| Close | Previous Close | Change | |

|---|---|---|---|

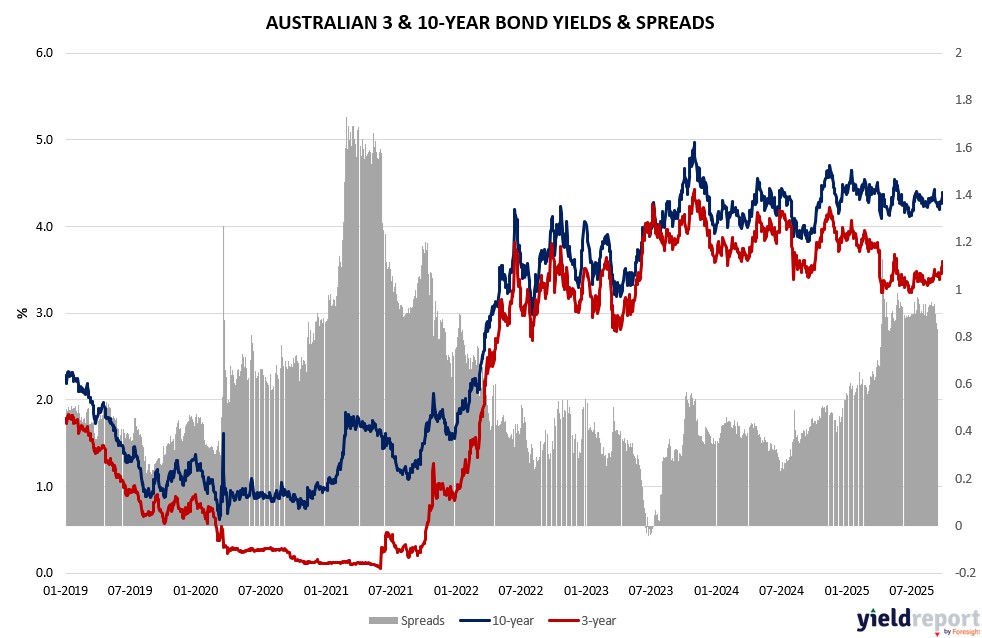

| Australian 3-year bond (%) | 3.596 | 3.556 | 0.04 |

| Australian 10-year bond (%) | 4.392 | 4.341 | 0.051 |

| Australian 30-year bond (%) | 5.063 | 5.05 | 0.013 |

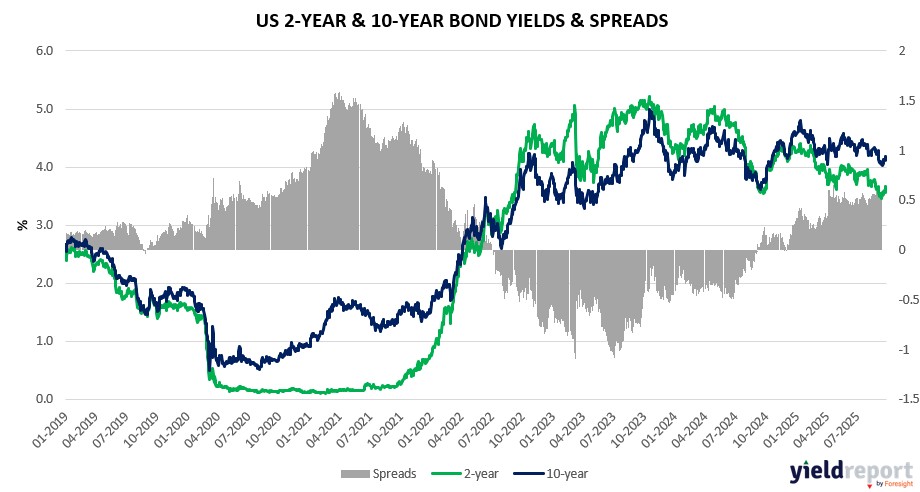

| United States 2-year bond (%) | 3.659 | 3.604 | 0.055 |

| United States 10-year bond (%) | 4.178 | 4.141 | 0.037 |

| United States 30-year bond (%) | 4.7576 | 4.7428 | 0.0148 |

Overview of the Australian Bond Market

Australian government bond yields edged higher across the curve, tracking US movements and local inflation data that tempered rate-cut expectations, as the economy shows signs of steadying amid global uncertainties. The 10-year yield rose four basis points to 4.38%, the 5-year added three to 3.80%, and the 2-year climbed three to 3.52%, reflecting recalibrated bets on RBA policy with cuts now fully priced only into 2026.

August’s CPI surprise at 3.0% seasonally adjusted year-over-year, alongside resilient US growth data, bolstered the view of persistent price pressures down under, even as flash composite PMI at 52.1 suggests cooling from prior highs. Trump’s tariff proposals, including on drugs, weighed on health care stocks but could indirectly support miners via commodity rallies, blending with domestic fiscal catalysts like potential stimulus. Markets see limited near-term volatility from US shutdown risks, historically neutral for equities, as bond trader’s position for a gradual easing path amid trend growth and tariff adaptations.

Overview of the US Bond Market

Bond yields showed mixed movements as traders digested inflation data that met forecasts and robust consumer spending figures, reinforcing expectations for measured Fed easing amid a resilient economy. The 10-year Treasury yield raised one basis point to 4.18%, while the 2-year declined one basis point to 3.64%, flattening the curve slightly as markets priced in about 40 basis points of cuts by year-end. The 30-year yield held steady at 4.76%, reflecting muted reactions to PCE details that kept inflation above the Fed’s 2% target but not accelerating.

With second-quarter GDP revised higher to 3.8% on stronger household outlays and intellectual property investment, bonds absorbed the narrative of a economy recovering from tariff shocks, potentially leading to better-than-expected third-quarter growth. Fed Chair Jerome Powell’s focus on labor-market cooling supports the case for an October cut, barring surprises in upcoming jobs data, though persistent inflation has some officials vigilant. A potential government shutdown could inject short-term volatility, historically having limited lasting impact on markets, as seen in the S&P 500’s flat average during past events.

In futures positioning, asset managers trimmed long positions in Treasury contracts last week, signaling caution ahead of policy clarity, while leveraged funds reduced shorts in longer tenors. Dealers anticipate steady coupon auction sizes for August-October, aligning with April guidance, as the rally in equities draws parallels to bonds’ sensitivity to economic strength and tariff resolutions.