| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.372 | 3.358 | 0.014 |

| Australian 10-year bond (%) | 4.321 | 4.291 | 0.03 |

| Australian 30-year bond (%) | 5.073 | 5.053 | 0.02 |

| United States 2-year bond (%) | 3.709 | 3.713 | -0.004 |

| United States 10-year bond (%) | 4.295 | 4.269 | 0.026 |

| United States 30-year bond (%) | 4.9315 | 4.8928 | 0.0387 |

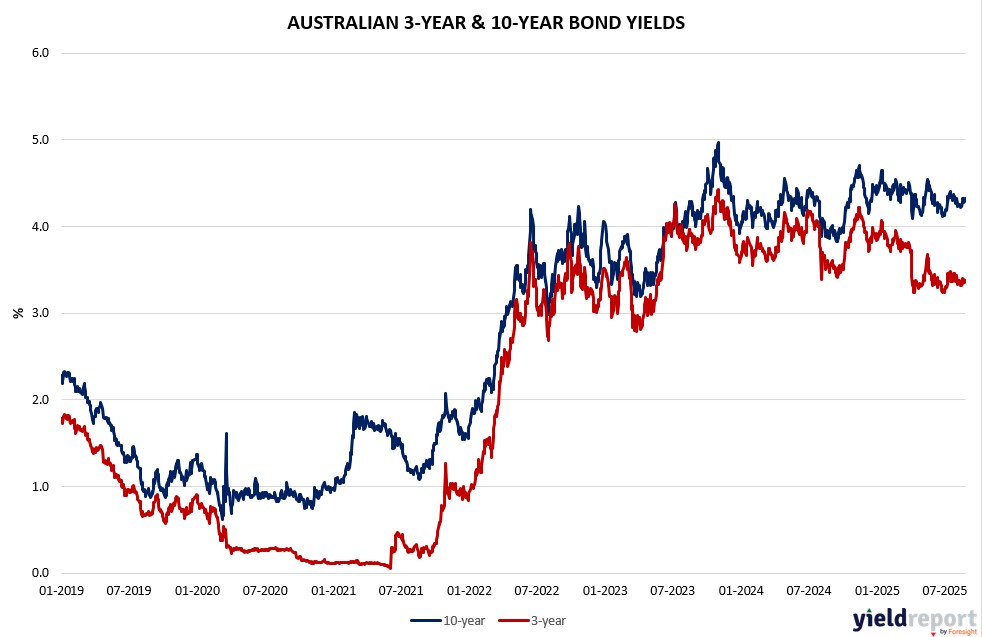

Overview of the Australian Bond Market

Australian government bonds were mixed on August 27, 2025, with yields little changed as hotter domestic inflation tempered rate cut bets, while global concerns over U.S. political pressure on the Fed added caution. The 10-year yield eased 1 basis point to 4.30%, the 2-year held at 3.34%, the 5-year was flat at 3.65%, and the 15-year unchanged at 4.68%. Month-to-date, shorter tenors dipped 8-9 bps, reflecting some easing expectations, but the curve’s steepness highlights persistent inflation risks.

The ABS’s July CPI surge to 2.8% YY—up from 1.9% prior and beating forecasts—backs the RBA’s patient stance, reducing odds of near-term cuts and pressuring yields higher intraday before stabilization. Globally, President Trump’s push to fire Fed Governor Lisa Cook tests central bank independence, potentially eroding U.S. dollar confidence and boosting safe-haven gold, which could spill over to Australian assets given commodity ties. Analysts note this may make gold a “safe haven of choice,” indirectly supporting resource-linked bonds. Meanwhile, U.S.-Europe tariff reductions on industrial goods and ongoing U.S.-China truce talks (possible 90-day extension) ease some trade uncertainties, but India’s bracing for Trump duties adds volatility. U.S. crude stockpiles fell 2.4 million barrels—more than expected—lifting energy sentiment, while German consumer gloom and Bank of Canada’s reaffirmed 2% inflation target underscore global caution.

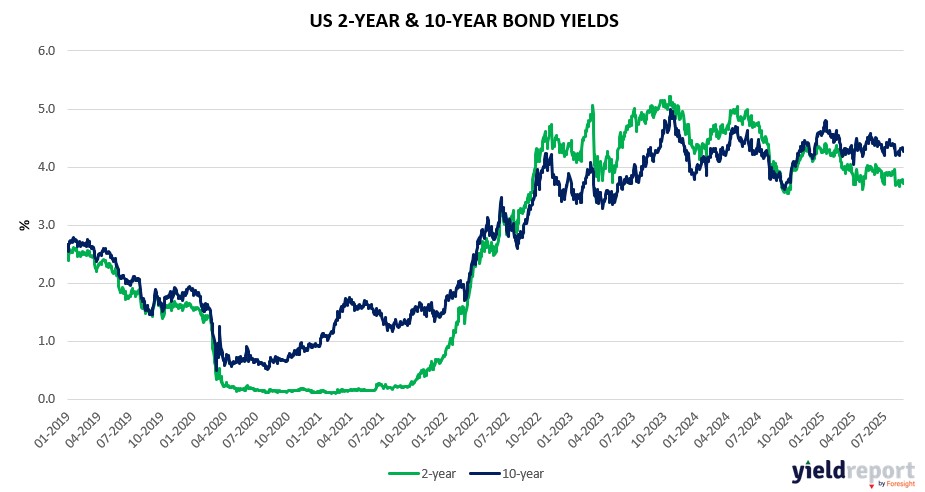

Overview of the US Bond Market

U.S. Treasuries softened on August 27, 2025, with yields ticking higher as tariff progress and resilient data countered Fed independence fears, though positioning remains cautious ahead of key releases. The 10-year yield fell 15 basis points month-to-date to 4.23%, the 2-year dropped 31 bps to 3.61%, the 5-year eased 26 bps to 3.70%, and the 30-year held flat at 4.92%. Shorter bills like the 3-month declined 17 bps to 4.17%, signaling some easing bets persist.

Traders trimmed aggressive cut wagers amid U.S. economy’s tariff resilience—deals with Europe and Japan dissipate uncertainty—bolstering views for higher-for-longer rates. Yet, Trump’s aggression on the Fed, challenging Governor Cook’s removal post-Supreme Court signals on independence, clouds the medium-term outlook, risking higher inflation and eroding Treasury appeal versus gold. Swap contracts price a 60% chance of a 25 bps September cut, but today’s GDP (3.1% poll) and jobless claims, plus tomorrow’s PCE (core MM 0.3%), could amplify FOMC dissent if soft. U.S. crude drawdowns (2.4M barrels >1.9M expected) and nuclear energy expansion for AI demand add inflationary pressures, while German gloom and Bank of Canada’s 2% target reaffirmation highlight global divergence. Sovereign wealth fund performance studies note U.S. potential despite mediocrity elsewhere, but tariff extensions (U.S.-China talks for 90 days) may stabilize flows.