Elstree Investment Management is a fixed interest fund specialising in a diverse range of floating rate credit securities including mostly hybrid securities. It has released a report on the state of the hybrid market which notes it has been six years since the end of the GFC and hence getting to the latter stages of the credit cycle.

Credit default activity has not increased yet (YieldReport has another article on this very topic) and it may be time to start assessing the likelihood of this happening. The Elstree report say margins of securities in the credit markets often anticipate default increases and as such it is a useful early warning system on corporate health.

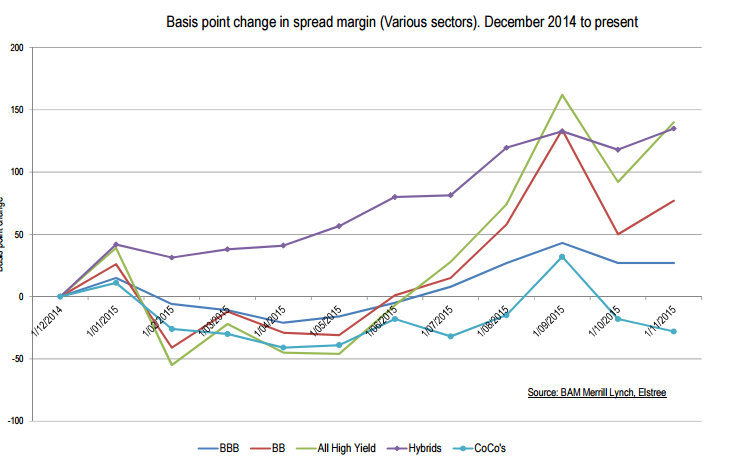

Analysis in the chart below shows margin changes since the start of 2015 for a range of credit and bank capital instruments. Elstree thinks the margin contraction at the start of 2015 was “chase for yield” in an environment where no one was thinking about issuer defaults. However, by mid-2015, ructions in the Chinese financial markets and some specific credit issue in commodity companies led to concerns among investors in local markets. Credit margins soared as a result. One explanation included the fall in commodities prices (on weak Chinese demand and over-supply) put resource companies under financial pressure, with doubt over growth prospects which has ramifications for all Australian corporate issuers.

High yield bonds were the worst affected of the sectors but Elstree was intrigued by the behaviour of local hybrids. They noticed European CoCo* margins and hybrid margins had diverged (see above). CoCo margins are seen as a proxy indicator of the presence of concerns regarding the global banking system and the current state of CoCo margins would thus indicate there are not any. Therefore the difference between the two segments is not due to global risks. Elstree then considered domestic risks as the source of the difference. This possibility was discounted as local banks had strengthened their balance sheets through equity capital raisings recently and profitability is currently high. Another factor which should be considered is the type of investor holding hybrid securities. In the UK, retail investors are not allowed to buy hybrids – it is exclusively the domain of wholesale or institutional investors. In Australia, it is almost the opposite – the majority of hybrids are owned by retail investors. This may result in some differences in pricing and volatility.

*Contingent convertible bonds: convertible notes/bonds are largely issued in Europe with a conversion clause dependent on the issuer’s share price. For a more on CoCos click here