| Close | Previous Close | Change | |

|---|---|---|---|

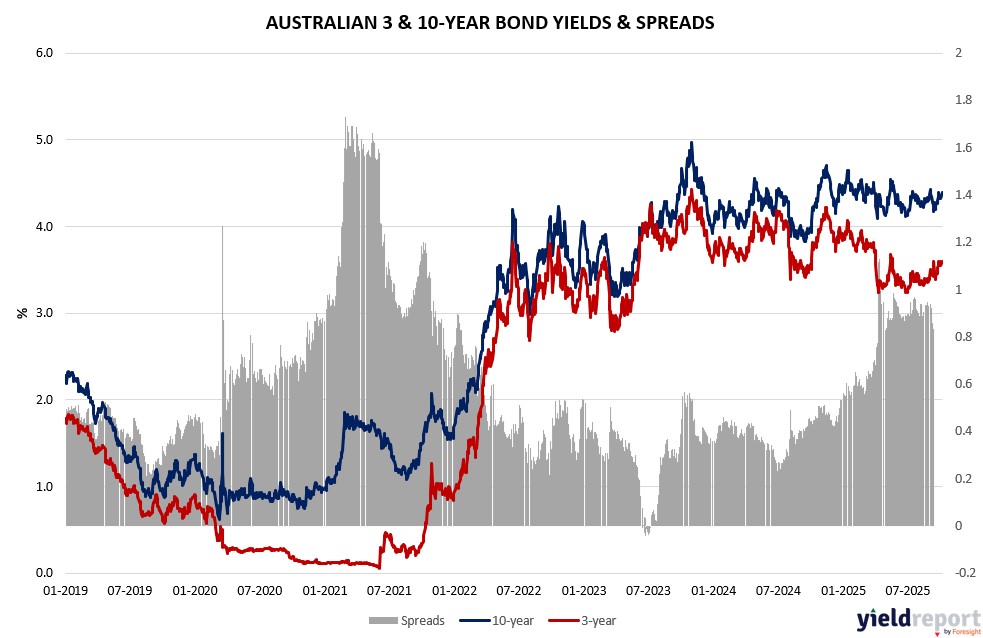

| Australian 3-year bond (%) | 3.582 | 3.592 | -0.01 |

| Australian 10-year bond (%) | 4.396 | 4.392 | 0.004 |

| Australian 30-year bond (%) | 5.069 | 5.012 | 0.057 |

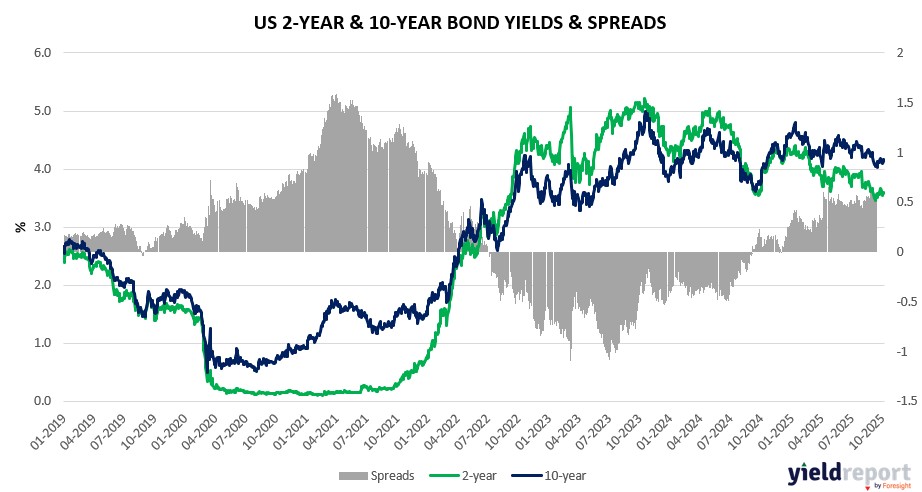

| United States 2-year bond (%) | 3.599 | 3.574 | 0.025 |

| United States 10-year bond (%) | 4.17 | 4.135 | 0.035 |

| United States 30-year bond (%) | 4.7664 | 4.7398 | 0.0266 |

Overview of the Australian Bond Market

Australian government bond yields rose modestly on October 7, 2025, tracking global caution amid US shutdown risks and local data signaling persistent inflation pressures. The 10-year yield climbed three basis points to 4.36%, the 2-year rose one basis point to 3.50%, and the 15-year advanced two basis points to 4.70%. The 5-year edged up one basis point to 3.76%, reflecting a flattish curve as markets digest fading RBA cut hopes.

President Trump’s tariff truce talks with China, including potential extensions, could indirectly support Aussie exports but heighten volatility in commodity-linked bonds. Domestically, weakening consumer sentiment and job ads reinforce a wait-and-see RBA stance, with no immediate easing signals ahead of key US payrolls that might sway global sentiment.

Strategists note bond proxies like real estate underperforming as yields rise, making equities less attractive, while high-PE tech faces harsher discounting. HSBC and UBS maintain long-term bullish equity views but caution on near-term pullbacks, seeing AI tailwinds and earnings growth as offsets to valuation stretches.

Futures positioning shows trimmed longs, aligning with a prudent diversification push amid high US valuations potentially spilling over to Aussie markets.

Overview of the US Bond Market

Bond yields eased on October 7, 2025, with the 10-year Treasury yield dropping three basis points to 4.13% following solid demand at a $58 billion sale, as traders sought safety amid equity pullbacks and shutdown uncertainties. The 2-year yield fell two basis points to 3.57%, and the 30-year declined two basis points to 4.72%. Shorter maturities like the 3-month bill rose to 3.82%, reflecting mixed views on near-term policy.

The rally in Treasuries comes as President Trump’s administration drafts memos questioning automatic back pay for furloughed workers under the 2019 law, escalating shutdown risks that could pressure fiscal dynamics. Treasury Secretary’s comments on potential tariff extensions with China add to the mix, with options for a 90-day delay under consideration, potentially easing inflation fears but heightening scrutiny on Fed independence.

Economic resilience persists, with upcoming data including Tuesday’s August trade balance expected at -$61 billion and Wednesday’s factory orders at 1.4% month-over-month, which may test the narrative of a soft landing. Thursday’s initial jobless claims at 223,000 and September payrolls could sway expectations for Fed cuts, currently priced at under half a point by year-end.

Strategists at BMO Capital Markets noted the pullback as a tech wobble providing a rally excuse for bonds, maintaining comfort in the prevailing range despite AI margin concerns. Goldman Sachs highlights bullish client sentiment at highs, while Barclays’ exuberance tracker signals caution. Asset managers trimmed net long positions in Treasury futures last week per CFTC data, with reductions concentrated in 5-year and bond contracts, as leveraged funds pared shorts.

Primary dealers anticipate steady coupon auction sizes for November-January, aligning with April guidance, though shutdown delays could disrupt issuance plans.