| Close | Previous Close | Change | |

|---|---|---|---|

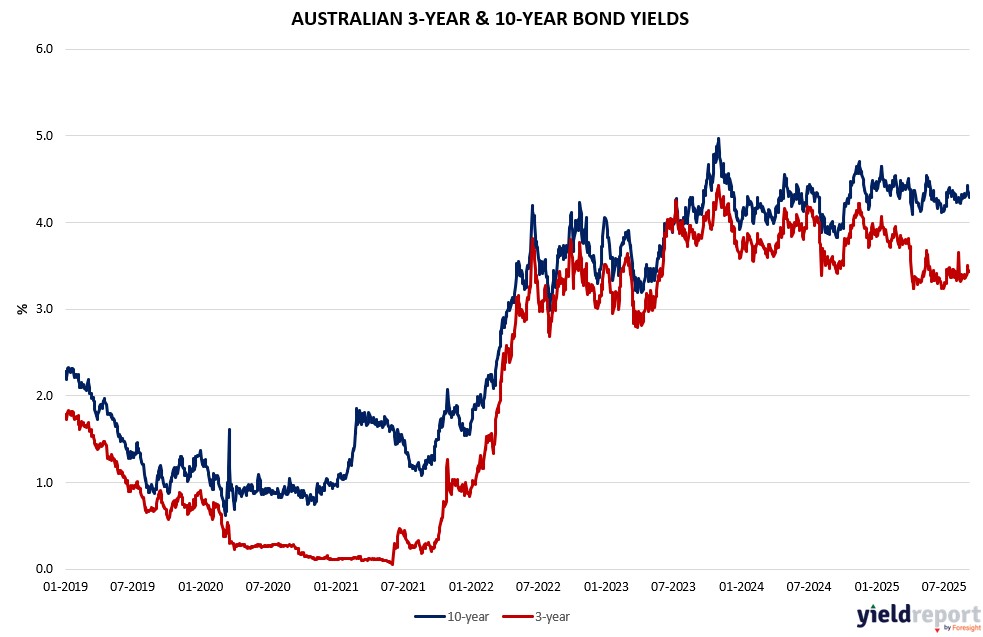

| Australian 3-year bond (%) | 3.43 | 3.447 | -0.017 |

| Australian 10-year bond (%) | 4.288 | 4.345 | -0.057 |

| Australian 30-year bond (%) | 5.031 | 5.093 | -0.062 |

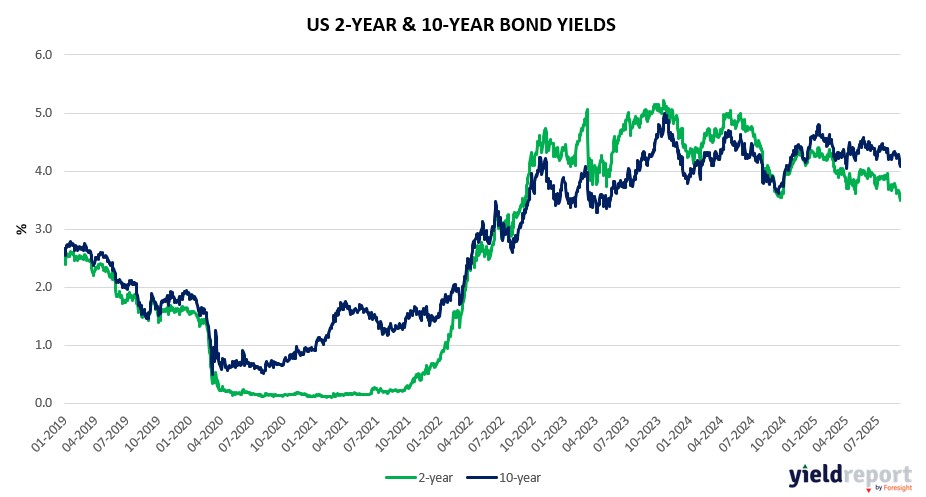

| United States 2-year bond (%) | 3.501 | 3.561 | -0.06 |

| United States 10-year bond (%) | 4.08 | 4.134 | -0.054 |

| United States 30-year bond (%) | 4.7665 | 4.8392 | -0.0727 |

Overview of the Australian Bond Market

Australian government bond yields eased across the curve on September 8, 2025, as a pullback in long-dated yields followed weaker-than-expected US jobs data, cooling some of the recent spike amid broader market choppiness. The 2-year yield dipped 4 basis points to 3.36 per cent, the 5-year fell 6 basis points to 3.65 per cent, the 10-year declined 9 basis points to 4.25 per cent, and the 15-year dropped 10 basis points to 4.61 per cent, reflecting a flight to safety in fixed income after the ASX’s modest decline and ongoing September seasonality.

The move aligns with a natural retracement from elevated levels driven by prior yield surges and a post-rally pullback in equities, though corporate earnings from recent seasons indicate underlying resilience. Globally, US Treasury yields have similarly softened in response to Friday’s employment print, with futures implying a roughly 60 per cent chance of a 25 basis-point Federal Reserve cut in September, potentially spilling over to influence Reserve Bank of Australia expectations as inflation remains in focus. Bond traders are trimming positions ahead of key US data releases this week, including producer prices on Tuesday, core CPI and headline CPI on Wednesday—both forecast at 0.3 per cent month-over-month with year-over-year readings of 3.1 per cent and 2.9 per cent respectively—and initial jobless claims alongside University of Michigan sentiment on Thursday, which could clarify the pace of Fed easing and its ripple effects on the Aussie dollar and local borrowing costs.

With the RBA’s benchmark rate steady and domestic surveys like Tuesday’s Westpac and NAB releases poised to gauge sentiment amid trade war echoes and commodity softness, the bond market’s bearish tilt persists on bets that rates stay higher for longer if US resilience holds. Recent deals easing global tariff uncertainties have bolstered this view, though stretched valuations in equities underscore the need for diversification. In the cash market, net long positions in Australian bonds have held steady, but investors remain cautious as swap contracts price in modest easing potential by year-end, contingent on softer Chinese producer prices and US inflation prints not reigniting yield pressures.

Overview of the US Bond Market