| Close | Previous Close | Change | |

|---|---|---|---|

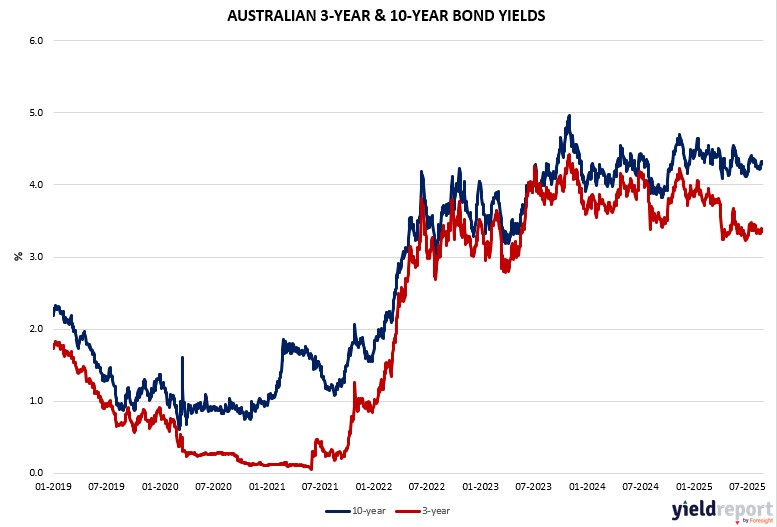

| Australian 3-year bond (%) | 3.358 | 3.386 | -0.028 |

| Australian 10-year bond (%) | 4.291 | 4.32 | -0.029 |

| Australian 30-year bond (%) | 5.053 | 5.068 | -0.015 |

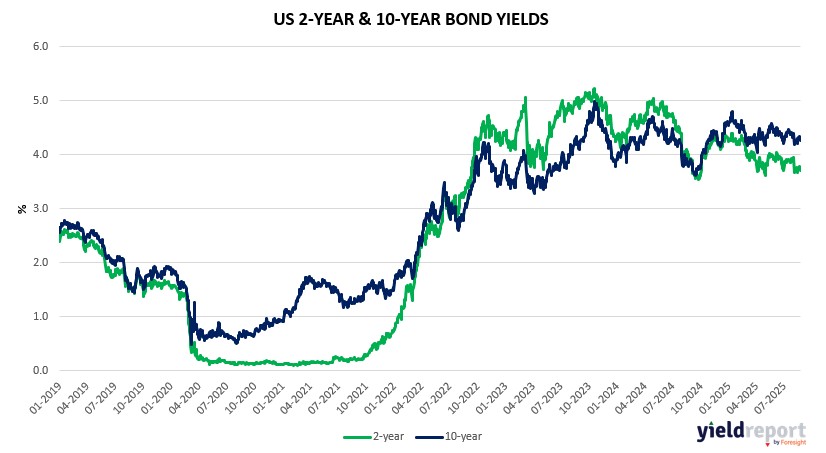

| United States 2-year bond (%) | 3.713 | 3.785 | -0.072 |

| United States 10-year bond (%) | 4.269 | 4.332 | -0.063 |

| United States 30-year bond (%) | 4.8928 | 4.9275 | -0.0347 |

Overview of the Australian Bond Market

Australian government bond yields dipped on August 25, 2025, as market reset and Powell’s dovish speech—citing shifting risks to jobs/growth, tariffs as one-time shift—ramped cut odds to 89% for September, blending with Ukraine talks’ promise (Trump-Putin call, potential de-escalation easing energy risks). The 10-year yield fell 2 basis points to 4.29%, 2-year -1 to 3.34%, 5-year -2 to 3.65%, 15-year -1 to 4.67%. Monthly down (10-year -5 bp), reflecting easing bias despite PMIs.

August PMIs (Composite 54.9) support gradual cuts post-3.60%, Bullock data-tied amid trade surplus. US jobless 235k (above poll), Philly -0.3 (miss), PMIs/Home Sales beat, China extension influence.

Traders added longs post-speech, Fed swaps ~89% September 25 bp from 4.25%-4.5%, pacts/summit progress sustaining higher-rates but PMIs affirm soft landing, bonds hedging volatility if Ukraine delays. Locally, yields eased on resource rotations, shorter focus. Tomorrow’s US jobless (poll 230k) could sway if high, aiding bonds, though vigor caps. Dealers stable auctions August-October per guidance, talks/FCC deregulation aiding diversification.

Overview of the US Bond Market

Bond markets reacted to Federal Reserve Chair Powell’s dovish pivot at Jackson Hole with markets interpreting it as a signal towards easier monetary policy. This triggered a flattening of the Treasury yield curve, while long-term yields, including those on 10-year notes, eased modestly. Investors continued to price in high odds for a September rate cut and further easing by year-end. Although bond yields slipped slightly, the move was subdued, suggesting that even with Powell’s shift, long-term rates may not drop significantly. It reflects cautious optimism amid uncertainties around inflation and economic resilience.

The Federal Reserve’s annual Jackson Hole symposium, typically a relaxed gathering for central bankers and economists, was unusually tense this year, underscoring the difficult policy challenges facing the US central bank. Chair Jerome Powell used his keynote speech to signal that an interest-rate cut is possible at the Fed’s September meeting, but divisions among policymakers remain sharp. Powell acknowledged the “challenging situation,” with inflation still above the Fed’s 2% goal and labor market conditions weakening, creating conflicting policy signals.

Chicago Fed President Austan Goolsbee described the environment as one of “cross-currents,” with the toughest challenge being timing policy shifts at moments of transition. Powell highlighted uncertainty over whether tariffs will reignite inflation more persistently and called the current labor market dynamic of both falling demand and declining supply “curious.” While last year’s Jackson Hole gathering strongly favored rate cuts, this year support is more fragmented, reflecting disagreements among officials about whether inflation or employment poses the greater risk. Two governors dissented in July when no cut was delivered, raising the possibility of more split votes if cuts begin in September.

The political backdrop added to the unease. President Donald Trump has escalated pressure on the Fed, seeking lower rates and threatening Fed officials directly. During Powell’s speech, Trump said he would fire Governor Lisa Cook if she didn’t resign over mortgage fraud allegations, intensifying scrutiny of the central bank’s independence. Security at the conference was heightened, and one Trump supporter was forcibly removed after confronting Cook. Powell’s term as chair ends in May, and Trump has indicated he will name new officials, including economic adviser Stephen Miran, which could tilt the Fed more toward his policy preferences.

Despite the political noise, much of the conference focused on substantive economic debates. Data show inflation stalled above target, with signs of broadening beyond tariff-affected goods, while job growth slowed over the summer. Yet unemployment remains low, leaving policymakers uncertain about the economy’s true trajectory. Many economists stressed the importance of relying on rigorous research and evidence, with Harvard professor Karen Dynan noting the value of grounding policy in expertise rather than political pressures.

Powell also introduced a new policy framework to replace the 2020 version that had emphasized persistently low inflation. The revised document re-centers the Fed’s dual mandate of maximum employment and price stability, removing language specific to the pre-pandemic era. Analysts said the shift clarified priorities and reaffirmed independence. Carolin Pflueger of the University of Chicago highlighted Powell’s emphasis on focusing solely on inflation and unemployment, which drew appreciation from conference attendees. Powell received a standing ovation from global policymakers, reflecting recognition of the Fed’s critical role beyond US borders.

International markets reacted immediately. The euro strengthened 1% against the dollar after Powell’s remarks, signaling potential challenges for euro-area inflation and growth. Maurice Obstfeld of the Peterson Institute noted that a US slowdown would likely spill over abroad, underscoring the global stakes of Fed decisions.

Overall, the Jackson Hole meeting revealed deep internal divisions, growing political pressures, and high uncertainty, leaving investors braced for a consequential September decision.