| Close | Previous Close | Change | |

|---|---|---|---|

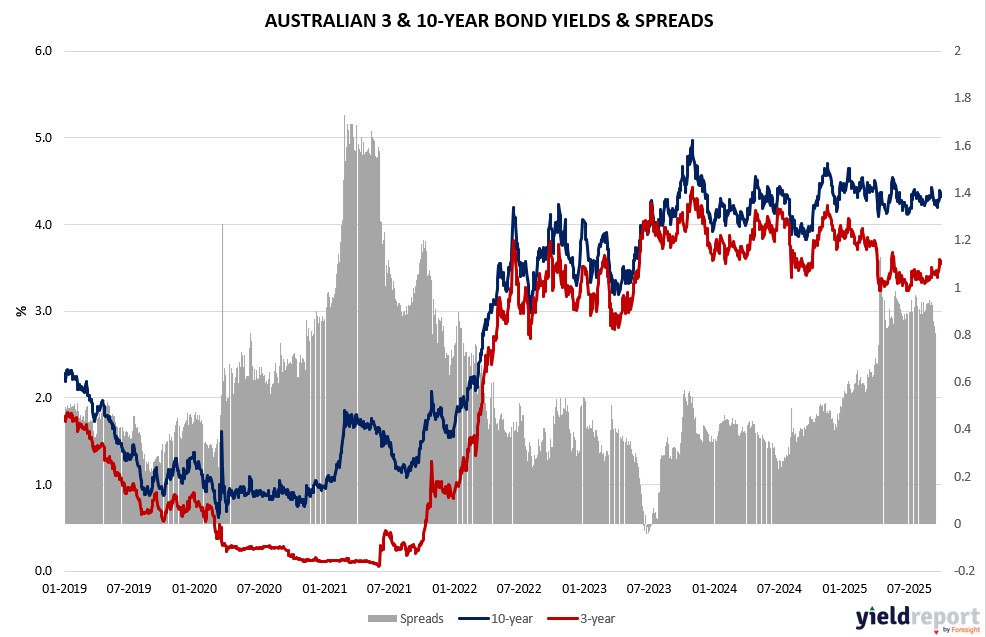

| Australian 3-year bond (%) | 3.574 | 3.552 | 0.022 |

| Australian 10-year bond (%) | 4.324 | 4.344 | -0.02 |

| Australian 30-year bond (%) | 4.992 | 5.018 | -0.026 |

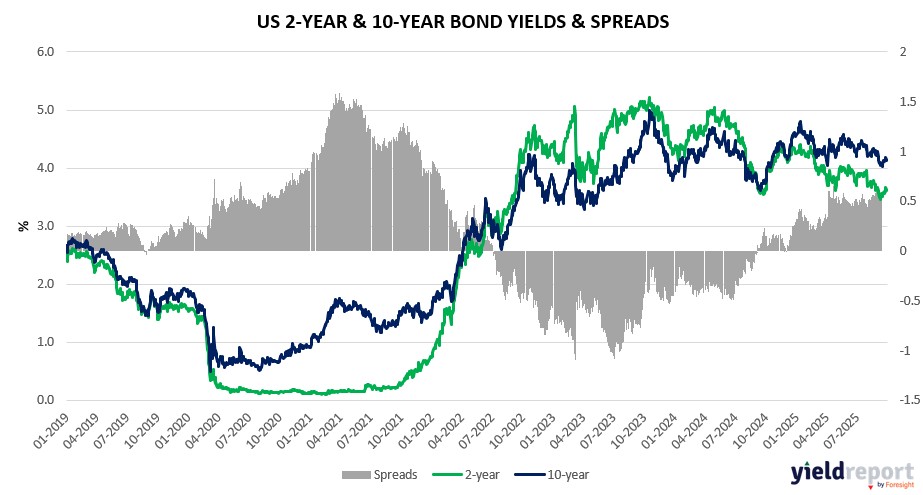

| United States 2-year bond (%) | 3.61 | 3.625 | -0.015 |

| United States 10-year bond (%) | 4.137 | 4.145 | -0.008 |

| United States 30-year bond (%) | 4.7075 | 4.7183 | -0.0108 |

Overview of the Australian Bond Market

Australian government bonds saw yields rise modestly on September 30, 2025, with the policy-sensitive 2-year yield up 5 basis points to 3.52% as the RBA’s hawkish commentary reinforced caution amid persistent inflation and a resilient labor market. The 5-year yield climbed 3 basis points to 3.78%, the 10-year added 1 basis point to 4.33%, and the 15-year held steady at 4.68%. Traders trimmed expectations for a November rate cut to 38% following the central bank’s statement highlighting slower disinflation and stronger private demand, with Governor Bullock noting the policy remains “probably a little bit restrictive” but urging patience as third-quarter inflation may exceed forecasts.

The RBA board emphasized uncertainties from domestic growth picking up, a strengthening housing market, and readily available credit, alongside international risks like US tariffs and geopolitical tensions that could dampen global demand. Economists at Toronto-Dominion Bank described the tone as hawkish, pushing some to delay expected easing to next year, while Bloomberg Economics noted the bank’s ability to remain patient given elevated monthly inflation at the top of the 2-3% target and steady unemployment at 4.2%. The Australian dollar strengthened above 66 US cents on the uplifted rate outlook.

August building approvals plunged 6% month-on-month, missing the 3% poll and signaling uneven recovery, while annual total approvals fell 1.2%. S&P Global Manufacturing PMI finalized at 51.4, slightly below preliminary. Ahead, Wednesday’s goods balance is eyed at A$6.2 billion, with exports potentially buoyed by commodities but tempered by China’s slowdown. Global factors, including Trump’s protectionist moves expected to curb growth and squeeze margins, add to the RBA’s vigilance on imported inflation, as the bank prepares its Financial Stability Review on Thursday.

Overview of the US Bond Market

Bond traders are increasingly betting that US 10-year Treasuries are poised for a rally, potentially driving yields to their lowest levels in five months. The shift comes ahead of a possible US government shutdown that could weigh on the economy, strengthen expectations for Federal Reserve rate cuts, and delay key economic data. On Tuesday, traders boosted bullish positioning, including a $35 million options premium targeting a drop in yields to around 4.05% by late November, compared with current levels near 4.15%. This follows a $50 million wager last week aiming for yields to fall as low as 3.95%, levels not seen since April’s market turmoil.

Strategists at BMO Capital Markets argue that investors view shutdown risk as supportive of lower rates. Historically, prolonged shutdowns have reinforced Treasury rallies, such as in 2018 when 10-year yields fell nearly half a percentage point during a month-long closure. The risk is heightened this time by President Donald Trump’s threat to fire federal workers in a shutdown and by potential delays to jobs data, which traders rely on to gauge Fed policy direction. Many see confirmation of a cooling labor market as necessary to fuel the next rally leg in Treasuries.

Positioning indicators confirm the shift. JPMorgan’s client survey shows long positions rising to their highest since April, while short positions declined. In SOFR (Secured Overnight Financing Rate) options, heavy activity centered on December 2025 contracts at the 96.50–96.625 strikes, signaling traders are targeting additional Fed rate cuts by year-end. Open interest in 10-year options surged, with demand concentrated on strikes implying yields between 4.05% and 3.95%. This growth reflects new bullish positioning rather than unwinding prior trades.

Meanwhile, CFTC data showed asset managers recently pared long Treasury futures positions for the third consecutive week, while hedge funds covered SOFR shorts. Despite some liquidation, options activity suggests traders are preparing for lower yields, with open interest spiking as buyers bet on declines below 4%.

The outlook hinges heavily on upcoming labor market signals, particularly Friday’s nonfarm payrolls release — now at risk of being delayed if the shutdown occurs. Without updated data, the Fed’s October decision may rely more heavily on its September dot plot, which projects a 25 basis point rate cut. Overall, traders are positioning for near-term volatility but see shutdown uncertainty, softer economic indicators, and Fed easing expectations as drivers of a sustained Treasury rally.