JCB find the YieldReport to be an invaluable summary of all debt market activity. Whilst we are focussed on the highest grade bonds it is important to see what is..Angus Coote, Executive Director, JCB Active Bond Fund

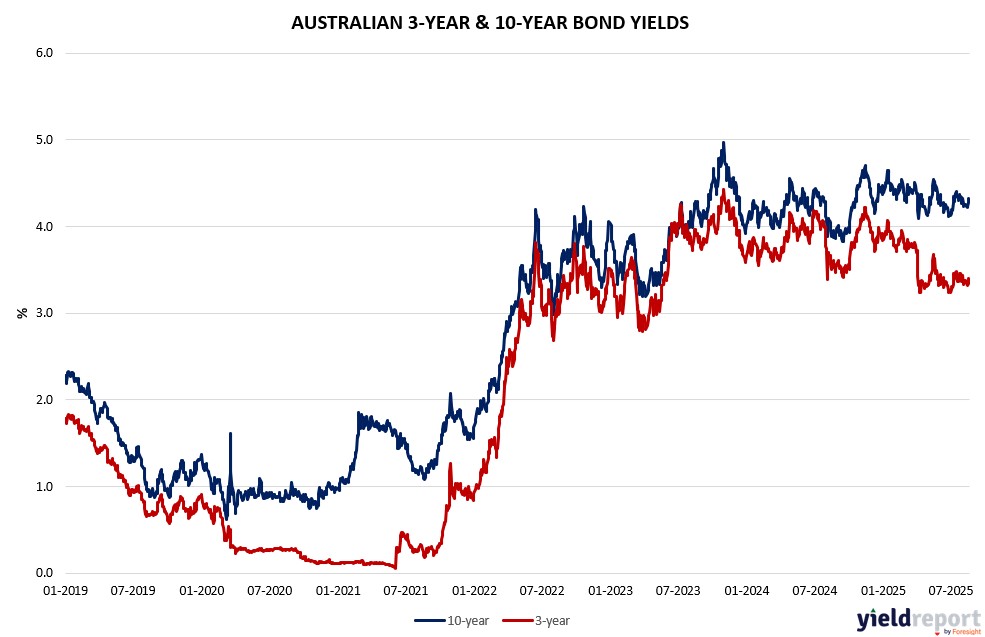

Australian yields rose on August 22, 2025, as market dip and Ukraine talks’ optimism (Trump-Putin call, potential truce reducing energy risks) spurred risk-on flows, though monthly upticks limited amid dovish RBA signals. The 10-year yield climbed 4 basis points to 4.31%, 2-year +2 to 3.35%, 5-year +3 to 3.67%, 15-year +2 to 4.68%. Monthly up (10-year +2 bp), cautious despite PMIs.

August PMIs (Composite 54.9) support gradual cuts post-3.60%, Bullock data-dependent with trade surplus boost. US jobless 235k (above poll), Philly -0.3 (miss), PMIs/Home Sales beat, China extension influence.

Traders pared longs on uranium/energy gains, Fed swaps ~60% September 25 bp from 4.25%-4.5%, pacts/summit progress sustaining higher-rates but PMIs affirm soft landing, bonds hedging volatility if Ukraine delays. Locally, yields firmed on sector rotations, shorter focus. Tomorrow’s US jobless (poll 230k) could sway if high, aiding bonds, though vigor caps. Dealers stable auctions August-October per guidance, talks aiding diversification.

Overview of the US Bond Market

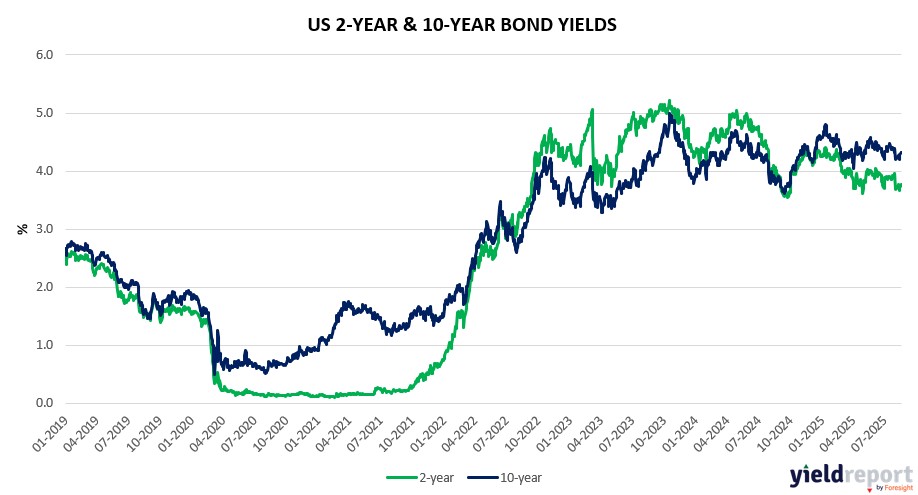

Bond traders boosted Treasuries as yields fell on Powell’s dovish Jackson Hole speech signaling cuts despite tariff bumps, bracing for PMIs amid media deregulation debates. The 10-year yield dropped to 4.26% (down 5 basis points from prior), 2-year to 3.69% (-6 bp), 30-year to 4.91% (flat). Shorter maturities rallied as oil rose 1.01% to $63.78/barrel, gold +1.24% to $3,377.60, Ukraine talks’ promise (Trump-Putin call, potential deal) easing energy risks.

August jobless 235k (above poll), Philly -0.3 (miss), PMIs beat, Home Sales beat counter industrial weakness. FCC’s TV cap push, enabling mergers, highlights Trump deregulation impacting bonds via consolidation.

JPMorgan survey net longs expanded post-speech, bullish shift, swaps ~89% September 25 bp cut, half-point year-end. Powell notes tariffs as onetime shift, resisting Trump easing amid dissent, yields down. Trade war resilience via EU/Japan, China extension favors higher-rates-longer, though PMIs affirm soft landing, bonds hedging volatility from Ukraine summit if delays.

Cash surveys to August 21: more longs, fewer shorts, net high. CFTC August 19: asset managers added net longs $18 million per basis point in 2-year, leveraged trimmed 30-year shorts $5 million.

Dealers unchanged auctions August-October per guidance, 10-year +$1 billion recent.