| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 46,601.78 | -1.2 | 0.00% |

| S&P 500 | 6,753.72 | 39.13 | 0.58% |

| Nasdaq | 23,043.38 | 255.02 | 1.12% |

| VIX | 16.3 | -0.94 | -5.45% |

| Gold | 4,040.60 | -29.9 | -0.73% |

| Oil | 62.15 | -0.4 | -0.64% |

OVERVIEW OF THE US MARKET

Wall Street rebounded on October 8, 2025, as dip buyers fueled gains amid speculation the bull market has legs after a brief pullback, with the S&P 500 climbing 0.58% to 6,753.72 and notching a fresh all-time high. The Nasdaq Composite rose 1.12% to 23,043.38, driven by AI enthusiasm, while the Dow Jones Industrial Average was little changed at 46,601.78. Nvidia led megacap advances as CEO Jensen Huang highlighted strong Blackwell chip demand, and AMD surged 11.37% extending gains from an OpenAI deal. Cisco escalated AI data center competition with new chips, while Opendoor Technologies tumbled 8.61% on heavy volume.

Sector gains were led by information technology up 1.52% and industrials at 0.85%, with materials adding 0.52%, contrasting declines in consumer staples down 0.52% and financials off 0.52%. The rebound followed a mild retreat that snapped a seven-day streak, amid thin economic data during the government shutdown. Recent releases showed September non-farm payrolls at a weak 22,000 versus expectations of 50,000, unemployment steady at 4.3%, and average earnings up 3.7% year-over-year as forecast, underscoring labor market cooling that may prompt Fed easing. August factory orders fell 1.3% month-over-month against a 1.4% rise poll, and international trade deficit widened to -$78.3 billion from -$61 billion expected, highlighting external pressures.

Fed minutes from September revealed officials open to further rate cuts this year but cautious on inflation, with tariffs a key discussion point and several noting AI’s potential to soften labor demand. UBS’s Mark Haefele sees the bull intact with tech P/E ratios below dot-com peaks, while Piper Sandler’s Craig Johnson urges vigilance on momentum divergences amid shutdown uncertainties. LPL’s Jeff Roach flags futures implying two more cuts this year but a January pause if inflation eases in 2026. Evercore’s Krishna Guha notes no Fed alarm on stock prices, with AI debates entering policy talks.

Corporate highlights included Elon Musk’s xAI raising $20 billion with Nvidia backing, Alphabet pushing back on DOJ bundling curbs for Gemini AI, and Paramount Skydance eyeing Warner Bros. Discovery. Ryanair received Boeing aircraft amid production ramps, Cenovus hiked its MEG Energy bid, and Shell prepared Venezuelan gas work under potential Trump license. Airbus delivered 73 planes in September, BMW cut guidance on China weakness, and SoftBank acquired ABB’s robots unit for $5.4 billion. Gold topped $4,000 an ounce, with Citadel’s Ken Griffin viewing it as a dollar de-risking signal, though correlations suggest separate paths amid central bank buying and momentum trades.

Looking ahead, Thursday brings initial jobless claims expected at 230,000 for the week ended September 29, while Friday’s preliminary October University of Michigan sentiment at 54.2 could gauge consumer resilience amid ACA subsidy debates.

OVERVIEW OF THE AUSTRALIAN MARKET

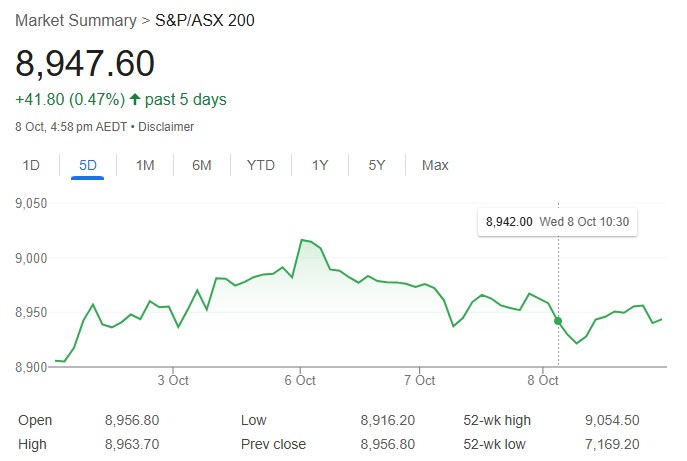

Australia’s share market extended losses for a third session on October 8, 2025, amid uncertainty and fading rate cut hopes, with the S&P/ASX 200 dipping 0.10% to 8,947.6 and the All Ordinaries down 0.10% to 9,244.8. Health care rose 0.55% and materials gained 0.55%, buoyed by miners, while consumer discretionary slumped 1.53%, information technology fell 1.23%, and communication services lost 1.07%. James Hardie surged 9.9% on preliminary Q2 results, Mesoblast climbed 9.4% after revenue beat, and Droneshield advanced 7.8% on AI software release. Liontown Resources added 5.7% amid lithium strength.

The pullback follows a rally above 9,000, with small caps up 0.10% continuing outperformance. September Melbourne Institute inflation expectations await Thursday, alongside US 10-year auction and Fed Chair Powell’s speech. Recent local data showed October Westpac sentiment down 3.5% and September job ads off 3.3%, reinforcing RBA caution. Gold miners eased 0.33% despite spot topping $4,000, as ETFs saw $64 billion inflows this year.

Standouts included Cyprium Metals up 17.5% and Arafura Rare Earths gaining 16.3% on critical minerals strength, while Dateline Resources dropped 25.2% post-rally. Pro Medicus rose on a $10 million German deal, but energy tracked lower with oil. New Zealand’s central bank surprised with a 50 basis point cut to 2.5%, lifting the kiwi against the Aussie.