| Close | Previous Close | Change | |

|---|---|---|---|

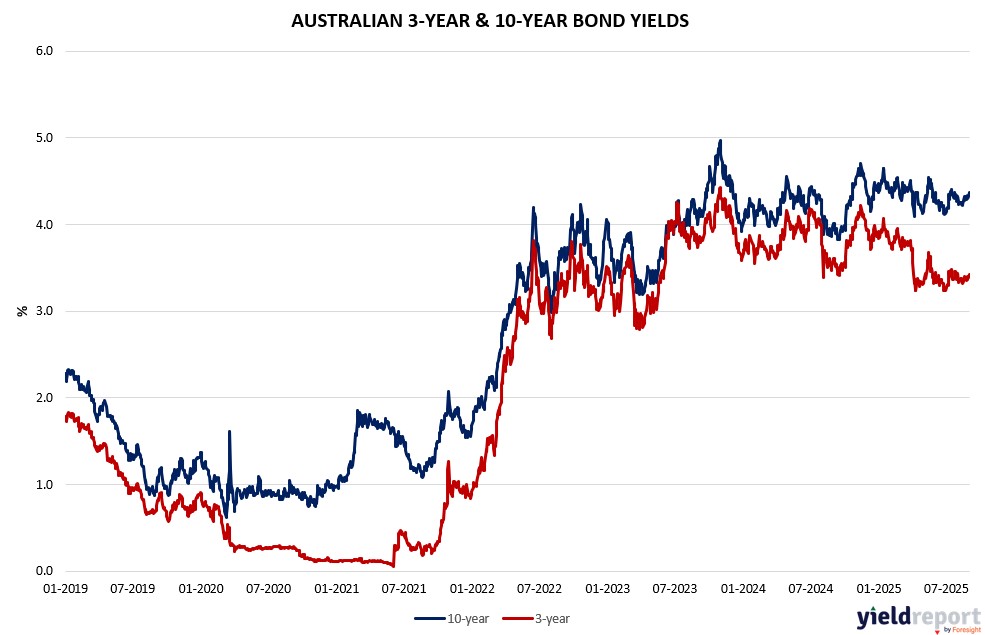

| Australian 3-year bond (%) | 3.508 | 3.424 | 0.084 |

| Australian 10-year bond (%) | 4.433 | 4.364 | 0.069 |

| Australian 30-year bond (%) | 5.182 | 5.126 | 0.056 |

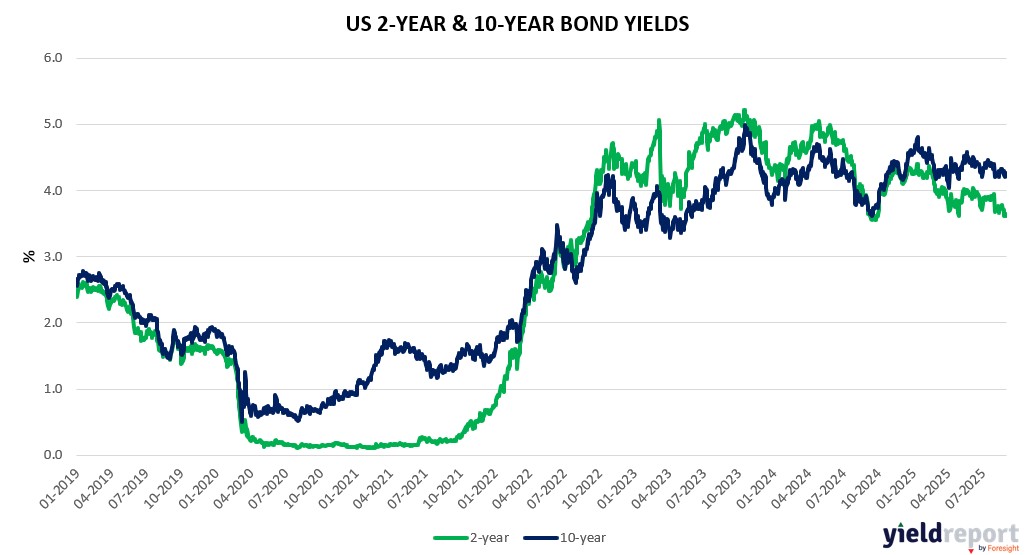

| United States 2-year bond (%) | 3.66 | 3.647 | 0.013 |

| United States 10-year bond (%) | 4.293 | 4.269 | 0.024 |

| United States 30-year bond (%) | 4.9883 | 4.9634 | 0.0249 |

Overview of the Australian Bond Market

Australian government bonds weakened further on September 3, 2025, with yields rising amid stronger-than-expected GDP data and global selloff pressures from US policy turmoil, extending August’s uptick. The 10-year yield climbed 1 basis point to 4.37%, the 2-year added 4 bps to 3.42%, the 5-year gained 3 bps to 3.74%, and the 15-year held flat at 4.74%. In August, yields rose—10-year up ~11 bps—reflecting fiscal worries and RBA hold post-CPI surprise, though global easing capped gains.

Q2 GDP at 0.6% QQ (surpassing 0.5% forecast), 1.8% YY bolsters higher-for-longer views, blending with bond pressure as Trump’s Fed interference—court fights over independence—and tariff legality rulings risk inflation spikes, eroding US credibility and spilling to Aussie yields via risk-off flows as gold surges to $US3,578.

Tariff truce extensions and EU deals mitigate trade wars, but domestic unrest (National Guard threats) and Ukraine tensions amplify haven demand, while weak US ISM (48.7 vs 49) reinforces Fed cuts, potentially easing cross-border pressures.

Upcoming goods balance (5000M expected) and services PMI (55.8 poll) may guide RBA, with swaps at ~60% Fed September cut amid resilience. Positioning bearish per CFTC, favoring havens as US deficits and meddling converge.

Overview of the US Bond Market

Bond traders boosted easing wagers on September 3, 2025, as soft job data reinforced Fed cut odds, easing earlier selloff pressures amid global fiscal and political strains. The 10-year yield fell 1 basis point month-to-date to 4.21%, the 2-year dropped 7 bps to 3.61%, the 5-year eased 7 bps to 3.69%, and the 30-year rose 7 bps to 4.89%. Shorter ends like the 3-month declined 16 bps to 4.11%, signaling growth concerns.

Treasuries rallied after a $128 billion corporate debt rush siphoned demand, but long-end fragility persists as deficits and sticky inflation demand higher premia—US 30-year near 5%, Japan 20-year at 1999 highs, UK 30-year at 1998 levels—blending with Trump’s Fed meddling (independence legal fights) risking policy instability and inflation surges, eroding global trust amid tariff doubts and domestic unrest (Guard deployments). Beijing’s US fiber levies add trade frictions, though EU deals and extensions (90-day possible) mitigate, while Ukraine escalation boosts havens like gold.

Economic front: Job openings’ 10-month low tips Fed to 25 bps September cut per Boockvar, with payrolls eyed; factory orders -1.3% (better than -1.4%). TD’s Munoz/Goldberg bias long on dips if labor surprises weak.

This shift counters resilience against tariffs but amplifies bearish views on higher-for-longer amid QE unwind and budget binges—One Big Beautiful Bill adding $3.4T deficit. JPMorgan survey likely shows high shorts, CFTC data asset managers trimming longs, leveraged paring shorts in longs.

Dealers expect steady August-October auctions per April, 10-/5-year +$1B.