Summary

The great Australian dividend drought is here. Mining heavyweights are cutting payouts to eight-year lows while the ASX 200 soars to records – creating a dangerous disconnect for income investors. BHP’s dividend hit an eight-year low, Rio delivered its smallest payout in seven years, yet insurers are defying gravity with Suncorp surging 58% and QBE up 32.6%. At just 4.2% yield, Australia’s dividend appeal is fading fast compared to historical norms. Smart money is now tactical dividend harvesting across monthly cycles, potentially generating 50% more income than traditional approaches. The dividend game has fundamentally changed – those adapting will thrive.

Earnings Headwinds Lead to Lower Dividend Distributions

Australian dividend payouts are expected to fall to their lowest level in four years, reflecting weaker commodity prices, China’s slowdown, and a shift in corporate priorities toward debt reduction and growth investment.

Despite the ASX 200 reaching record highs earlier this year, dividend momentum has faltered since a resources-driven peak of $36 billion in early 2022. While payments will ramp up in August and September, lower overall payouts come amid heightened volatility, concerns about US tariffs, and cautious domestic sentiment despite an RBA rate cut.

Resources led the decline,with Mining companies being hardest hit. BHP, Rio Tinto and Fortescue all slashed dividends as profits weakened. BHP’s interim payout of US50 cents per share was its lowest in eight years, reflecting both weaker iron ore prices and a focus on growth projects in copper. Rio declared its smallest dividend in seven years, while Fortescue halved its interim payout.

Insurers had a standout reporting season, raising dividends significantly. Suncorp lifted payouts 58%, QBE 32.6% and IAG 18.2%, all supported by stronger profits and lower catastrophe claims. Banks were steadier: Commonwealth Bank increased its interim dividend to a record $2.25 per share, distributing $3.8 billion.

Several large corporations rewarded investors with dividend growth. Qantas resumed dividends for the first time since 2019, alongside a special payout. Telstra raised its interim dividend and announced a buyback, while CSL, Brambles, Origin Energy and Computershare also lifted payouts. In retail, Wesfarmers, JB Hi-Fi and Coles all increased dividends on the back of resilient consumer spending, though Woolworths cut its payout after a sharp profit drop. Notably, A2 Milk declared it’s first-ever dividend.

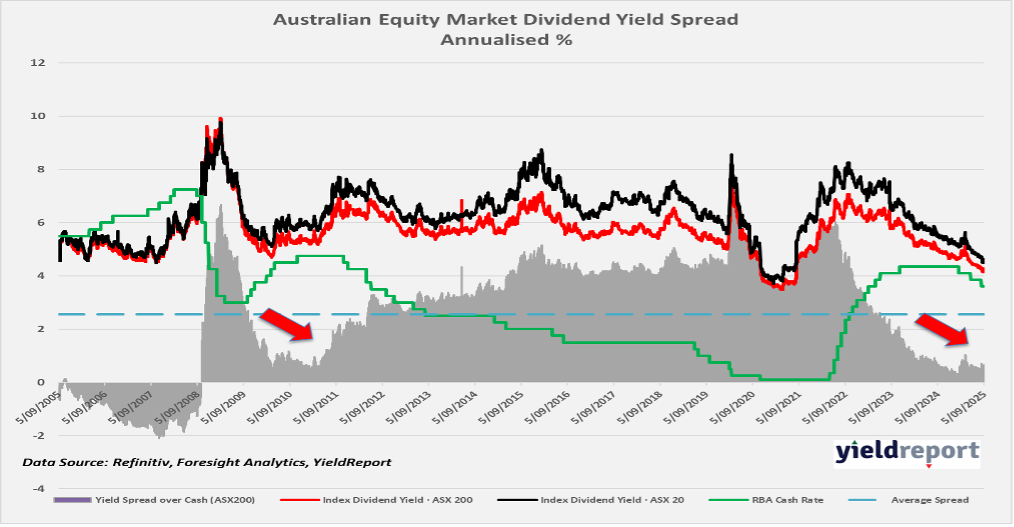

Despite solid company-level stories, aggregate yields remain under pressure. The ASX 200’s historic dividend yield sits at just 4.2% (ASX top 20 companies at 4.6%), below long-term average of 4.5%. High valuations, earnings growth pressures, and uncertainty around China and tariffs are weighing on distributions. Nonetheless, yields remain competitive internationally: the ASX 200’s 4.2% compares to 1.4% for the S&P 500 and 2.7% for the MSCI Asia-Pacific index.

Exhibit 1: Australian Equity Dividend Income Spread at Decade Lows

Significant Divergence at Sector Level

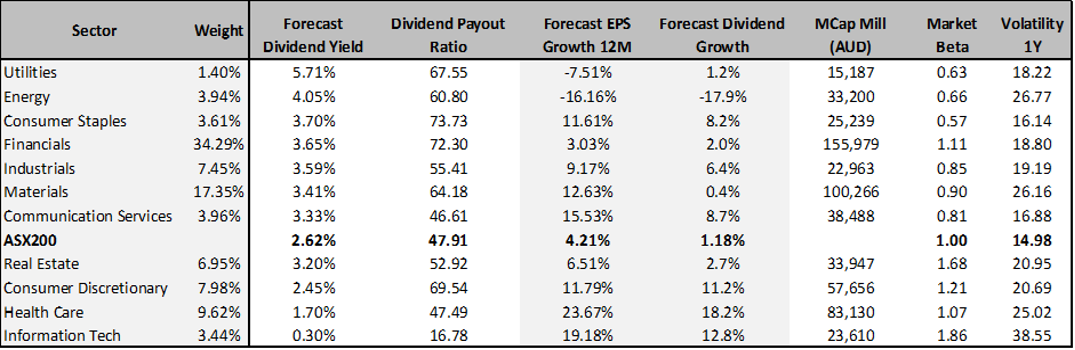

The ASX200 benchmark shows a forecast dividend yield of 2.62% and a dividend payout ratio of 47.91%, with projected earnings per share (EPS) growth of 4.21% over the next 12 months and dividend growth of 1.18%.

This reflects moderate income potential combined with cautious corporate earnings outlooks. Financials dominate the index with a 34.3% weighting, providing a 3.65% yield and stable dividend growth of 2.0%.

Despite modest EPS growth (3.03%), the sector’s large market cap and central role in the Australian economy make it a stabilising anchor. Materials, at 17.4% weight, project healthy EPS growth (12.63%) but almost no dividend expansion (0.4%), suggesting reinvestment over payouts.

High-growth opportunities lie in Health Care and Information Technology. Health Care (9.6% weight) offers the strongest EPS (23.67%) and dividend growth (18.2%), though with a low 1.70% yield. Information Technology (3.4% weight) forecasts 19.18% EPS growth and 12.8% dividend growth but provides only a 0.30% yield and carries the highest volatility (38.6%).

Defensive sectors offer stronger yields. Utilities (5.71%) and Energy (4.05%) lead in income, but both face earnings pressures, with Utilities’ EPS forecast at -7.5% and Energy’s at -16.2%. Energy also expects dividend contraction of -17.9%, reflecting weaker commodity dynamics. Consumer Staples (3.70% yield, 11.6% EPS growth) and Communication Services (3.33% yield, 15.5% EPS growth) balance steady dividends with growth potential.

Real Estate (3.20% yield) and Consumer Discretionary (2.45%) are positioned as cyclical plays, offering moderate EPS growth (6.5% and 11.8% respectively) but higher betas, reflecting greater sensitivity to market conditions

Exhibit 2: Fundamental Scorecard by Equity Sectors

Data Source: YieldReport, Foresight Analytics

Bottom line: Australia’s dividend cycle is softening from record highs, led by resources, but income opportunities remain. Insurers select blue chips, and consumer-facing businesses are providing stability, while attractive yields persist in energy, utilities and financials. Despite near-term headwinds, active stock selection and the support of franking credits continue to make dividends a valuable component of total returns for Australian investors.

Active Management is the Key

A strong dividend stock should deliver above-market yield, earnings and dividend growth, and exposure to long-term structural themes. Classic Australian dividend names include Telstra and Wesfarmers, but less obvious candidates can also stand out.

Another advantage of active management is the ability to tactically harvest dividends across the year. Different companies pay dividends at different times, depending on their financial year-ends. For example, most ASX companies with June year-ends pay around two distributions, while banks with off-cycle year-ends, as well as REITs and infrastructure firms, provide income in other months. By tactically overweighting stocks paying dividends each month, investors can boost portfolio yield.

Analysis by manager Ausbil suggests this can generate about 50% more dividends than the index. For funds such as the Ausbil Active Dividend Income Fund, this enables monthly income distributions rather than the typical semi-annual cycle, a key advantage for investors relying on consistent cash flow. A well-constructed active dividend portfolio combines multiple strong dividend names across sectors, balancing yield and growth. By doing so, it can deliver both higher income and competitive capital appreciation.

Equity income investing is not without risks. Unlike term deposits, hybrids, private credit and public traded bonds, equities can suffer cyclical drawdowns from market volatility, earnings shocks, or macroeconomic events. Banks suspending dividends during COVID-19 is a reminder of this risk.

However, a diversified portfolio approach helps reduce the impact of individual company setbacks. Sector diversification cushions cyclical swings, while long-term holding strategies allow investors to ride out market downturns. For long-term income investors, volatility can even present opportunities: adding to high-quality dividend stocks during periods of weakness can enhance future yields and total returns.