| Close | Previous Close | Change | |

|---|---|---|---|

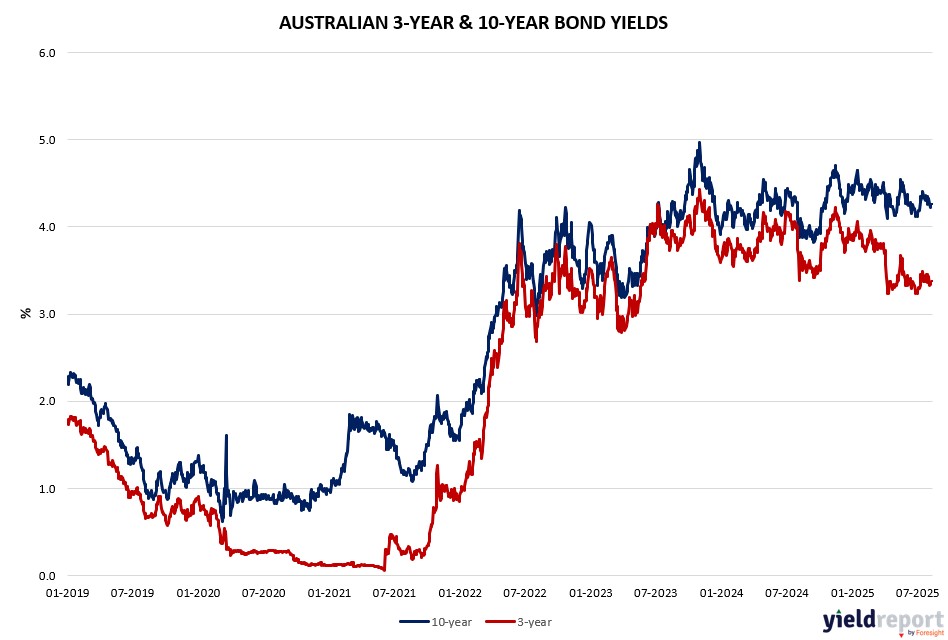

| Australian 3-year bond (%) | 3.325 | 3.322 | 0.003 |

| Australian 10-year bond (%) | 4.23 | 4.215 | 0.015 |

| Australian 30-year bond (%) | 4.97 | 4.951 | 0.019 |

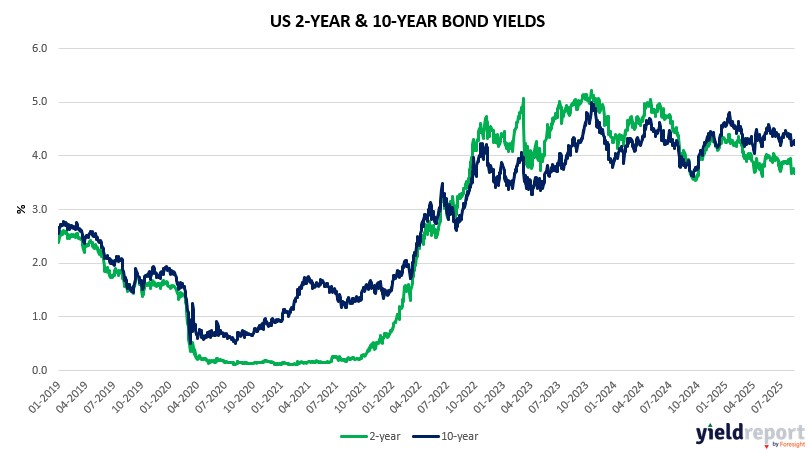

| United States 2-year bond (%) | 3.728 | 3.668 | 0.06 |

| United States 10-year bond (%) | 4.293 | 4.208 | 0.085 |

| United States 30-year bond (%) | 4.8867 | 4.7984 | 0.0883 |

Overview of the Australian Bond Market

Australian bond yields ticked higher on August 15, reflecting tempered rate cut expectations after July employment data undershot slightly, but wage growth on August 13 came in at 0.8% quarterly and 3.4% yearly, above forecasts and signalling persistent inflation pressures post the RBA’s August cut to 3.6% from 3.85%. The 10-year yield rose 2 basis points to 4.23%, down 15 monthly but up 35 yearly, while the 2-year climbed 1 to 3.29%, and the 15-year to 4.60%.

With core CPI steady and consumer confidence buoyed by the rate reduction, markets eye upcoming US data for global cues, though local earnings and stimulus hopes from China data support a bullish tilt. Dealers anticipate steady auction sizes, but geopolitical risks like tariff talks could spur volatility. The AUD’s 0.18% gain versus the USD underscores currency strength, potentially capping yield declines as the RBA balances growth and prices.

Resilient labor metrics, despite the slight employment miss, bolster the case for gradual easing, with wage pressures dissipating some trade war uncertainty from recent pacts, though high valuations warrant caution on duration bets.

Overview of the US Bond Market

Bond traders trimmed long positions in Treasuries over the past week, bracing for clarity on Fed rate cuts amid mixed economic signals, including July’s steady retail sales but softer industrial production, which bolstered bets for easing while highlighting growth headwinds. A rally in shorter maturities gained traction, with 2-year yields dipping to 3.75% from 3.76% a month prior, though 10-year yields rose to 4.32% on the day, up 16 basis points monthly but 40 higher year-over-year. Oil prices eased 0.30% to $63.16/barrel, tempering inflation fears as gold fell 1.98% to $3,336.20.

Core CPI data from August 12 showed a 0.3% monthly rise and 3.1% yearly, slightly above expectations, reinforcing the Fed’s cautious stance on cuts, with markets pricing in about a 60% chance of a 25 basis-point move in September. JPMorgan’s client survey revealed net longs at two-month lows, with asset managers paring positions by $23.5 million per basis point across tenors, while leveraged funds reduced shorts in the bond contract. Geopolitical talks, including US-Russia discussions in Alaska, add uncertainty, potentially influencing tariff extensions and debt auction sizes, which dealers expect to hold steady for August-October.

The resilience of consumer spending amid Trump’s trade policies has supported higher-for-longer rate views, dissipating some uncertainty from recent EU and Japan deals, though elevated valuations suggest diversification. Countervailing factors, like labour market cooling from prior job openings data, cloud the medium-term outlook, with Fed Chair Powell possibly facing internal dissent for more support.