Summary

Australia’s Monthly CPI Indicator rose 3.0% in the year to August, sitting between Westpac’s forecast of 3.1% and the market median of 2.9%, with forecasts ranging from 2.4% to 3.3%. On a monthly basis, the CPI fell 0.1%, softer than Westpac’s near-term projection of a 0.1% increase. The decline was driven by a sharp 6.3% fall in electricity prices, partly offset by a stronger-than-expected 0.4% rise in dwelling costs.

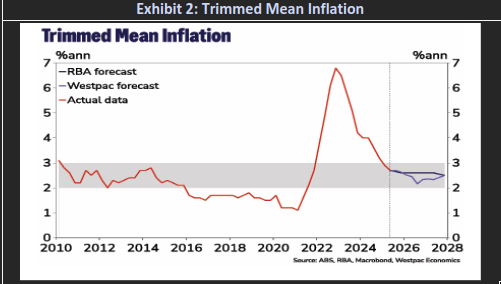

The Trimmed Mean estimate, a key measure of underlying inflation, eased to 2.6% year-on-year in August, down from 2.7% in July and 3.4% a year earlier. However, this monthly series excluded electricity’s annual rise and other significant price swings. Importantly, the Reserve Bank of Australia does not place weight on the monthly Trimmed Mean, with Assistant Governor Hunter noting it is not a reliable indicator of inflation trends.

Market Expectations

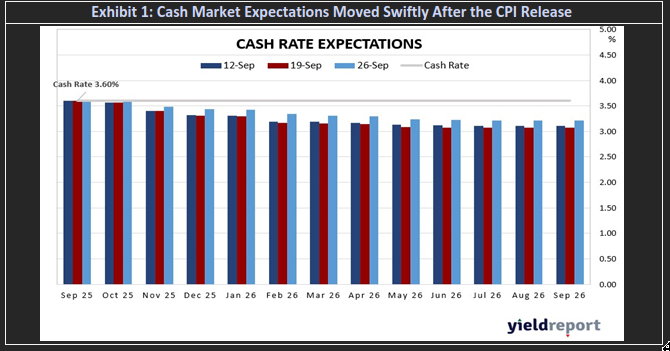

Bond traders have sharply reduced expectations for further interest rate cuts in Australia following a hotter-than-anticipated inflation reading for August. The consumer price index rose to 3.0%, up from 2.8%, surpassing economists’ forecasts of 2.9% and marking the fastest pace in over a year. This surprise spike triggered a swift reaction in financial markets, with the Australian dollar climbing to US66.21¢ and three-year government bond yields jumping 8 basis points to 3.53%.

The inflation data prompted major banks—including Deutsche Bank, Citi, NAB, and Barrenjoey—to revise down their forecasts for rate cuts by the Reserve Bank of Australia (RBA). Money markets now reflect less than a 50% chance of a rate cut in November, a stark shift from earlier expectations that had fully priced in a reduction. Bond traders are now anticipating just one more cut this cycle, likely in February, down from two earlier in the week.

Andrew Lilley, chief rate strategist at Barrenjoey, described the CPI print as “very hot,” suggesting it undermines the case for further easing. He argued that the RBA has already achieved a “perfect economic landing,” having slowed the economy enough to bring inflation within its 2–3% target without triggering a recession or spike in unemployment. The trimmed mean inflation, the RBA’s preferred gauge, eased slightly to 2.6% in August from 2.7% in July.

Despite the hawkish sentiment, not all market participants agree that the RBA is done cutting. Kris Bernie of Kapstream Capital emphasized that monthly inflation figures carry less weight than quarterly data, with the September quarter report due on October 29 seen as pivotal. Alex Joiner of IFM Investors echoed this caution, noting the RBA would need to see a more pronounced rise in unemployment to justify further cuts.

The Trimmed Mean estimate, a key measure of underlying inflation, eased to 2.6% year-on-year in August, down from 2.7% in July and 3.4% a year earlier. However, this monthly series excluded electricity’s annual rise and other significant price swings. Importantly, the Reserve Bank of Australia does not place weight on the monthly Trimmed Mean, with Assistant Governor Hunter noting it is not a reliable indicator of inflation trends.

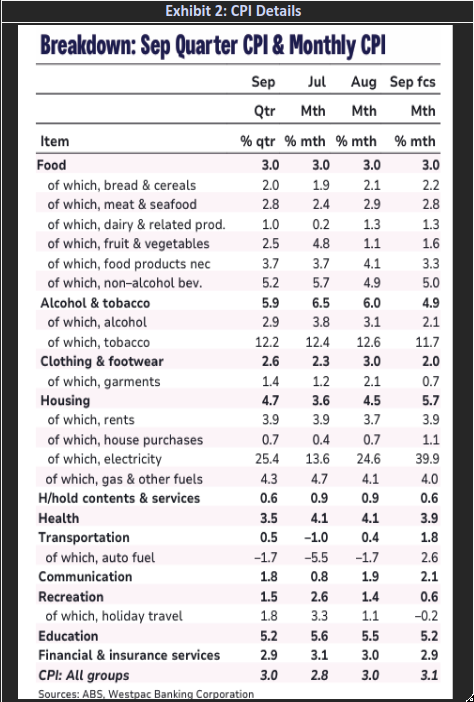

CPI – the Details

The Monthly CPI Indicator reflects partial data from the quarterly CPI survey, with some components only updated quarterly or annually. Therefore, averaging monthly figures doesn’t yield a reliable quarterly result. Instead, full-quarter prices must be applied judiciously.

For September, notable movements include strong rises in restaurant meals (1.3%), take-away foods (1.5%), and audio-visual services (6.3%), while motor vehicle accessories (–1.3%) and games (–3.3%) declined. These updates suggest balanced risks to the headline CPI, with falling electricity prices offsetting strength in services and housing. Consequently, the September quarter CPI estimate remains unchanged at 1.1% quarter-on-quarter and 2.9% year-on-year.