| Close | Previous Close | Change | |

|---|---|---|---|

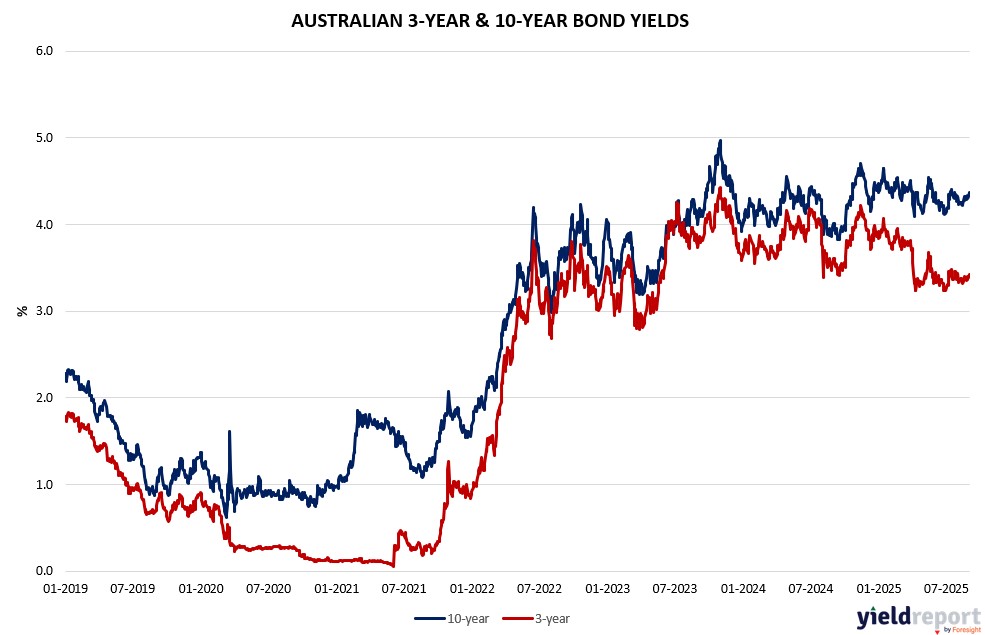

| Australian 3-year bond (%) | 3.424 | 3.394 | 0.03 |

| Australian 10-year bond (%) | 4.364 | 4.325 | 0.039 |

| Australian 30-year bond (%) | 5.126 | 5.082 | 0.044 |

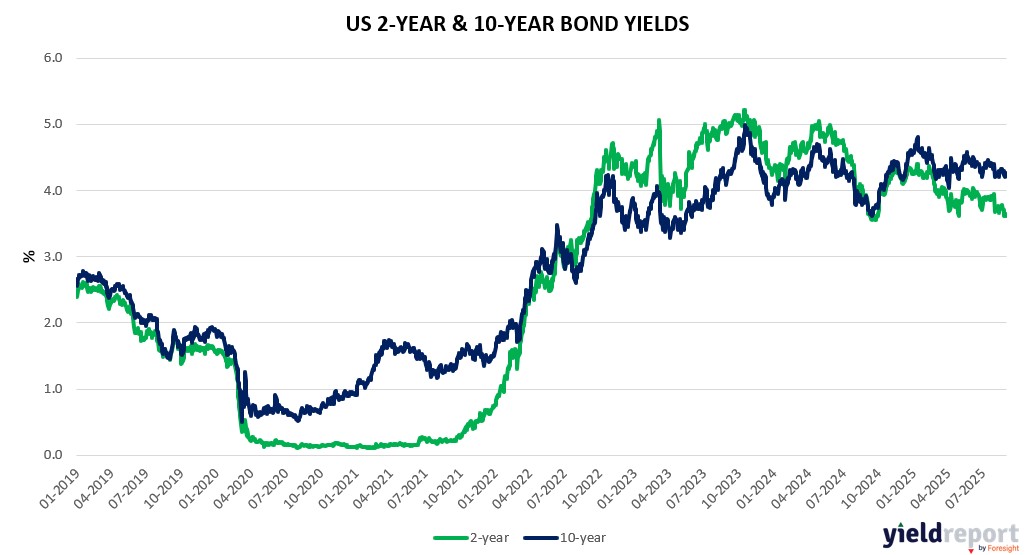

| United States 2-year bond (%) | 3.647 | 3.623 | 0.024 |

| United States 10-year bond (%) | 4.269 | 4.226 | 0.043 |

| United States 30-year bond (%) | 4.9634 | 4.918 | 0.0454 |

Overview of the Australian Bond Market

Australian government bonds weakened on September 2, 2025, with yields rising as better-than-expected current account data tempered easing bets, amid gold’s record rally and global haven flows post-US holiday. The 10-year yield climbed 4 basis points to 4.36%, the 2-year added 2 bps to 3.37%, the 5-year gained 3 bps to 3.70%, and the 15-year rose 4 bps to 4.73%. In August, yields increased modestly—10-year up ~9 bps overall—reflecting RBA patience after July CPI surprise, though global dovish shifts capped rises.

Q2 current account -13.7B (surpassing -16B forecast) and +0.1% net exports bolster growth views pre-GDP, blending with bond selling as Trump’s inflation claims and Fed interference—firing attempts on Cook—risk politicized policy, inflating long-term costs and eroding US asset trust, spilling to Aussie yields via haven demand as gold hits $US3,578. Tariff truce talks (90-day extension possible) and EU deals ease trade wars, but Ukraine escalation and weakening US ISM (48.7 vs 49) underscore divergence, supporting higher-for-longer locally.

Upcoming S&P Global Services PMI (55.8 expected) and GDP (1.6% YY poll) could sway RBA, with swaps at ~60% Fed September cut amid data resilience. Positioning cautious per CFTC, eyeing diversified plays as US deficits worsen.

Overview of the US Bond Market

U.S. Treasuries weakened at the start of September, with the 30-year yield climbing toward 5% in tandem with a selloff in long-dated European bonds. The move comes during a historically challenging month for duration risk, as long-term government bonds have averaged 2% losses each September over the past decade. On Tuesday, benchmark yields settled about 4 basis points higher at the long end, retracing session highs after weaker-than-expected ISM manufacturing data showed soft activity, employment, and prices paid, though new orders improved.

Selling pressure was also fueled by a surge in corporate debt issuance, with 27 investment-grade deals launched in the post-Labor Day rush. Analysts suggested as much as $160 billion in supply could come this month, compounding the seasonal weakness. Kathy Jones of Charles Schwab noted that markets are demanding a higher term premium until clearer economic signals or policy coherence emerges, with Friday’s jobs report seen as pivotal.

Global dynamics added pressure: U.K. 30-year yields reached levels last seen in 1998, while French yields rose to 4.51%. Pimco’s Michael Cudzil and Natixis’s John Briggs highlighted that yields around 5% may not hold but underscore persistent concerns about long-end vulnerability.

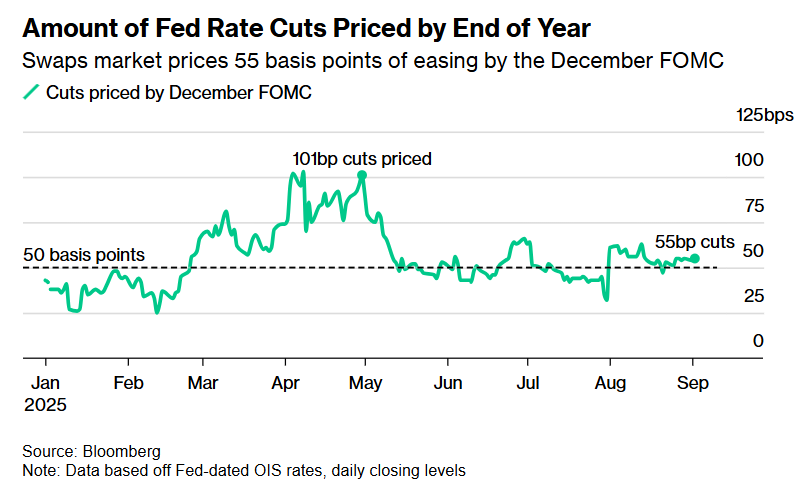

Markets are increasingly pricing Federal Reserve easing, with fed funds futures assigning a 92% chance of a quarter-point cut in September and 55 basis points by year-end. While Governor Christopher Waller backed a 25-basis-point reduction, he left the door open to larger cuts if labor data deteriorates. Economists expect Friday’s report to show 75,000 new jobs and unemployment rising to 4.3%. Weak outcomes could push traders to consider a half-point cut, amplifying volatility in long bonds already pressured by global fiscal strains and heavy issuance.