| Close | Previous Close | Change | |

|---|---|---|---|

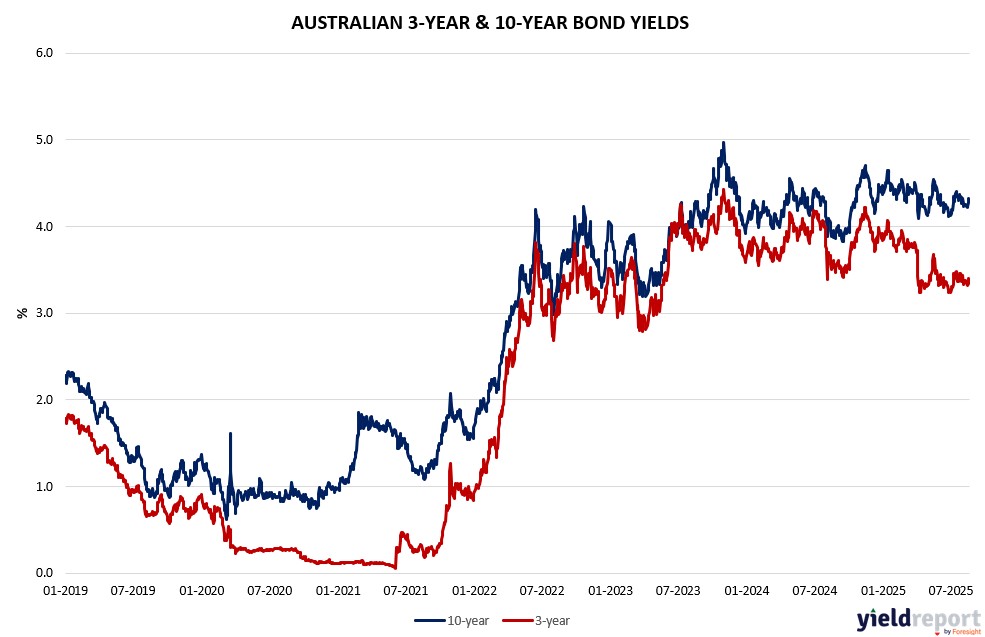

| Australian 3-year bond (%) | 3.361 | 3.367 | -0.006 |

| Australian 10-year bond (%) | 4.279 | 4.301 | -0.022 |

| Australian 30-year bond (%) | 5.054 | 5.052 | 0.002 |

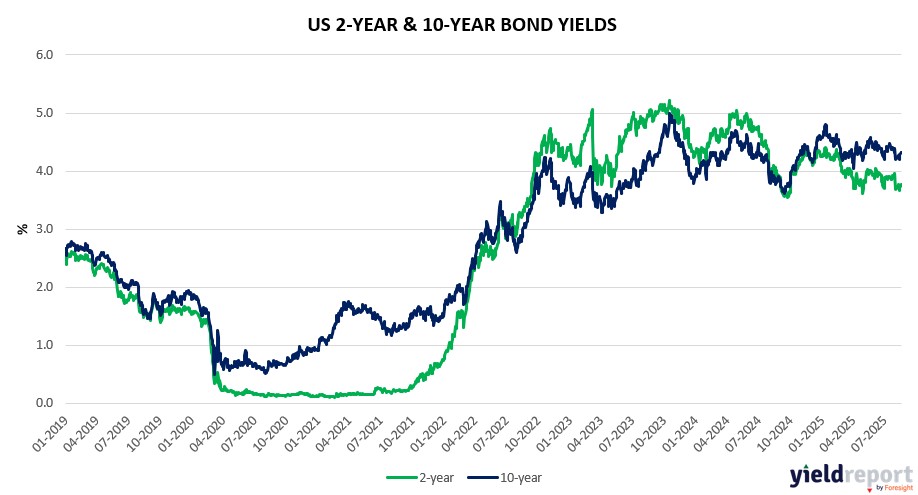

| United States 2-year bond (%) | 3.764 | 3.763 | 0.001 |

| United States 10-year bond (%) | 4.316 | 4.322 | -0.006 |

| United States 30-year bond (%) | 4.9244 | 4.9213 | 0.0031 |

Overview of the Australian Bond Market

Australian government bond yields rose on August 21, 2025, as equity highs and PMI expansion reduced safe-haven appeal, though monthly declines reflect RBA easing path amid global de-escalation hopes from Ukraine talks’ progress—Trump’s Putin dialogue and potential concessions easing commodity risks. The 10-year yield climbed 3 basis points to 4.30% (+1 daily per data), 2-year +2 to 3.35%, 5-year +2 to 3.67%, 15-year +2 to 4.69%. Monthly down (10-year -1 bp), dovish despite data.

August PMIs (Composite 54.9) support gradual cuts post-3.60%, Bullock data-tied with “couple more” possible amid trade surplus. US PMIs beat (Manufacturing 53.3 vs. poll 49.5), Philly Fed miss (-0.3 vs. 7), Home Sales beat (4.01M vs. 3.92M), China extension influence.

Traders trimmed longs on records, Fed swaps ~60% September 25 bp from 4.25%-4.5%, pacts/peace hopes sustaining higher rates but PMIs affirm soft landing, bonds hedging volatility if Ukraine deal delays. Locally, yields firmed on sector gains, shorter focus. Tomorrow’s US jobless (poll 225k), Philly could sway if weak, aiding bonds, though vigour caps. Dealers’ stable auctions August-October per guidance, summit aiding diversification.

Overview of the US Bond Market

Money markets priced in about a 70% chance of a Federal Reserve rate cut in September, down from more than 90% a week earlier, as stronger U.S. economic data tempered expectations for easing. The adjustment came ahead of Fed Chair Jerome Powell’s highly anticipated Jackson Hole speech on Friday, where investors hope for policy clarity.

Several Fed officials struck a hawkish tone. Cleveland Fed President Beth Hammack said she wouldn’t support a cut if voting immediately, while Atlanta’s Raphael Bostic reiterated his view of only one cut this year. Kansas City’s Jeffrey Schmid emphasized inflation remains the bigger risk, and Chicago’s Austan Goolsbee warned against reading too much into one “dangerous” inflation data point despite recent improvements.

Recent data has complicated the Fed’s outlook. Jobless claims rose, pointing to labour market cooling, but manufacturing PMIs surprised on the upside, expanding at the fastest pace since 2022. This resilience prompted traders to scale back rate-cut bets. Analysts highlighted the Fed’s dilemma: inflation remains above target while labour market conditions weaken.

eToro’s Bret Kenwell noted the Fed faces “pressures to cut as inflation rises and jobs slow,” pulling policy in opposite directions. BNP Paribas’s Calvin Tse said markets may be surprised hawkishly if Powell sticks to July’s reaction framework, signalling patience. Plante Moran’s Jim Baird cautioned that cutting too soon risks fueling inflation expectations, while moving too slowly risks a deeper labour slowdown.

Meanwhile, political pressures intensified. The Justice Department signalled a potential probe into Fed Governor Lisa Cook over alleged mortgage irregularities, while Trump allies renewed calls for her removal. In global markets, oil rose after a U.S. trade official warned of additional tariffs on India over Russian crude imports.