| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 46,601.78 | -1.2 | 0.00% |

| S&P 500 | 6,753.72 | 39.13 | 0.58% |

| Nasdaq | 23,043.38 | 255.02 | 1.12% |

| VIX | 16.32 | 0.02 | 0.12% |

| Gold | 4,050.80 | -19.7 | -0.48% |

| Oil | 62.67 | 0.12 | 0.19% |

OVERVIEW OF THE US MARKET

Wall Street closed lower on October 9, 2025, as signs of an overstretched rally prompted caution amid a 36% surge from April lows, with the S&P 500 slipping 0.28% to 6,735.11. The Nasdaq Composite dipped 0.08% to 23,024.63, while the Dow Jones Industrial Average fell 0.52% to 46,358.42. Nvidia rose 1.83% on heavy volume, but energy and materials dragged, down 1.30% and 1.52% respectively, as oil sank on easing Middle East tensions. Consumer staples gained 0.61%, providing some offset.

Actives included Rigetti Computing up 8.98% and Plug Power adding 3.42%. Recent data showed August factory orders down 1.3% month-over-month versus 1.4% expected, underscoring industrial weakness, while September payrolls loom Friday at a forecasted 50,000 adds with unemployment at 4.3%. Initial claims for the week ended September 27 came in at 218,000 below 223,000 poll, offering labor resilience.

Truist’s Keith Lerner sees no excessive optimism despite froth, with the bull below median historical gains at 90% from 2022 lows. Piper Sandler’s Craig Johnson flags short-term stretches and breadth fatigue, suggesting consolidation. Bespoke notes returns after all-time highs nearly match averages since 1953, advising against overthinking. Sevens Report’s Tom Essaye views AI as a capex bubble needing adoption to sustain, not yet imminent pop.

Morgan Stanley’s Daniel Skelly highlights leading spenders’ earnings power differentiating from dot-com, recommending quality dividend growers as hedges. UBS’s Ulrike Hoffmann-Burchardi sees AI rally underpinned by fundamentals despite circular investment concerns. JPMorgan notes modest hedge fund exposure, signaling room before extended. City Index’s Fawad Razaqzada advises buying dips amid positive sentiment pre-earnings, with SoFi’s Liz Thomas expecting strong Q3 results supporting valuations, profit margins key amid tariff debates. Strategas’s Ryan Grabinski warns of buyback blackout weakness, but reassertion by November.

Corporate highlights included US approving Nvidia exports to UAE, Microsoft extending data-center crunch, OpenAI raising EU antitrust concerns over Google, Microsoft, Apple. Google’s Gemini Enterprise launches for workers, Amazon updates AI business tool. Tesla under NHTSA probe for traffic violations, Intel unveils turnaround products. Salesforce enters IT management, UnitedHealth eyes Massachusetts practice stake. Paramount’s Ellison sees media consolidation, Warner plans Minecraft sequel. Delta forecast strong demand, Citigroup rejected Banamex bid, Lyft partners Tensor for robotaxis. PepsiCo overhauls amid activist talks, Costco beat sales estimates. Trump mulls TP-Link restrictions, US rare-earth miners rally on China curbs. Marathon bought First Brands loan, Novo bought Akero for $5.2 billion, TSMC reported 30% Q3 sales rise.

Ahead, Friday brings preliminary October University of Michigan sentiment at 54.6 and inflation expectations.

OVERVIEW OF THE AUSTRALIAN MARKET

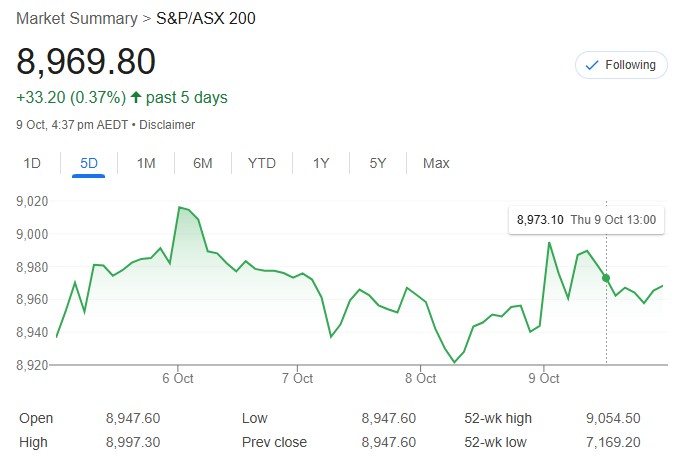

Australia’s share market ended higher on October 9, 2025, snapping a three-session slide as materials surged 1.80% on copper and rare earths strength, lifting the S&P/ASX 200 by 0.25% to 8,969.8 and All Ordinaries up 0.34% to 9,276.6. Small caps outperformed at 0.63%, emerging companies up 1.44%. Sandfire Resources rose 5.3%, Capstone Copper added 7.6%, Arafura Rare Earths gained 8.8%, Lynas up 5.3%. Infini Resources soared 226.1% on uranium hits, Marmota jumped 41.2% on gold grades.

September Melbourne Institute inflation expectations rose to 4.8% annually from 4.7%, hotter than anticipated, dimming RBA cut hopes. Consumer staples rebounded 0.67% with Coles and Woolworths, but financials fell 0.47% on NAB down 1.4%. Energy edged 0.09% as oil recovered slightly.

Standouts included Ioneer up 18.6% on US lithium stake, European Lithium gaining 18.2% on offtake LOI. Findi dropped 21.2% on guidance. Capital.com’s Kyle Rodda notes blind flying pre-Fed amid shutdown, with AI narratives driving globals. Betashares’ David Bassanese sees end-October inflation key for November RBA cut debate.

Ahead, Fed Chair Powell speaks Thursday, RBA Governor Bullock Friday, tentative US payrolls.