| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 45,711.34 | 196.39 | 0.43% |

| S&P 500 | 6,512.61 | 17.46 | 0.27% |

| Nasdaq | 21,879.49 | 80.79 | 0.37% |

| VIX | 15.04 | -0.07 | -0.46% |

| Gold | 3,666.80 | -15.4 | -0.42% |

| Oil | 62.95 | 0.32 | 0.51% |

OVERVIEW OF THE US MARKET

Wall Street closed higher on September 9, 2025, with the S&P 500 hitting a fresh record as investors bet on Federal Reserve interest-rate cuts amid signs of labor-market cooling. The benchmark index rose 0.27%, while the Dow Jones Industrial Average climbed 0.43% and the Nasdaq Composite added 0.37%. Gains were driven by big tech names, though Apple Inc. fell 1.5% after unveiling its iPhone 17 lineup. In after-hours trading, Oracle Corp. jumped on strong bookings growth. Bonds declined, snapping a four-day advance, and oil rose amid Middle East tensions following an Israeli strike in Qatar.

Sector performance was mixed, with communication services leading gains at 1.64%, followed by utilities up 0.71% and health care advancing 0.60%. Materials lagged, dropping 1.57%, while industrials fell 0.65%. Among actives, Opendoor Technologies Inc. saw massive volume of 239.5 million shares, rising 1.16%, and NVIDIA Corp. gained 1.46% on 157.4 million shares traded. CaliberCos Inc. surged 323.72% amid high activity.

The session came as government data revealed a record downward revision to US payrolls, with job growth through March marked down by 911,000, signaling a weaker labor market than previously thought. This fueled expectations for Fed easing, with traders pricing in three cuts this year. Investors are now focused on upcoming inflation reports, starting with producer prices on September 10 and consumer prices on September 11, which could influence the Fed’s September 17-18 meeting.

Jamie Dimon, CEO of JPMorgan Chase & Co., noted the economy is weakening, though he stopped short of predicting a recession. Economists like Sal Guatieri at BMO Capital Markets said the revision gives the Fed another reason to lower rates next week. Chris Zaccarelli at Northlight Asset Management warned that hotter-than-expected CPI could spark stagflation fears, potentially derailing the rally.

Corporate developments included Nvidia announcing a new AI product, Google’s cloud unit disclosing $106 billion in commitments, and JPMorgan forecasting high-teens growth in third-quarter trading revenue. Boeing delivered 57 aircraft in August, its best for the month since 2018, while United Airlines reported a rebound in corporate travel. UnitedHealth anticipated strong Medicare ratings, but Humana shares dropped on tougher bonus criteria. Deals were prominent, with Anglo American acquiring Teck Resources for over $50 billion and Novartis buying Tourmaline Bio for $1.4 billion.

Strategists like Gary Schlossberg at Wells Fargo Investment Institute see the slowdown as a soft patch, supported by liquidity and prospective Fed cuts, favoring large-cap stocks. Omar Aguilar at Charles Schwab noted a 25 basis-point cut next week as the optimal scenario for markets, with a larger move risking alarm over economic health.

OVERVIEW OF THE AUSTRALIAN MARKET

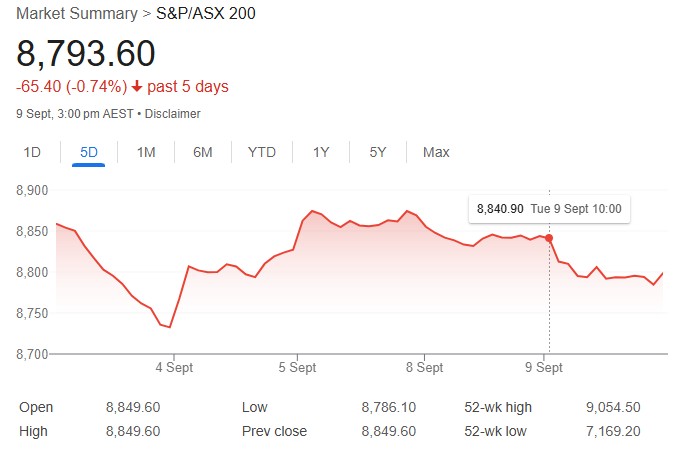

Australian shares extended their September slide on September 9, 2025, with energy, real estate, and healthcare sectors dragging the market lower amid seasonal weakness and dividend payouts. The S&P/ASX 200 shed 46.1 points, or 0.52 per cent, to close at 8,803.5, while the broader All Ordinaries dipped 46.2 points, or 0.51 per cent, to 9,080.7. Advancers trailed decliners 108 to 170 in the S&P/ASX 300, underscoring the lackluster session that saw the benchmark trade 0.52 per cent off its intraday high and just 0.23 per cent above its low.

September’s notorious reputation as the weakest month for global equities, including Australia, appears to be holding true so far, following a string of record highs in August. CommSec analyst Steven Daghian noted the pause is understandable after five straight months of gains and 10 all-time peaks last month, though the mood remains cautious. Dividend ex-dates sapped further momentum, with roughly $700 million flowing back to shareholders this week and tens of billions more by mid-October—CSL fell 1.6 per cent, BlueScope Steel dropped 1.9 per cent, Medibank eased 0.6 per cent, and Brambles declined 1.8 per cent, while Regis Healthcare bucked the trend with a 1.3 per cent rise.

8 of 11 sectors ended in the red, led lower by energy at minus 1.0 per cent, real estate down 0.9 per cent, healthcare off 0.9 per cent, and financials slipping 0.7 per cent. The big four banks all retreated, with Commonwealth Bank down 1.3 per cent to $166.08, Westpac off 0.8 per cent after Morgan Stanley named it its least preferred, and ANZ edging 0.2 per cent lower to $32.88 amid plans to cut over 3,000 jobs. Materials eased 0.4 per cent despite iron ore hitting its highest since October 8 last year, as BHP Group and Rio Tinto each fell 1.0 per cent—BHP after settling a $110 million class action over the 2015 Fundão dam disaster in Brazil—though Fortescue gained 1.5 per cent and Mineral Resources added 0.9 per cent.

Gold miners shone brighter, with the XGD index up 1.3 per cent as spot gold touched a record $US3,659 an ounce on fading odds of a US Federal Reserve September rate cut; Evolution Mining led with a 2.1 per cent jump to $9.12, marking a sixth straight week of gains for the sector. Lynas Rare Earths rose 2.8 per cent and Sandfire Resources climbed 1.9 per cent in energy transition metals, while lithium names like Pilbara Minerals fell 3.2 per cent and Liontown Resources 2.0 per cent; uranium was mixed with Boss Energy down 2.4 per cent but Paladin up 0.2 per cent.

Information technology provided a bright spot, up 0.4 per cent in line with a firm Nasdaq overnight, while consumer discretionary edged 0.3 per cent higher on strength from Wesfarmers and JB Hi-Fi. Standouts included Imricor Medical Systems surging 17.2 per cent with no fresh news, Boab Metals up 16.7 per cent amid precious metals momentum and uptrends, Echoiq ahead 16.3 per cent sans catalysts, Dreadnought Resources gaining 14.3 per cent on sector tailwinds, Polymetals Resources rising 13.3 per cent after an Endeavor Silver Zinc Mine update, and Golden Horse Minerals up 12.0 per cent in critical minerals. On the downside, 4DMedical plunged 27.5 per cent in a post-rally pullback after lung screening deals, Kaili Resources fell 17.6 per cent despite REE drilling news, Zeotech dropped 10.5 per cent following a securities quotation application, IperionX eased 10.0 per cent on director interest changes, and EQ Resources declined 8.3 per cent in line with downtrends.

News Corp slipped 1.4 per cent to $50.26 after going ex-dividend and settling the Murdoch family succession battle, handing control to Lachlan via a $5 billion share deal with his siblings. The Australian dollar strengthened, breaking above 66 US cents for the first time since July 24 to buy 66.09 US cents, up 0.26 per cent from Monday’s 65.76. US futures pointed higher overnight, with S&P 500 contracts up 0.16 per cent, Dow Jones adding 0.13 per cent, and Nasdaq futures gaining 0.19 per cent, offering potential relief ahead.