the 5-year to 3.64% (+1 bp), and the 15-year at 4.60% (flat daily, -7 bp monthly), reflecting caution on inflation amid commodity strength.

June’s trade surplus surprised at AUD 5,365 million (vs. poll AUD 3,400 million), driven by 6% export growth and -3.1% imports, fueling RBA cut bets for Tuesday and lifting resources stocks. Yet, July’s S&P Global Services PMI at 54.1 and Composite at 53.8 signal expansion, tempering dovish views.

Global factors, including US-China truce talks (potential 90-day extension) and the Fed’s steady 4.25%-4.5% rate, influence flows, with US 10-year yields up to 4.28%. Locally, resilient data like steady jobless claims echo US stability, supporting higher-for-longer rates, though tariff risks cloud the outlook.

Bond investors monitor US CPI on August 12 for Fed cues, with swaps implying ~60% chance of September 25 bp cut. Australian dealers expect stable auction sizes, mirroring US guidance. With equity valuations stretched and gold/commodity haven demand, bonds offer diversification, but trade war resilience may keep yields elevated longer.

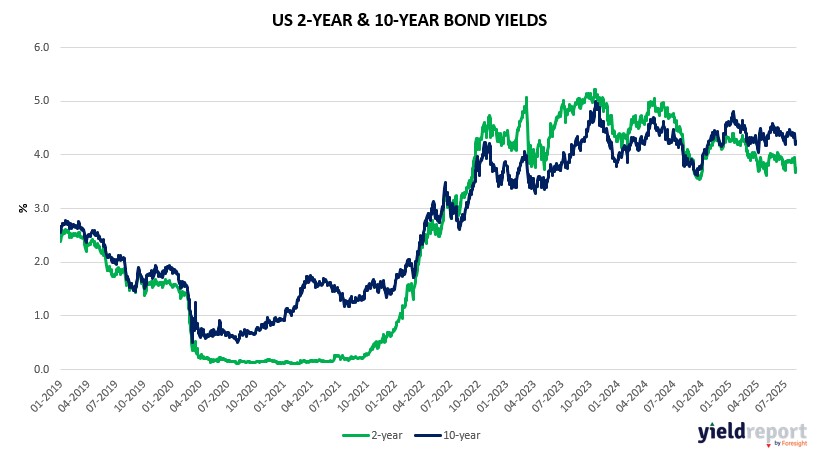

Overview of the US Bond Market

Bond traders increased wagers on Treasuries amid a volatile week, as markets positioned for the Federal Reserve’s potential rate path clarification in upcoming meetings. Yields rose modestly, with the 10-year Treasury note climbing to 4.28% from an implied prior close, the 2-year up to 3.76% ( +7 basis points implied daily), and the 30-year at 4.85%. Shorter maturities saw pressure from resilient labor data, while longer ends reflected inflation watchfulness.

A steady $44 billion auction earlier in the week supported demand, with longer-dated bonds holding firm despite oil’s 5.49% drop to $63.57 per barrel on supply concerns. Gold, however, rose 1.26% to $3,402.5, underscoring safe-haven flows amid US-Russia tensions over Ukraine, where President Trump hinted at additional levies absent a truce.

On the economic front, initial jobless claims held steady at 226,000 for the week ended August 2 (in line with expectations), bolstering views of labor market stability despite July’s softer ISM Non-Manufacturing PMI at 50.1. June factory orders fell 4.8% as polled, and the trade deficit improved to -$60.2 billion, easing some external pressures.

JPMorgan’s weekly Treasury client survey indicated a slight uptick in net long positions, the highest in a month, signaling renewed bullishness. Market-implied Fed expectations via swaps price in about a half-point easing by year-end, starting possibly in September, with a 60% chance of a 25 basis-point cut then. This comes as Fed Chair Jerome Powell faces internal dissent for more labor support and external pressure from Trump to ease borrowing costs, currently at 4.25%-4.5%.

Countervailing factors, including the US economy’s trade war resilience and recent EU/Japan deals reducing uncertainty, support a higher-for-longer rate view, pressuring Treasury prices. Yet, with S&P Global Composite PMI at 55.1 for July (above prior), optimism persists for soft landing.

In cash markets, JPMorgan’s survey to August 7 showed more longs and fewer shorts since early July, with net longs at a two-month high. CFTC data through August 5 revealed asset managers trimming net longs by $15 million per basis point across tenors, focused on 5- and 10-year contracts, while leveraged funds reduced shorts in the 30-year by $4 million.

Dealers anticipate unchanged coupon auction sizes for August-October, per Treasury guidance, with 10-year sizes up $1 billion from recent issues.