| Close | Previous Close | Change | |

|---|---|---|---|

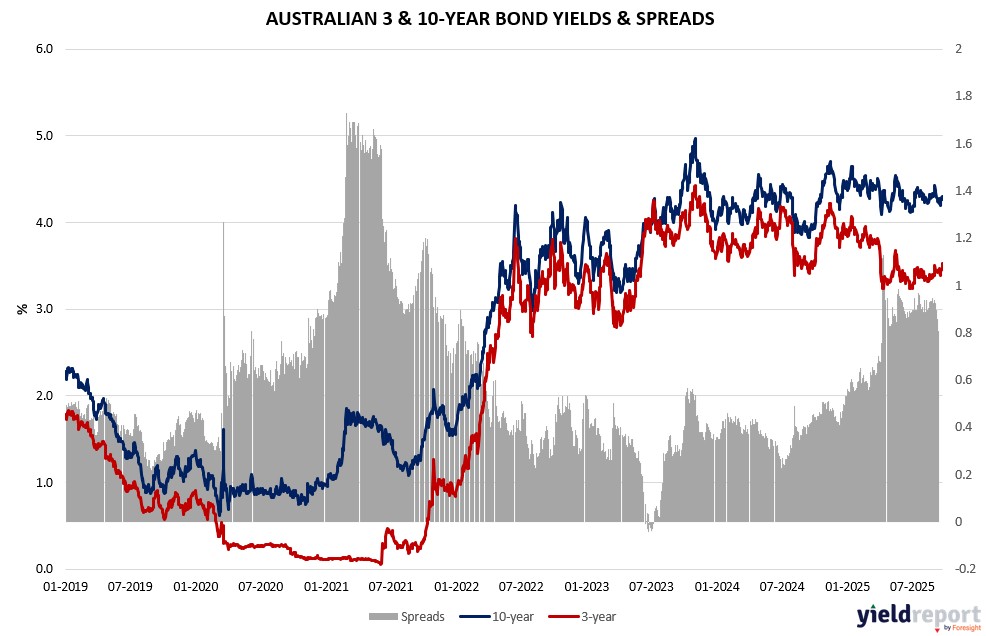

| Australian 3-year bond (%) | 3.522 | 3.459 | 0.063 |

| Australian 10-year bond (%) | 4.299 | 4.271 | 0.028 |

| Australian 30-year bond (%) | 5.004 | 4.999 | 0.005 |

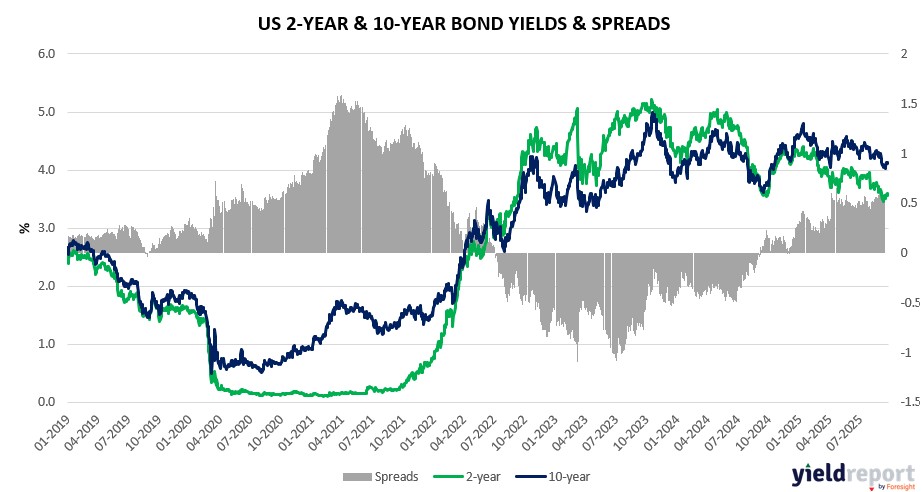

| United States 2-year bond (%) | 3.565 | 3.599 | -0.034 |

| United States 10-year bond (%) | 4.11 | 4.131 | -0.021 |

| United States 30-year bond (%) | 4.7252 | 4.7507 | -0.0255 |

Overview of the Australian Bond Market

August AU CPI surprised to the high side yesterday. The monthly annual indicator printed at +3.0% YoY (headline), up from +2.8% YoY in July and ahead of consensus median at +2.9% YoY. The trimmed figure dropped from +2.7% YoY to +2.6% YoY, and while the trimmed mean is the RBA’s preferred inflation measure, they don’t really look at the monthly measure, preferring the quarterly data.

The RBA focuses on the quarterly Trimmed Mean as the monthly TM is not directly comparable. As recently noted by Assistant Governor Hunter “we really don’t look at [the monthly trimmed mean] series. We don’t think that it’s a good read [on inflation].”

Current estimate for the September quarter Trimmed Mean inflation is 2.5%yr moderating further to 2.4%yr in the December quarter.

From a market pricing perspective, a September rate cut is completely off the table while a November cut has been priced down to possible rather than probable with just 30% priced in (down from ~75% – 80% over the past week or two).

Markets have shifted the terminal rate higher also, up from ~3.10% to 3.22%.

Credit spreads were resilient despite the stronger-than-expected CPI print. Domestic accounts continued to deploy cash across the credit spectrum, while offshore participation was muted by the Hong Kong typhoon.

Attention remained on the primary market, with new issues from Lonsdale Finance, Weir Group, and SGSPAA. In secondary trading, traders noted flow was mixed in front-end OpCos, demand for higher-beta names stayed firm and corporates saw selective interest, leaving overall sentiment constructive.

Overview of the US Bond Market

Bond yields climbed as traders positioned ahead of key data releases, with the 10-year Treasury yield rising four basis points to 4.14% and the 2-year up two to 3.60%, reflecting tempered expectations for aggressive Fed easing amid sticky inflation signals. The 30-year yield advanced three basis points to 4.75%, while shorter maturities like the 3-month fell to 3.95%. A stronger dollar and higher oil prices contributed to the move, as West Texas Intermediate crude rose 2.2% to $64.82 a barrel.

New home sales for August surprised at 0.8 million units, beating the 0.65 million forecast and revised prior of 0.664 million, signaling housing resilience despite higher rates. With core PCE prices due September 26—monthly expected at 0.2%, yearly at 2.9%—and consumption at 0.5%, markets are pricing in gradual cuts, though Powell’s balancing act on inflation and labor softness adds uncertainty. UBS’s Ulrike Hoffmann-Burchardi views the easing cycle as supportive for equities and bonds, forecasting 25 basis-point cuts through January 2026.

Existing home sales on September 25 are polled at 3.96 million for August, down from 4.01 million, potentially pressuring yields if weaker. Strategists at JPMorgan note client longs shrank ahead of the Fed, suggesting less bullishness, while asset managers pared positions in futures. The Treasury is expected to hold auction sizes steady for August-October, with no changes signaled.