| Price | Change | % Chg | |

|---|---|---|---|

| Dow | 45,636.90 | 71.67 | 0.16% |

| S&P 500 | 6,501.86 | 20.46 | 0.32% |

| Nasdaq | 21,705.16 | 115.02 | 0.53% |

| VIX | 14.43 | -0.42 | -2.83% |

| Gold | 3,477.60 | 3.3 | 0.09% |

| Oil | 64.17 | -0.43 | -0.67% |

OVERVIEW OF THE US MARKET

The S&P 500 gained 0.3% to a record, and the Nasdaq 100 added 0.6%, lifted partly by resilience in tech stocks, including Nvidia, which rebounded after analysts raised price targets despite cautious guidance.

Market sentiment was shaped by data showing US GDP expanded at a faster 3.3% annualized pace in Q2, versus the previously reported 3%. The results underscored the strength of consumer spending and suggested the economy remains resilient. While this eased immediate recession concerns, it also raised doubts about inflation pressures, with the upcoming core personal consumption expenditures (PCE) report expected to show a 2.9% annual rise in July, the fastest in five months. Investors are therefore closely watching whether inflation aligns with expectations. A softer print could reinforce bets on a September Fed rate cut, while a hotter number may temper optimism.

Federal Reserve officials continue to signal flexibility. Chair Jerome Powell recently acknowledged growing risks in the labor market, interpreted by investors as an opening for further easing despite inflation staying above target. Markets are currently pricing in about 20 basis points of September easing, with a second cut likely by year-end. Treasury yields reflected this outlook: the two-year yield rose slightly to 3.63%, while longer-dated bonds rallied.

In currencies, the dollar index fell 0.3%, with the yen holding gains and the euro steady. The Australian and offshore Chinese yuan remained unchanged, reflecting subdued FX activity. Bitcoin rose 0.4% to $112,396 and Ether gained 0.9% to $4,498, continuing a recovery in digital assets.

Commodities were more volatile. Oil slipped 0.6% to $64.23 a barrel, retracing some of Thursday’s gains that had been driven by fading hopes of a Russia-Ukraine peace deal. Statements from German Chancellor Friedrich Merz downplayed the likelihood of direct talks between Vladimir Putin and Volodymyr Zelenskiy, despite earlier suggestions by US President Donald Trump. This uncertainty kept energy markets cautious. Gold prices were steady, reflecting demand for safe havens.

Corporate earnings remained in focus. Dell Technologies fell in extended trade after reporting weaker sales of AI servers and lower-than-expected profit margins in the segment. Meanwhile, investors awaited Alibaba’s earnings, with peers’ results highlighting intense competition across China’s e-commerce sector.

Elsewhere, geopolitical and trade developments continued to influence sentiment. The European Union moved to eliminate tariffs on US industrial goods and extend preferential treatment to some American agricultural products. In US politics, Fed Governor Lisa Cook faced scrutiny over a mortgage dispute, though her legal team attributed it to a clerical error.

Overall, global markets remain delicately balanced between optimism about US economic resilience and caution over persistent inflation. For Asia, the immediate direction hinges on Friday’s PCE report, which could either cement expectations of Fed easing or reignite inflation worries.

OVERVIEW OF THE AUSTRALIAN MARKET

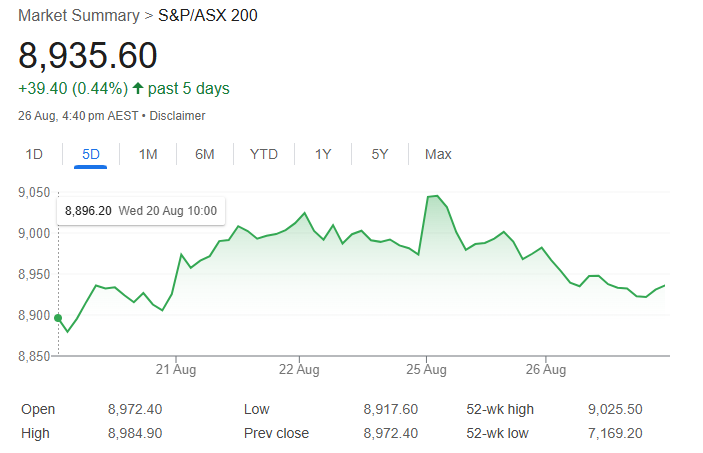

The Australian share market eked out modest gains on August 28, 2025, amid volatile earnings reports and a lull in broader activity as investors awaited U.S. inflation data, closing on session highs despite poor breadth. The S&P/ASX 200 rose 0.22% to 8,980.0, while the broader All Ordinaries added 0.11% to 9,241.1. Small-caps underperformed with the Small Ords down 0.67%, and advancers lagged decliners 105 to 165 in the ASX 300, highlighting uneven sentiment.

Financials topped sectors with a 1.10% advance, powered by the big four banks—NAB (+2.4%), CBA (+2.1%), Westpac (+1.3%), and ANZ (+0.9%)—more than offsetting Bank of Queensland’s 7.7% drop on a strategy and trading update. Real Estate climbed 1.02%, boosted by Lifestyle Communities (+14.9%) after full-year results and Goodman Group (+2.0%). Industrials gained 0.89%, led by Qantas Airways (+9.1%) following a 28.3% profit surge to $1.6 billion and CEO comments on strong delivery. Consumer Staples rose 0.88% and Consumer Discretionary added 0.76%, but Energy plunged 2.39% amid global oil pressures, with Woodside Energy down 3.3% and Santos -0.7%. Health Care fell 1.72% as Ramsay Health Care tumbled 10.5% on weaker-than-expected margins in Australia and the UK, and Telix Pharmaceuticals cratered 18.8% on a U.S. FDA setback for its imaging agent. Materials slipped 0.54%, with BHP -0.7%, Rio Tinto -1.1%, and Fortescue +1.5%, while lithium stocks pared Wednesday’s gains on falling futures.

Standout movers included IDP Education (+29.7%) on FY25 results and a multi-year cost transformation amid student restrictions, Kaili Resources (+15.3%) ahead of drilling, Genusplus Group (+13.9%), Eagers Automotive (+12.0%), Aeris Resources (+11.9%), Invictus Energy (+11.5%), Tabcorp (+9.7%), Nuix (+9.1%), Titomic (+8.7%), Duratec (+8.5%), Jumbo Interactive (+7.0%), Generation Development Group (+6.8%), Hot Chili (+6.4%), DUG Technology (+5.5%), Adairs (+5.4%), and Solvar (+5.4%). On the downside, Nine Entertainment (-12.2%) on a CFO appointment, Electro Optic Systems (-10.3%), Archtis (-9.2%), Core Lithium (-8.3%), Macquarie Technology Group (-8.2%), Findi (-8.0%), Clarity Pharmaceuticals (-7.6%), Clinuvel Pharmaceuticals (-7.5%), South32 (-7.2%) after FY25 results, and Karoon Energy (-6.6%).

The AUD/USD rose 0.08% to 0.6511. Q2 capital expenditure grew just 0.2%, missing the 0.7% Reuters poll, potentially easing RBA rate cut timelines after July’s CPI surprise, while U.S. GDP was revised higher to 3.3% and jobless claims fell to 229k—both better than expected—ahead of Friday’s PCE release that could spark volatility.